10 AI Budgeting Apps That Actually Save You Money (While You Sleep)

May 2026

Marcus found the problem on a Tuesday morning. He was in the kitchen, coffee in hand, balance open on his phone.

$340 missing. No idea where it went.

He’s not reckless with money. He doesn’t gamble. Doesn’t buy stupid stuff. He earns decent money and mostly lives within it. But $340 had just… evaporated somewhere between his last paycheck and that morning.

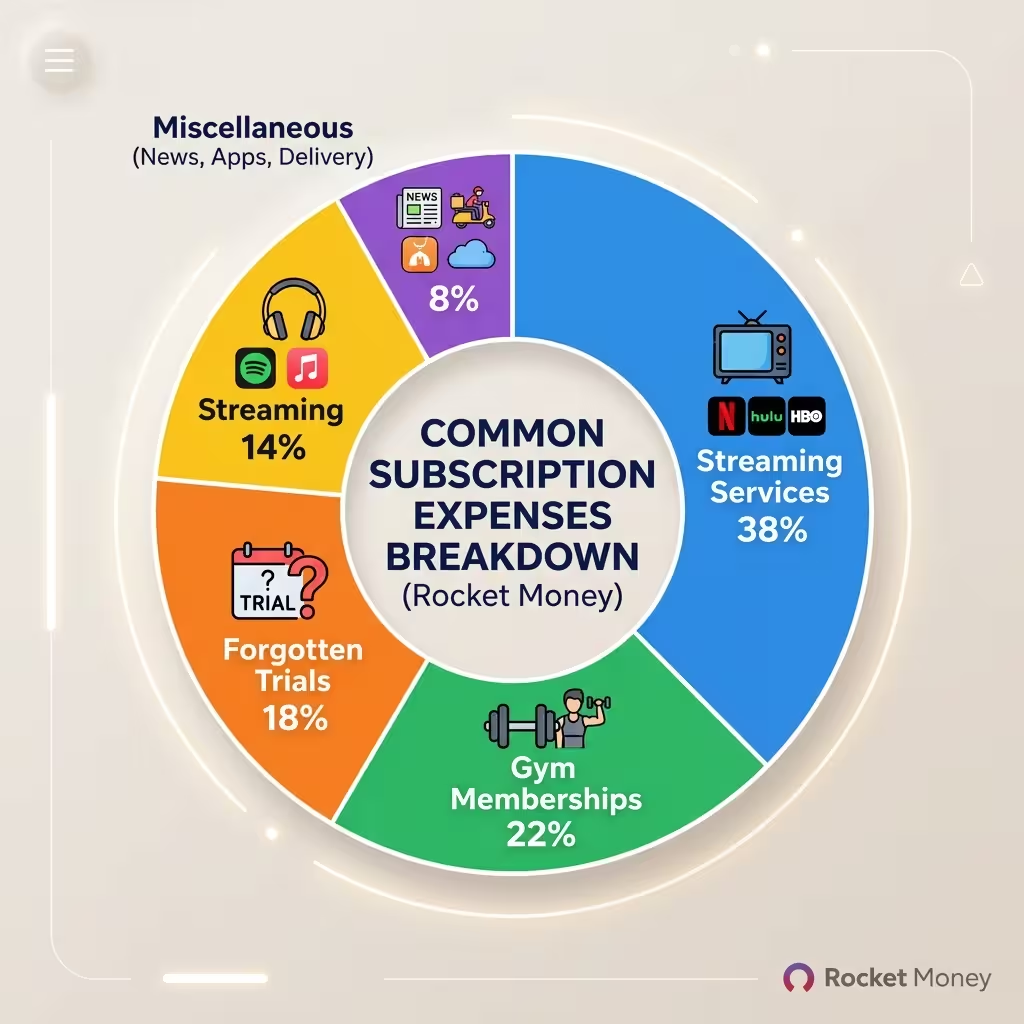

He scrolled through transactions for 20 minutes. Found it eventually. Three streaming services — he thought he’d cancelled one but hadn’t. A gym membership from March he kept intending to deal with. A food delivery membership he genuinely forgot existed. And a “free trial” from eight months ago that had been charging him $12.99 a month since October. He did the math on that one and felt briefly sick.

Nothing catastrophic. All small stuff. But the small stuff was the whole problem.

That’s what AI budgeting apps are actually built for. Not the dramatic financial decisions. The quiet drip of money leaving your account through forgotten recurring subscriptions and spending patterns you’d catch if you looked but never look.

Below are the ten best ones in 2026. What each does. Who it’s actually for. And the honest case for each.

Nothing here is financial advice. These are tools and observations. Talk to a licensed professional before making big decisions.

Why AI Apps Work When Spreadsheets Don’t

I’ve tried the spreadsheet. Most people have. It works for about three weeks.

The problem isn’t discipline. The problem is that a spreadsheet needs you. Every time you buy something, you update it. Get sick for a week, skip a weekend, travel for work — the spreadsheet falls behind and rebuilds the anxiety you were trying to remove. By week four most people have stopped opening it.

AI budgeting apps connect to your bank through read-only APIs — Plaid, Finicity, MX. These are data bridges that let the app see your transactions without being able to touch, move, or withdraw anything. Once connected, the categorization runs automatically. Forgotten subscriptions get flagged. Savings get moved when your balance has room. All without you doing a single thing after setup.

That’s the actual shift. Not smarter budgeting. Removing yourself from the process so your inconsistency can’t break it.

1. Rocket Money — Best for Finding the Leak

This is where Marcus started. If your money is disappearing and you can’t figure out where, Rocket Money is the first call.

It scans for recurring charges with high detection accuracy. The difference from other apps — and it’s a big one — is that after finding the subscriptions, Rocket Money cancels them for you. In-app. Their premium team handles it. They also negotiate your existing bills directly with providers. Cable, phone, internet. They keep 35% to 60% of whatever annual savings they generate. For most people the math lands comfortably in their favor.

The live “Safe-to-Spend” number is genuinely useful. It recalculates after every transaction and shows you what’s actually available before you start eating into rent or savings. If you’ve ever looked at your balance and thought you had room to spend, then overdrafted two days later, this number is what you were missing.

Beginners who find full budgets overwhelming: the Watchlist feature lets you track one or two specific categories — takeout, Amazon, coffee — without committing to a full budget setup. Awareness without pressure. Good place to start.

2. YNAB — Best for People Who Want Every Dollar Accounted For

YNAB is the manual option. Some people need that.

The system is called zero-based budgeting. Every dollar you earn gets assigned to something before the month starts. Rent gets its dollars. Groceries get theirs. Entertainment gets a number. Savings gets a number. You keep going until everything is accounted for and the leftover hits zero.

When you overspend on food one week, you pull from somewhere else. YNAB calls this “rolling with the punches.” The budget doesn’t break when life happens — it adjusts. That flexibility is actually what makes the system sustainable for people who’ve tried rigid budgets and quit.

The thing that changes the game long-term is a concept YNAB calls aging your money. The goal is to stop paying this month’s bills with this month’s paycheck. You want to get to where last month’s income covers this month’s expenses. That one-month cushion doesn’t sound life-changing until you have it. Then a car repair or medical bill stops being a crisis and starts being an inconvenience you handle from your cushion.

$14.99 a month. No ads, no data selling. Most people who stay with it three months don’t cancel.

3. EveryDollar — Best for the Ramsey Baby Steps

EveryDollar comes from Ramsey Solutions. It’s built around the Dave Ramsey method — pay off debt first, then save an emergency fund, then invest — in that specific order, no skipping.

The free version makes you type in transactions manually. A lot of people see that and immediately look for something with automatic sync. Fair enough. But the manual entry does something that automatic sync doesn’t: it makes you confront every purchase as you log it. There’s a version of financial awareness that only comes from typing the number in yourself.

Money left over at the end of the month doesn’t roll forward in spending categories the way it does in YNAB. EveryDollar points it toward whichever Baby Step you’re currently on. Behind on debt? The leftover goes to debt. Working on your emergency fund? It goes there. The whole app is designed around forward momentum on one goal at a time, not optimizing for everything at once.

If you’re carrying consumer debt and want a clear, step-by-step method rather than a passive tracking tool, this is the one that fits.

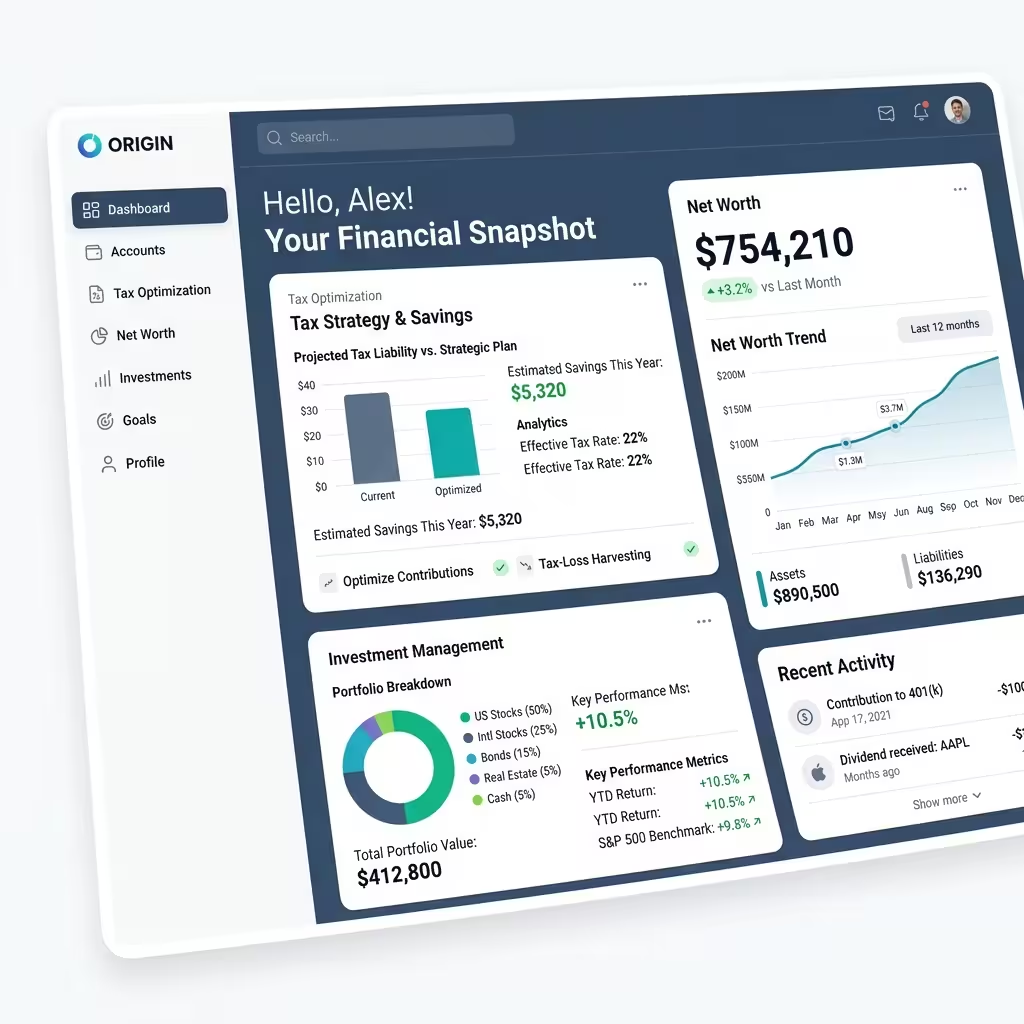

4. Origin — Best for Replacing Every Other App

Origin’s pitch is that it’s the last app you need to download.

Spending tracking, investing, tax filing, estate planning, one-on-one CFP sessions — all of it in one dashboard. The AI runs what they call multi-agent reasoning: multiple processes working across your accounts at the same time. You type something like “optimize for this year’s tax brackets” and it rebalances while modeling the tax impact, simultaneously. That’s not something most budgeting apps can do. Most budgeting apps don’t touch investing at all.

Net worth view is complete — assets, liabilities, full projection. The 2-in-1 toggle lets you flip between individual and joint views.

My honest read on Origin: if you’ve been managing three separate apps trying to get a full financial picture and still feel like you’re missing something, this solves the fragmentation problem. It’s the most complete tool on this list.

5. Monarch Money — Best for Power Users Who Want Control Over the Layout

Monarch connects to over 13,000 institutions. The dashboard is fully configurable — you build it around how you think about money, not around how someone else decided money should look.

The Sankey Diagram is the feature that gets mentioned most. It’s a flow visualization showing exactly where every dollar of income ends up — which categories it moves through, what lands in savings, what goes to bills. I’ve looked at a lot of personal finance dashboards and this is the clearest single view of cash flow I’ve seen.

Monarch recently got SOC 2 Type II certified. That’s not a badge they bought — it’s an ongoing independent audit of how the platform protects financial data over time. For anyone cautious about connecting accounts to a third-party app, it’s a meaningful signal.

Runs $8 to $15 a month. No ads, no data selling. Couples managing shared finances specifically: the shared view and joint account support here is the best outside of Origin.

6. Tilt — Best for People Who Can’t Make Themselves Save

Tilt watches your income and expenses in real time. When your balance has room, money moves to savings automatically. No decision from you. When cash flow tightens, it stops — no overdraft risk. The whole thing runs without you once it’s set up.

I’ve spoken to people who tried every app on this list and said Tilt was the only one that actually made them save money regularly. Not because it’s the most powerful tool here. Because it removed the moment where they had to decide. For anyone whose savings strategy has always been “I’ll set something aside at the end of the month” — and the end of the month arrives and there’s nothing left — this is the one that actually breaks that cycle.

7. Acorns — Best for Starting Investing Without Thinking About It

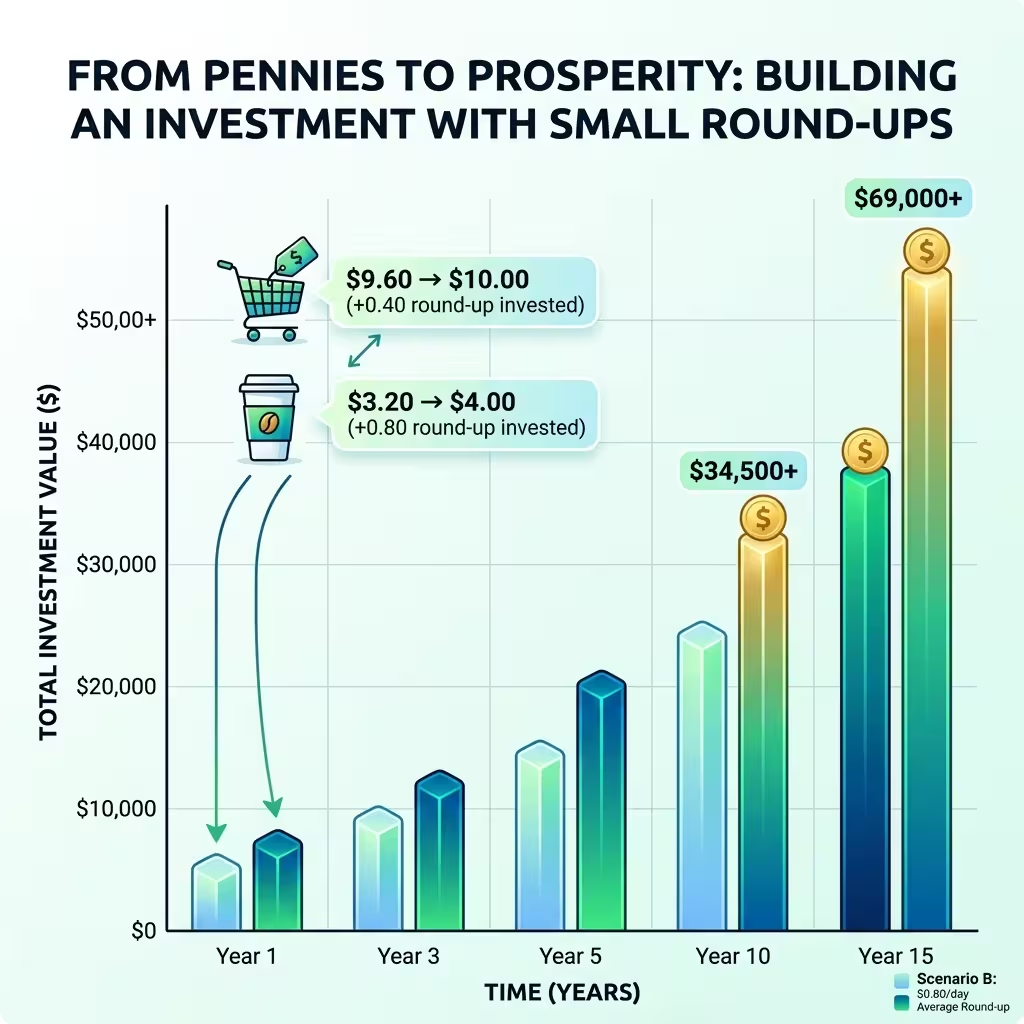

Acorns rounds up every debit card purchase to the nearest dollar. Buy a sandwich for $8.60, Acorns moves $0.40 to your investment account. It happens automatically, every transaction.

Those amounts feel like nothing. $0.40 here, $0.80 there. Over a year they add up into something real. The invested money goes into ETF portfolios put together by financial professionals. Nothing to pick. Nothing to rebalance. The portfolio builds while you just live your life.

Honest assessment: this is not a serious long-term investment strategy on its own. But for someone who has been telling themselves they’ll start investing “when things settle down” — and things never settle down — Acorns makes that procrastination impossible. You start the moment you connect the card.

8. Cleo — Best for Under-30 Users Who Find Budgeting Boring

Cleo has a personality. Roast Mode will mock you with memes when you overspend. Hype Mode celebrates you when you’re doing well. That sounds like a gimmick until you think about why most budgeting apps fail — they show you a pie chart, you close the pie chart, nothing changes. Cleo is designed around the idea that embarrassment is more motivating than data.

Whether the roasting actually changes your behavior depends on whether you’re the kind of person who laughs at that kind of thing. A lot of people under 30 are. Cash advances up to $250 interest-free for paid members. Secured cards for building credit without a credit check. An AI coach that talks like a person, not like a terms-and-conditions document. If you’ve downloaded and abandoned three budgeting apps because they felt like doing homework, try this one instead.

9. PocketGuard — Best for Impulse Spenders

The “Safe-to-Spend” number is what this app is really about. It recalculates constantly — every transaction, every bill that clears, every savings contribution. You always know the exact dollar amount you can spend without touching anything you shouldn’t. Not an estimate. Not yesterday’s number. Right now.

Snowball vs. Avalanche debt payoff plans are built in. You pick your method, the app shows you the projected payoff date, and it updates whenever your situation changes. Subscription price creep gets flagged too — those small $1 and $2 increases that services slip in and most people don’t catch for half a year. PocketGuard catches them immediately.

For someone who knows they overspend but can’t seem to stop, this builds friction into the process. Not by lecturing. By showing you a number that changes the moment you consider spending past it.

10. Quicken Classic — Best for Complex Investors

Quicken Classic is old. It’s been around since before smartphones. That age means depth the newer apps simply don’t have.

Real-time investment quote tracking. Transaction assignment to specific tax lines — genuinely useful for anyone who itemizes deductions or runs a business. Cryptocurrency support. The reporting depth is more robust than anything else in the consumer finance space.

Desktop-first is a real limitation if you manage everything from your phone. But for someone tracking a complex investment portfolio, multiple income sources, and a side business, Quicken Classic does things Origin and Monarch don’t yet. It’s not the modern choice. It’s the right choice for a specific type of user who needs serious tools and doesn’t mind a desktop interface to get them.

Which One Should You Pick

Here’s the honest answer: it depends entirely on where you’re leaking money and whether you’ll actually maintain a system.

If subscriptions and forgotten charges are the problem — Rocket Money first. Most people recover the subscription fee in the first week just from what it finds.

If you want real control and you’ll actually do the manual work — YNAB. If you need the Ramsey structure to stay motivated — EveryDollar. Both require your ongoing attention. Be realistic with yourself about whether you’ll give it.

If you want one app that handles everything, including taxes and investing — Origin. Especially worth it if you’ve been juggling three apps and still feel like you’re missing the full picture.

If you live with a partner and your money conversations always turn into arguments — Monarch Money. The shared dashboard genuinely reduces that friction.

If you’ve been meaning to save but it never happens — Tilt. Take the decision away from yourself.

If investing feels too complicated to start — Acorns. Connect the card, forget about it.

If you’re under 30 and boring finance apps make you close the app — Cleo. The roasting is annoying and it works.

If you already know you overspend and want something to stop you — PocketGuard. The live number changes behavior in a way a chart doesn’t.

If you have real investment complexity — multiple income streams, a business, a detailed portfolio — Quicken Classic. Nothing else touches it at that level.

One app used for 60 days straight will do more than six apps opened twice and abandoned. Start with your biggest problem and go from there.

People Also Ask – PPA’s

What are the 10 best AI budgeting apps to save money automatically?

Rocket Money, YNAB, EveryDollar, Origin, Monarch Money, Tilt, Acorns, Cleo, PocketGuard, and Quicken Classic. Each solves a different problem. Rocket Money is the subscription killer. Origin is the all-in-one. YNAB is for manual control. Acorns is for passive investing. Pick based on your situation, not on app store rankings.

What are the top-rated AI expense trackers for iPhone?

Rocket Money, Monarch Money, Origin, and YNAB all have strong iPhone apps in 2026. Rocket Money leads on subscription detection. Monarch leads on customization. Origin leads on all-in-one functionality. YNAB leads on zero-based budgeting. All four use 256-bit encryption and read-only account access.

Are these apps safe to connect to my bank account?

Yes, when they use read-only API access through verified aggregators like Plaid, Finicity, or MX. These connections let the app see transactions but cannot move or withdraw funds. Look for SOC 2 Type II compliance, 256-bit encryption, and multi-factor authentication before connecting anything.

Does Rocket Money actually negotiate bills?

Yes. It contacts your service providers directly — cable, phone, internet — and negotiates lower rates on your behalf. It keeps 35% to 60% of the annual savings it creates. Most users find the savings exceed the fee comfortably.

What’s the difference between YNAB and the automated apps?

YNAB requires active management — you assign every dollar manually and adjust throughout the month. It builds real financial awareness but needs your ongoing attention. Apps like Tilt and Acorns run without your involvement. Both approaches work. YNAB builds faster habits. Automation is more sustainable for people who won’t maintain a manual system.

What Marcus Did

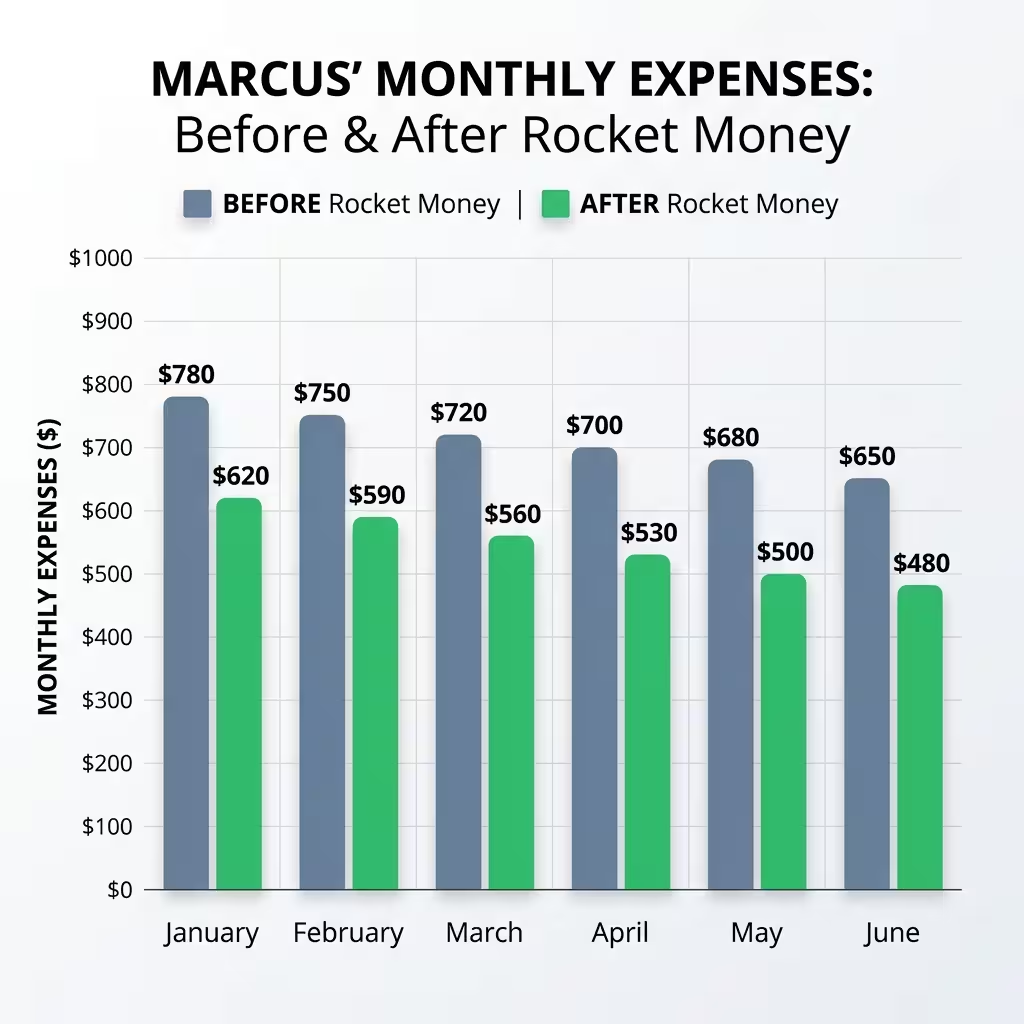

He downloaded Rocket Money on that same Tuesday morning.

Setup took about 15 minutes. The app found the gym membership, the forgotten trial, and the duplicate streaming service. He cancelled two of them in-app before his coffee was cold. Rocket Money’s team handled the internet negotiation.

Next month his balance was $87 higher without changing a single spending decision.

Four months in, he still hasn’t built a proper budget. Probably never will. But the quiet automated expense tracking running in the background has saved him more than any spreadsheet ever did.

That’s the honest case for these apps. They don’t ask you to become someone different. They just close the holes the current version of you is walking past every month.

The money was always there. It just needed a system to hold onto it.

Disclaimer: General information only. Not financial advice. App features, pricing, and availability may change. Verify current details with the app provider before subscribing or connecting financial accounts. The author and publisher accept no liability for outcomes based on this content.