The Ultimate Guide to AI Cash Flow Forecasting: Transforming Treasury for 2026

Last Updated: April 2026

Disclosure: Some links in this post are affiliate links. If you buy through them, we earn a small commission at no extra cost to you. I only mention tools I’d actually recommend.

Let me tell you what happened at a planning meeting I sat in on last October.

The CFO — sharp woman, ran a tight meeting — stopped the whole agenda about 20 minutes in and turned to the treasury director. Asked one question. Where’s our cash in 90 days?

The treasury director opened Excel. Scrolled. Said something about the ERP export being behind and an AR reconciliation that hadn’t closed from last week. The CFO picked up her coffee, closed her laptop, and left the room.

That was it. Meeting over. Someone eventually made a joke, people filtered out, and that was the whole thing.

I talked to the treasury director afterward. She knew her stuff. The spreadsheet was real, the numbers were real, the problem was the numbers were already wrong — three, maybe four days stale before they even landed in her model. She had no way to give her CFO a better answer because the system she was working from wasn’t built to give one.

That gap is the whole reason AI cash flow forecasting exists. Not to make treasury teams feel better about their spreadsheets. To replace the thing underneath them that was broken all along.

A note before we go further: I want to be upfront where I’m uncertain and where I’m not. The accuracy numbers in this post come from published research across global treasury practitioners — not vendor pitch decks. Where I’m drawing on my own experience talking to finance teams, I’ll say so.

Why Manual Forecasts Keep Getting It Wrong

Treasury directors and CFOs who’ve been through this know the excuses by heart. ERP exports were late. The business units didn’t report on time. AP and AR are on separate systems. Finance couldn’t get clean numbers from ops.

None of that is wrong. All of it is real.

But those things aren’t causes. They’re symptoms of a deeper problem — your forecast is built from a snapshot of the past, not a picture of right now.

By the time a standard ERP snapshot lands in a forecast model, it’s usually three to seven days old. During those three to seven days, things moved. An invoice that showed as open Thursday is now disputed. A customer who owed $200K called your AR team Monday and got an extra 45 days. Three payments that were “expected this week” already matched in clearing and are about to post.

Your model has none of that. So it predicts based on what was true last week.

Here’s the analogy that landed best when I was trying to explain this to someone outside finance: you photograph a highway at 6:30am and then at noon someone asks how bad the traffic is right now. You have a photo. It was accurate once. But the highway kept going after you stopped looking at it.

Predictive liquidity management works from live data — actual dispute flags, real promise-to-pay commitments from customer calls that happened this morning, payment probability built off how each specific customer actually behaves over time. Not how their customer segment behaves on average. That specific company, that specific contact, that specific history.

One treasury team I spoke with — I’m not naming the company — had a mid-size distributor in their AR portfolio. Classified as net-30 reliable for two years straight. Never caused a problem. What the segment-level model never caught: this same customer started disputing every fourth invoice in early 2024. The AR team knew about it. The forecast model had no idea. Pattern was obvious at the invoice level. Invisible when averaged across the segment.

That’s the gap. That’s what the new tools close.

What’s Actually Different About 2026

I’m going to be honest — I was skeptical about this for a while. We’ve been hearing “AI is going to transform finance” since at least 2018. Most of it landed with a thud. Piloted something, saw mixed results, moved on.

The thing that changed isn’t the technology. It’s the operating conditions.

FX volatility is sharper right now than most treasury teams have had to deal with in years. Supply chains are getting hit by tariff shifts with almost no advance notice. Interest rates haven’t settled. In that environment, a three-day-old cash position isn’t just inconvenient — it’s a decision being made on wrong information.

The language CFOs use about forecast misses has shifted too. Used to be treated as a statistics problem — bad inputs, look at the methodology, try harder. Now it’s being framed as an operational clarity problem. The business doesn’t know its own cash position. That’s a different category of failure and it lands on treasury teams differently.

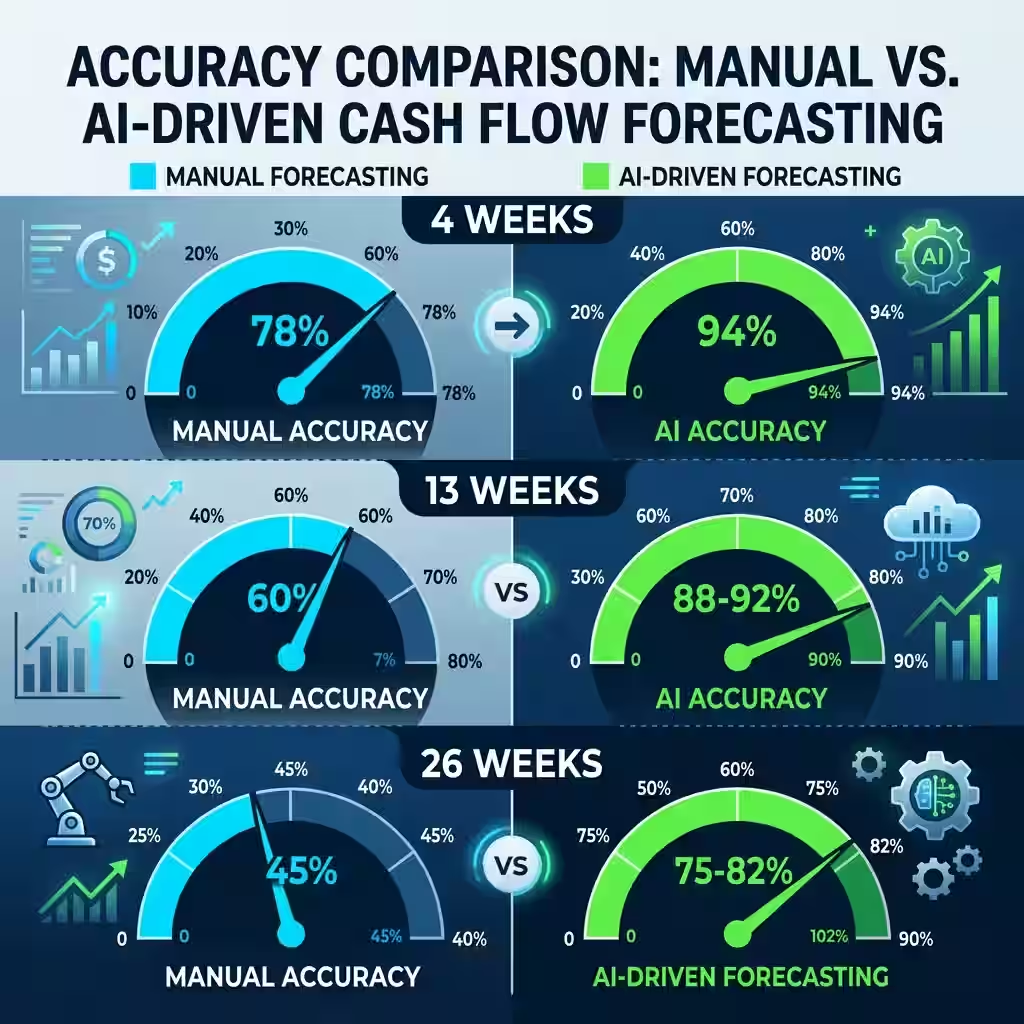

Manual 13-week forecasts average around 60% accuracy, based on research from global treasury practitioners. AI-driven models on the same time horizon are hitting 88-92%. Four-week accuracy pushes toward 94%.

“If you want a step-by-step walkthrough of actually building this, we’ve put together a full guide on how to automate a 13-week cash flow forecast with AI.“

I’ll be honest — when I first saw those numbers I assumed they were padded. Then I looked at why. It’s not a smarter model. It’s better inputs. AI forecasting runs off real-time bank feeds and processed AR data. Manual forecasting runs off whatever export someone pulled last night or the night before. The input gap explains almost all of the accuracy gap.

For treasury directors sitting at 60% accuracy: that means you’re off by 40% on average. That’s not a rounding problem. That’s a different picture of your business.

The Agents — What They Actually Do Day to Day

The phrase “Agentic AI” has been everywhere lately and it doesn’t always get explained clearly. Let me try.

“If you’re trying to decide which type of AI is right for your treasury team, we break down the exact difference in agentic AI vs. generative AI for treasury forecasting.“

Old treasury automation was rule-based. You’d code: if an invoice hits 30 days past due, trigger a collections email. If a bank balance drops below a threshold, send an alert. Those rules worked fine until something happened outside the rules — a dispute, a negotiated extension, a partial payment. Then the system had no idea what to do.

Modern automated cash flow software runs on agents instead. These are specialized AI systems, each one built to own a specific slice of the workflow. They don’t follow fixed rules — they learn from patterns and keep adapting as patterns change.

A collection prediction agent looks at customer payment history, invoice characteristics, dispute activity, and seasonality for each account. If late payments are your most pressing problem right now, we’ve gone deep on exactly this in our guide to predicting late payments with AI pattern recognition. It tells you which invoices are likely to be paid this week and which aren’t. Teams running these have cut Days Sales Outstanding by two to four days. That’s free working capital — you didn’t collect faster, you predicted correctly and managed accordingly.

Liquidity positioning agents connect directly to bank accounts and classify transactions as they come in. GL entries get generated on their own. No waiting for statements. No morning reconciliation. For any company with banking relationships across multiple countries, this closes a visibility gap that used to take a small team half a day to patch together manually every morning.

The variance analysis piece is the one I hear treasury directors get most excited about. When actuals don’t match forecast — and they will drift — the agent doesn’t just flag a number in red. It explains the gap. Which customers paid late. Which AP timing shifted. It generates a narrative that goes straight to the board instead of spending two days on the phone with department heads trying to figure out whose line items moved.

Scenario agents are the ones that change how meetings run. You can simulate live — what does our 30-day cash position look like if we push collections on the top 20 accounts a week earlier? What if our biggest customer stretches to 60 days? These were quarterly planning exercises that took days to model. Now someone runs them in a few minutes while the conversation is still happening.

The human job doesn’t disappear. It changes. You stop building the forecast and start questioning it — bringing context the model can’t have. A vendor relationship about to change. A deal close to signing. A customer you know is in trouble even though their invoices are still current. That’s where the real work is now.

A Closer Look at the AI Cash Flow Accuracy Numbers

Because fintech accuracy claims get inflated constantly, I want to be precise about where these come from.

The figures below come from research synthesized across global treasury practitioners and published platform benchmarking — not marketing materials:

| Forecast Horizon | Manual Accuracy | AI-Driven Accuracy |

| 4 weeks | ~78% | ~94% |

| 13 weeks | ~60% | 88–92% |

| 26 weeks | ~45% | 75–82% |

The metric is MAPE — Mean Absolute Percentage Error — presented as accuracy rather than error rate.

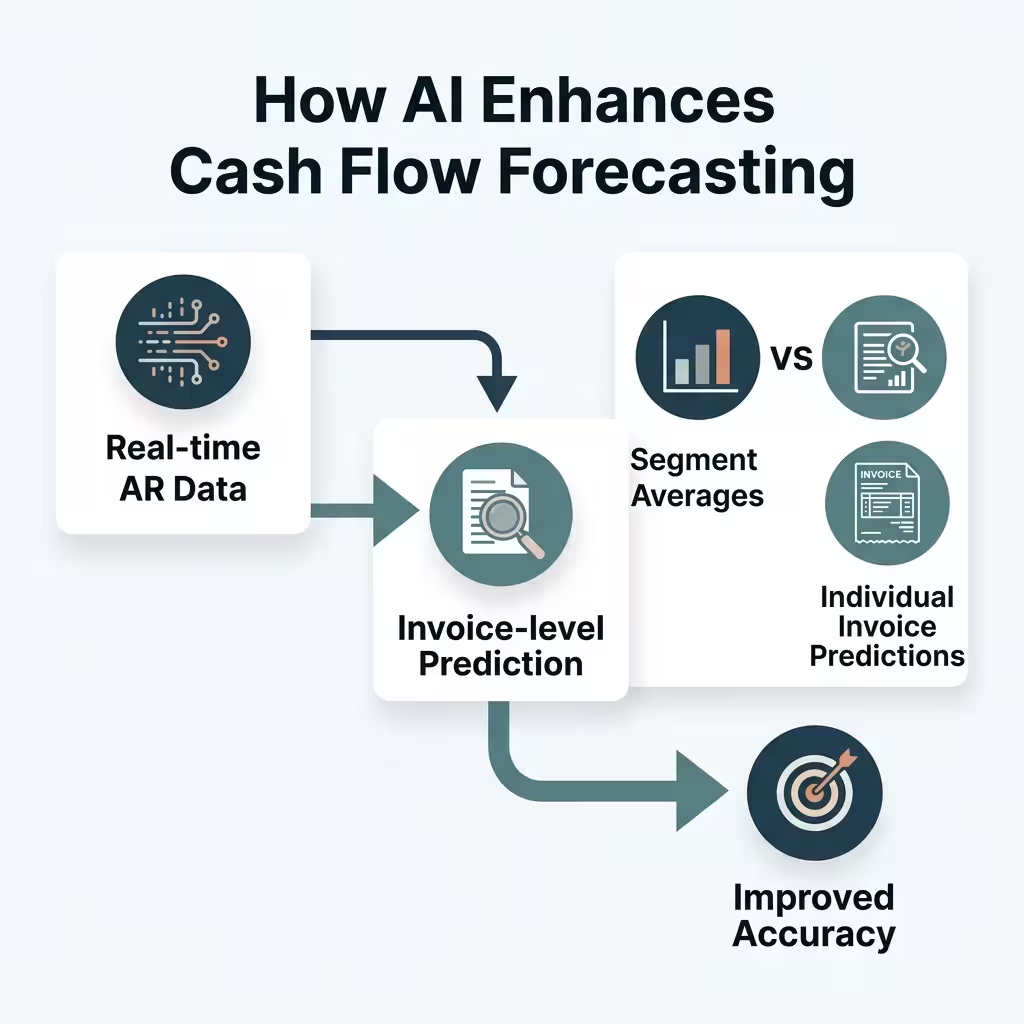

Machine learning financial forecasting gets there through two things traditional models can’t replicate.

First, invoice-level prediction instead of segment averages. Traditional tools aggregate receivables by customer tier and apply historical averages. That smoothing hides variation that actually matters. AI tracks individual customers and assigns payment probability per invoice independently. When you’re dealing with hundreds of open invoices, the aggregate view makes everything look more predictable than it is.

Second, live ERP integration through API connections, not scheduled batch exports. The model runs on current data, not yesterday’s pull. That alone closes a lot of the gap.

Worth saying plainly: AI forecasting doesn’t get harder to maintain as the business scales. SaaS founders dealing with burn rate and runway pressure will find this especially relevant — we’ve written specifically about AI cash flow forecasting for SaaS startups. It gets more accurate because it has more behavioral data to work from. Manual spreadsheet models do the opposite — they degrade as complexity grows.

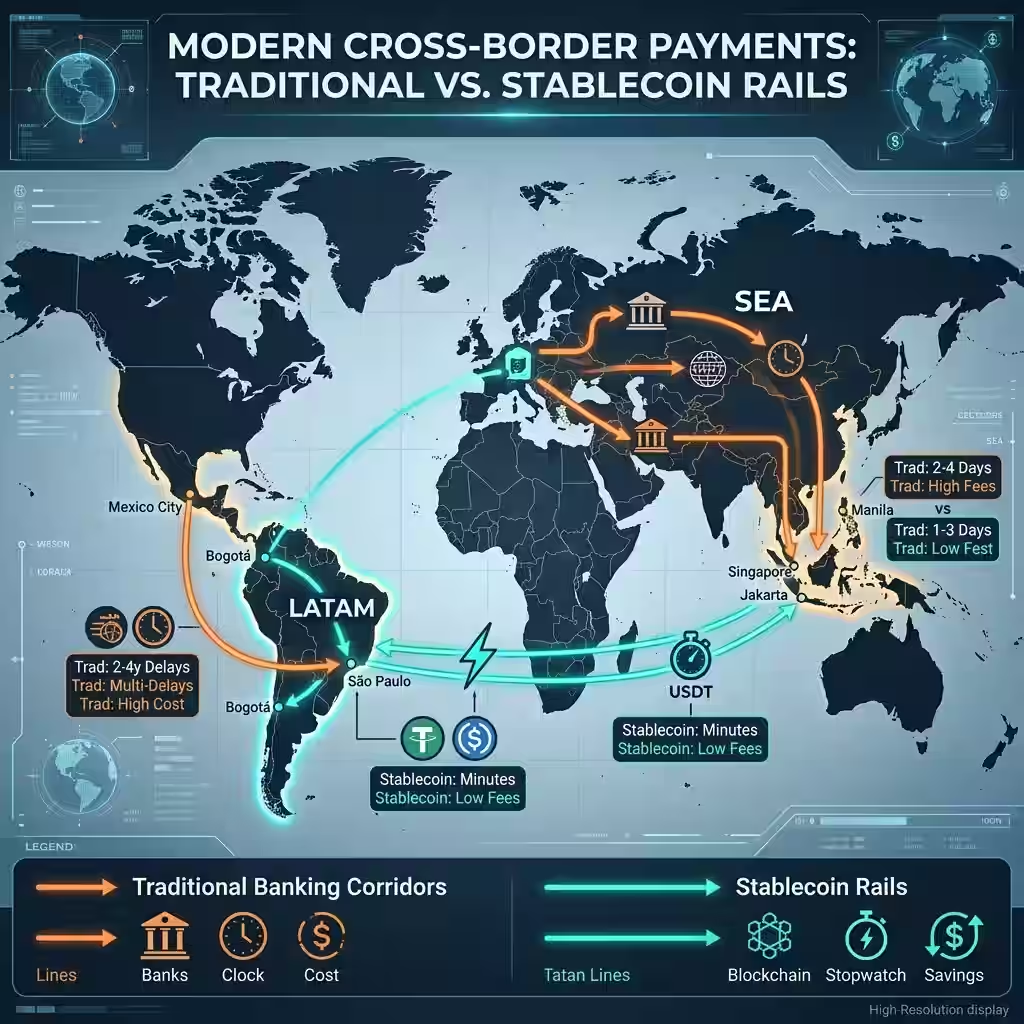

What the Cross-Border Payment Problem Actually Looks Like

Here’s a working capital optimization angle I don’t see discussed enough in treasury content.

Cross-border payments through traditional banking are genuinely slow and expensive in a lot of corridors. A U.S. company paying a supplier in Southeast Asia or parts of Latin America can wait three to five business days for settlement. Add the conversion spread on top of the wire fee and the cost compounds quickly for any company doing real volume internationally.

Some corporate treasury teams — more than the crypto association might suggest — are using stablecoin rails to fix this for specific corridors. Not as an investment. As a settlement tool. A payment that takes five days through standard banking can settle in hours on-chain. The balance shows up on the treasury dashboard next to USD and EUR. Once settlement is done, you close the position and you’re out. You’re not holding a speculative asset.

Kyriba and others have integrated these rails into their platforms. For treasury teams with meaningful cross-border volume in tight corridors, this is worth an actual conversation with your banking partners.

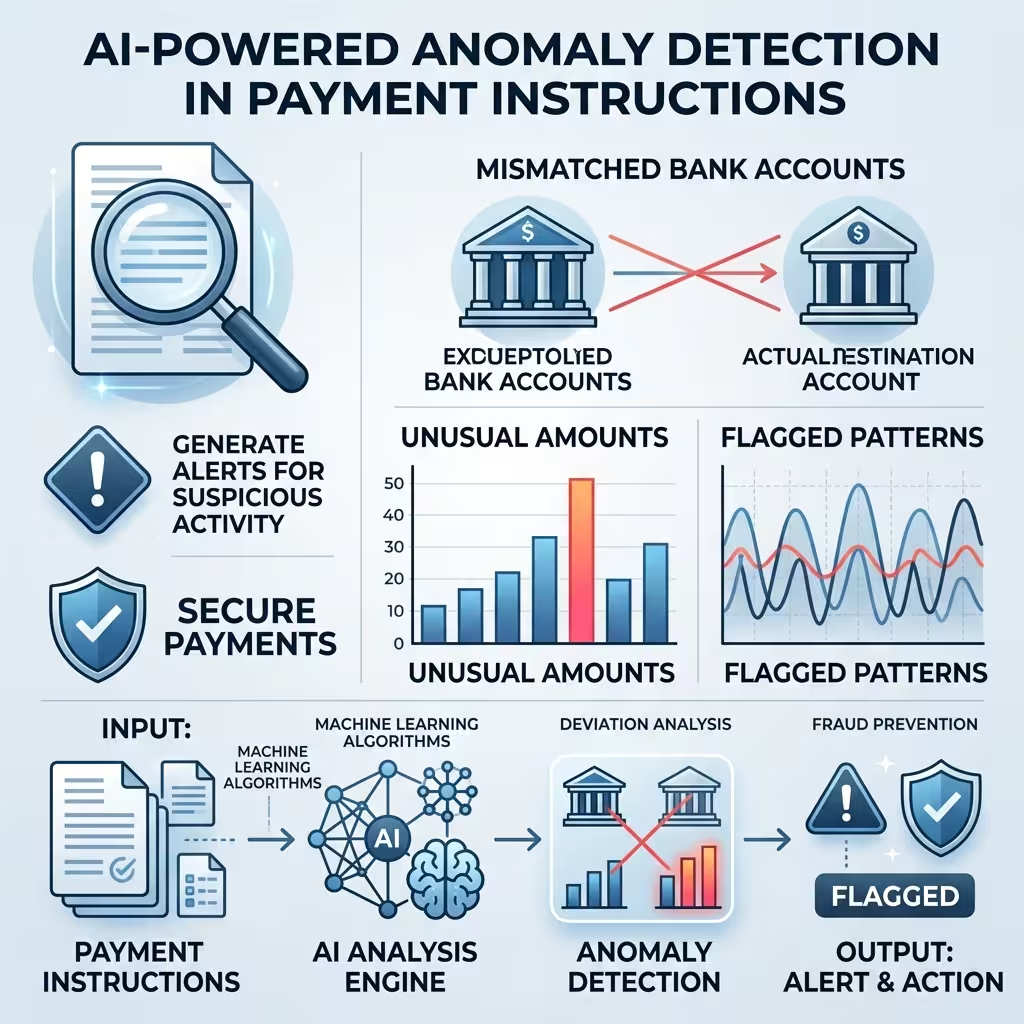

Fraud Moves Faster Than Any Manual Process

Business Email Compromise is the top fraud vector hitting treasury right now and I want to spend a minute on it because the scale is real — the FBI reports billions in BEC losses annually.

The attack is simple and fast. Someone impersonates a known vendor or executive, sends updated payment instructions to a new bank account, and waits. By the time manual review catches it — if it does — the money is already gone. Recovery rates are very low.

More approval layers don’t solve this. Approval layers need humans who are present. They fail on evenings, weekends, holidays. Every treasury team has a Friday-at-5pm window where the risk is real.

The answer is controls that run inside the payment creation process — invisible guardrails. While the payment is being built, the system checks in real time: Does this bank account match prior payments to this vendor? Is the amount pattern normal? Does something about this instruction break from established behavior?

If something flags, the payment stops before it leaves. Not after.

Boards are also pushing on explainability now. They don’t just want to know what the AI flagged — they want to know why. The platforms surviving governance review are the ones that show their reasoning clearly. The black-box systems are running into board-level resistance.

Platforms Worth Your Evaluation Time in 2026

No vendor has paid for placement here.

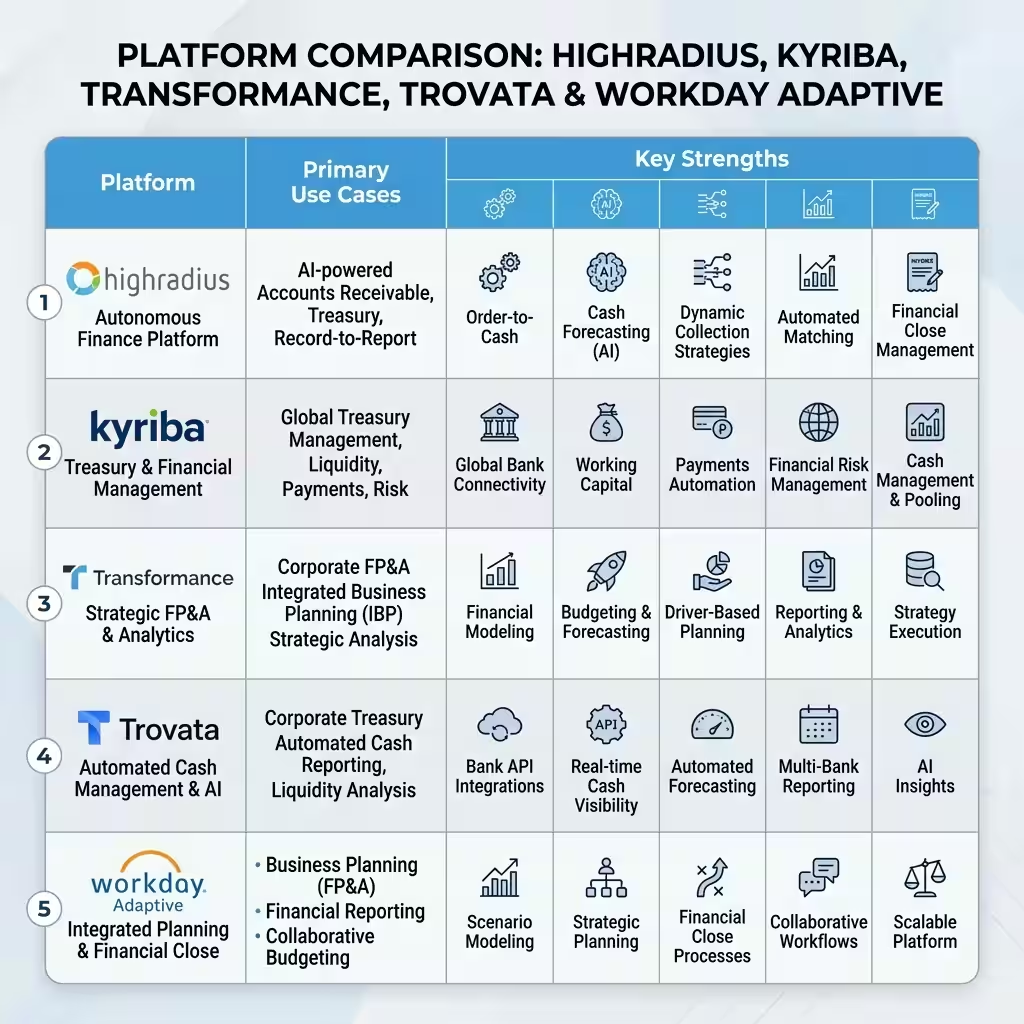

HighRadius is for large enterprises with complex AR operations. More than 100 machine learning models and seven specialized agents. The forecasting depth is strong — genuinely so, not just in marketing materials. Implementation is significant in scope, which reflects how deep the integration goes.

Kyriba leads on bank connectivity. Over 10,000 banking relationships, which matters when managing liquidity across a global treasury structure. Their Agentic AI handles hedging workflows directly. Best fit for multi-currency, multi-bank complexity.

Transformance is the one I’d send AR-heavy mid-market companies to first. Their CashPulse platform forecasts specifically from processed AR data — matched payments, active disputes, promise-to-pay commitments — not raw ERP extracts. That specific input difference produces a noticeably cleaner forecast for companies where AR complexity is the forecasting bottleneck.

Trovata is the fastest adoption path for mid-market teams. Cloud-native, API-first, search-style interface. If your team has real treasury expertise but limited IT support, Trovata closes the technology gap quickest without a six-month integration.

Workday Adaptive makes the most sense when treasury and FP&A need to be tightly linked — cash forecasts connected to revenue and headcount planning in ways standalone treasury platforms don’t offer.

Pick based on your actual problem. The platform that makes sense for a $10 billion enterprise with 40 banking counterparts probably isn’t the right call for a $100 million company with two.

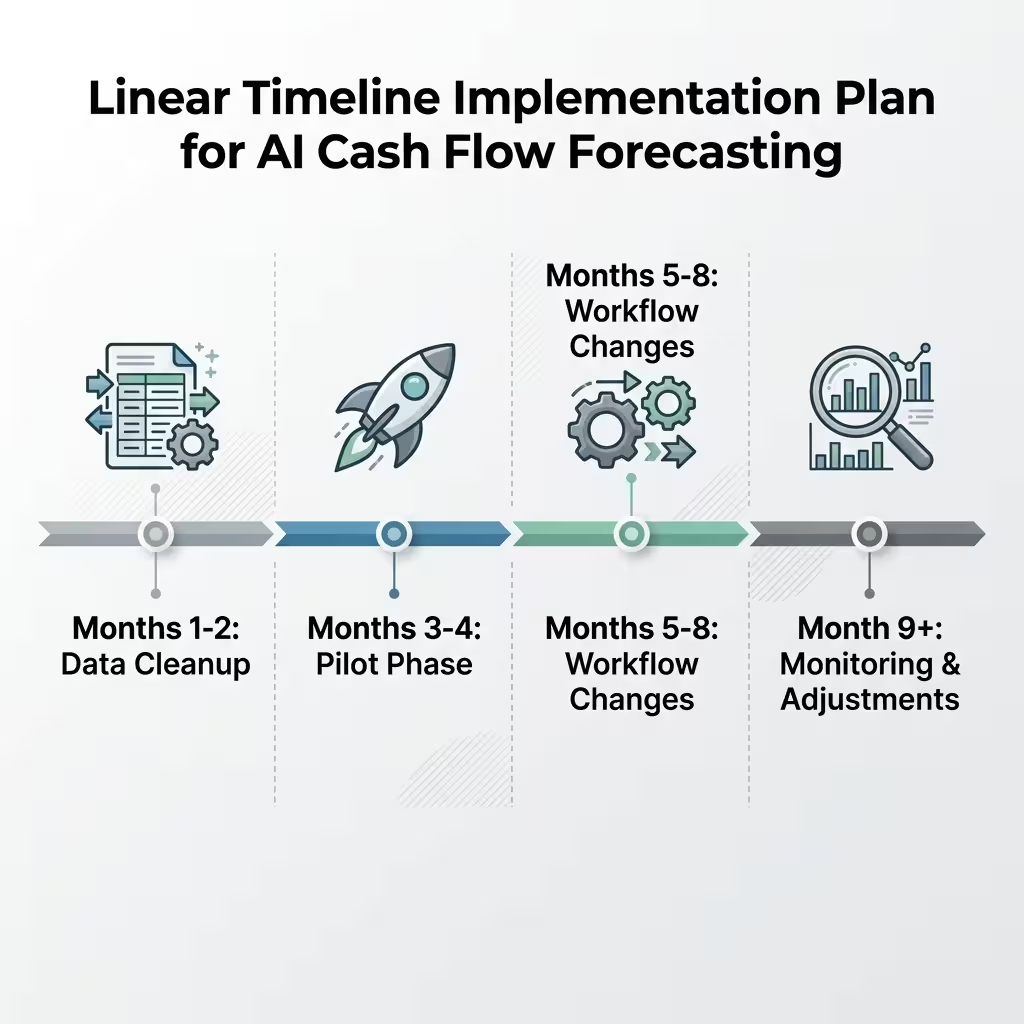

A Realistic Implementation Plan — Including the Part Most Teams Skip

Companies that waste money on AI treasury tools almost always share one mistake. They skipped the data foundation and went straight to the software.

An AI forecasting system running on corrupted AR data will be confidently wrong. It’ll miss your forecasts with more precision than your spreadsheet did. I’ve talked to teams this happened to. It’s a specific kind of demoralizing.

Months 1 and 2 — fix the data before you touch a platform. Audit your AR aging for completeness. Document your data lineage. Establish one source of financial truth across the organization. This step is slow and unglamorous. It’s also where most implementations quietly die.

Months 3 and 4 — pilot one use case only. Start with the 13-week cash forecast. Connect live bank feeds. Run the AI model alongside your existing model for four to six weeks without replacing anything yet. Compare outputs. Trust in a new system gets built by watching it be right repeatedly — not from a go-live announcement.

Months 5 through 8 — change how the team works, not who’s on it. Analysts move from building forecasts to validating AI outputs. Low-code tools on most platforms let treasury update rules and connectors without filing IT requests. That speed matters — finance should control its own automation.

Month 9 and beyond — watch for model drift. Business conditions change. Customer payment behavior shifts seasonally. The AI’s assumptions need periodic review to keep the accuracy numbers from slipping. This step gets skipped more than any other. It shouldn’t be.

The Regulatory Layer That Matters for U.S. Treasury Teams

The U.S. Treasury released the FS AI RMF — a sector-specific adaptation of the NIST AI framework covering 230 control objectives across the full AI lifecycle from procurement through ongoing monitoring.

For large enterprises, this is board-level governance documentation. For mid-market teams without dedicated AI governance staff, it’s more useful as a practical checklist — gives you the vocabulary to evaluate platforms before you commit.

The AI for Main Street Act and AI-WISE Act moved through Congress authorizing the SBA to provide training and technical support for smaller businesses adopting AI. The technology gap between Fortune 500 treasury teams and $50M companies has genuinely narrowed. SMEs using these tools are flagging cash flow risks weeks out instead of days out — which changes inventory decisions, payroll timing, and credit line management in ways that compound over a year.

People Also Ask – PAA’s

How does AI actually improve cash flow forecasting accuracy?

Real-time processed AR data replaces stale ERP exports. Individual invoice prediction replaces segment averages. Those two input improvements explain most of the accuracy gap — the model is just working from better, more current information.

What are the main benefits for corporate treasury teams?

Forecast accuracy is the headline — from roughly 60% manual accuracy on a 13-week horizon to 88-92% with AI. Behind that: scenario modeling you can run live during meetings, variance analysis that produces a board-ready narrative automatically, and fraud detection running inside payment workflows around the clock.

Which AI tools make sense for liquidity planning in 2026?

Depends on your setup. Large enterprise with complex AR: HighRadius or Kyriba. AR-heavy mid-market: Transformance. Mid-market fast adoption: Trovata. FP&A-integrated planning: Workday Adaptive. There’s no universal right answer.

What is predictive liquidity management?

Forecasting forward cash positions at the invoice and transaction level using AI — rather than building static models from aggregated historical data. Lets treasury teams make proactive calls on collections, disbursements, and borrowing instead of reacting to what’s already happened.

How long does implementation take realistically?

Three to six months from starting data cleanup to a fully running AI forecast. First real accuracy improvements typically show within 60 days of connecting live bank feeds to a pilot. Teams that skip data cleanup don’t save time — they add months.

The CFO who walked out of that meeting last October wasn’t being unfair. She needed a real answer. The tools available at that moment couldn’t produce one.

Those tools exist now. The treasury director I talked to afterward ended up switching platforms about eight months later. She told me her 13-week forecast is running above 89% accuracy. Her CFO hasn’t walked out of a meeting since.

That’s not magic. That’s what happens when the data feeding the model actually reflects what’s happening in the business right now instead of what was happening last Thursday.

If your forecasts keep missing and you’ve been blaming the data, the business units, or the ERP timing — worth asking whether the method itself is the real problem. Not the team. The process.

Disclaimer: This content is for informational purposes only and does not constitute financial, legal, or investment advice. Accuracy figures cited are drawn from published treasury research and vendor documentation. Your results will vary based on data quality, implementation choices, and your specific business. Evaluate any platform against your own requirements before purchasing.