The AI Wealth Revolution: How to Automate Your Path to Financial Freedom in 2026

May 2026

Nadia had three bank accounts, two investment apps, and no idea where her money was going.

She was a marketing manager in Chicago. Good salary. Every month she’d check her balance, feel stressed, tell herself she’d sort it out next weekend. She never sorted it out. The investing apps she’d downloaded all had different dashboards. Her 401k was somewhere she logged into once a year. She had a budget spreadsheet that hadn’t been touched since February.

She wasn’t bad with money. She was just buried under it.

Then she started using AI personal finance tools. Not to replace thinking about money. To stop thinking about it every waking hour. In three months, her accounts were connected, automated, and running on their own.

Most financial articles skip the actual experience of this. The tools that work. The traps that don’t. That’s what this covers.

Quick note: nothing here is financial advice. These are tools, data, and observations. Talk to a licensed professional before making big decisions.

Where AI and Money Actually Are in 2026

The numbers first. They matter.

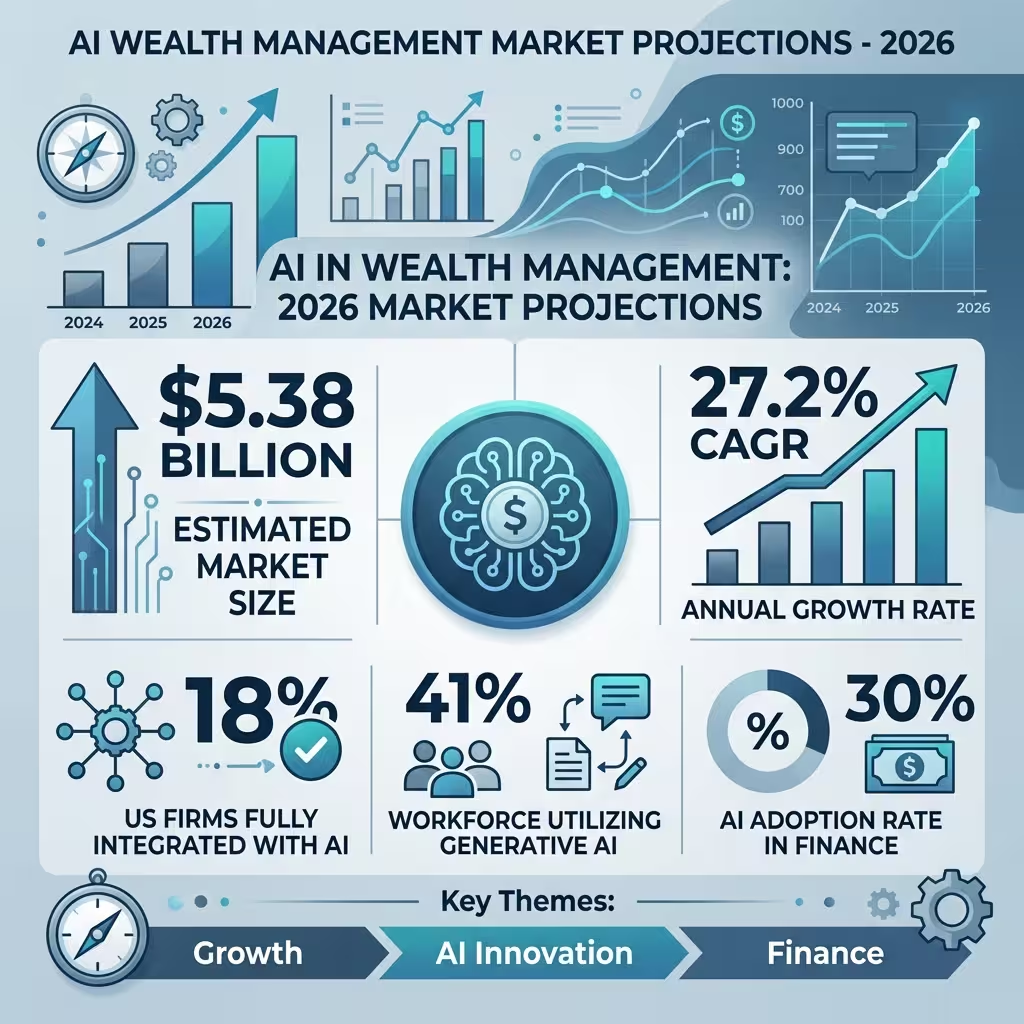

The AI wealth management market hit $5.38 billion this year. It is growing at 27.2% per year. About 18% of US firms have fully integrated AI. And 41% of the workforce uses generative AI for job-related tasks. In finance, AI adoption sits at 30%. Only professional services is higher at 33%.

This is not a trend heading somewhere. It has already arrived. The tools exist and work. People using them are getting real advantages over those who aren’t.

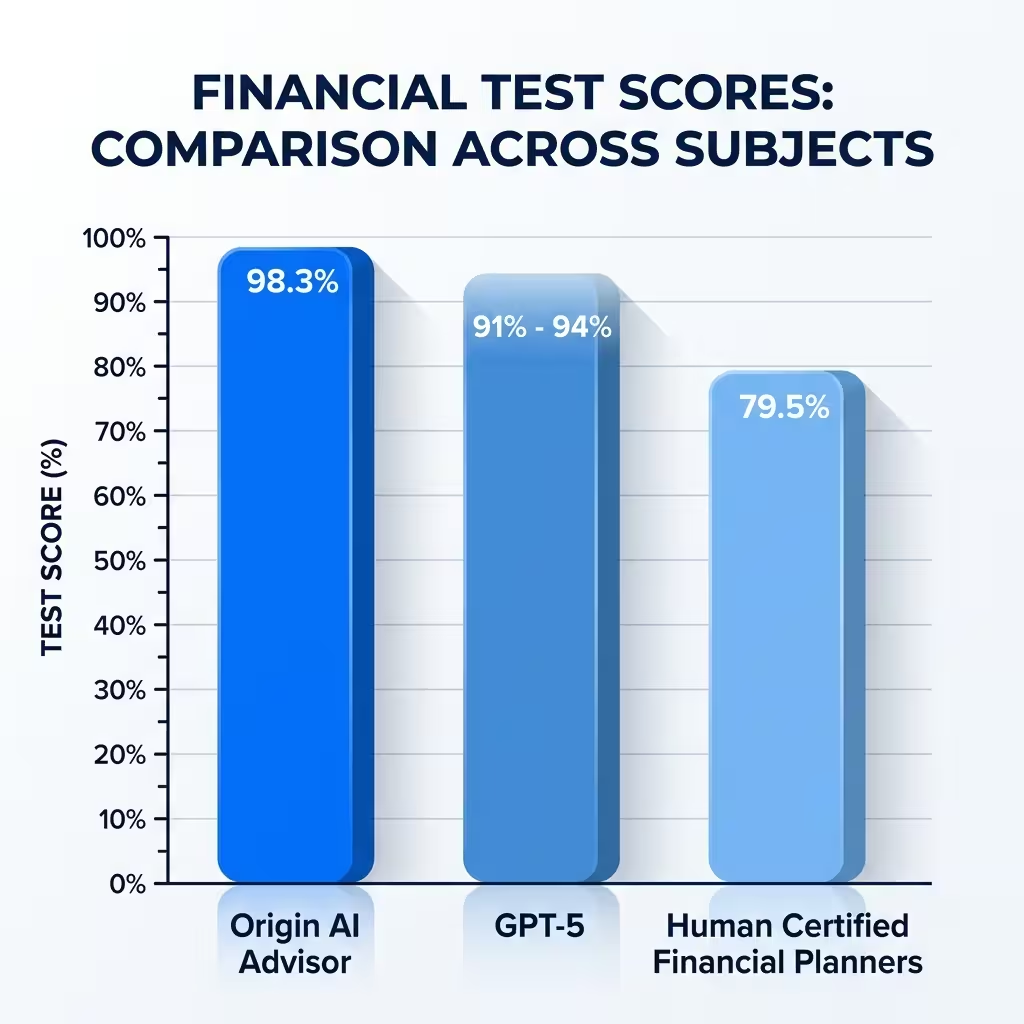

Here’s the specific advantage. Origin AI Advisor scores 98.3% on CFP-style financial tests. The average human Certified Financial Planner scores 79.5%. Standalone tools like GPT-5 come in at 91% to 94%. On technical financial questions, advisor-grade AI is more accurate than most human advisors.

That doesn’t mean humans are done. It means the job split. AI handles technical accuracy. Humans handle the stuff that’s hard to model — divorces, inheritances, family estate dynamics, emotional decisions. Understanding that split before you set up your system saves a lot of confusion later.

The OBBBA: Why 2026 Is Different

Before tools, a word on why right now matters more than previous years.

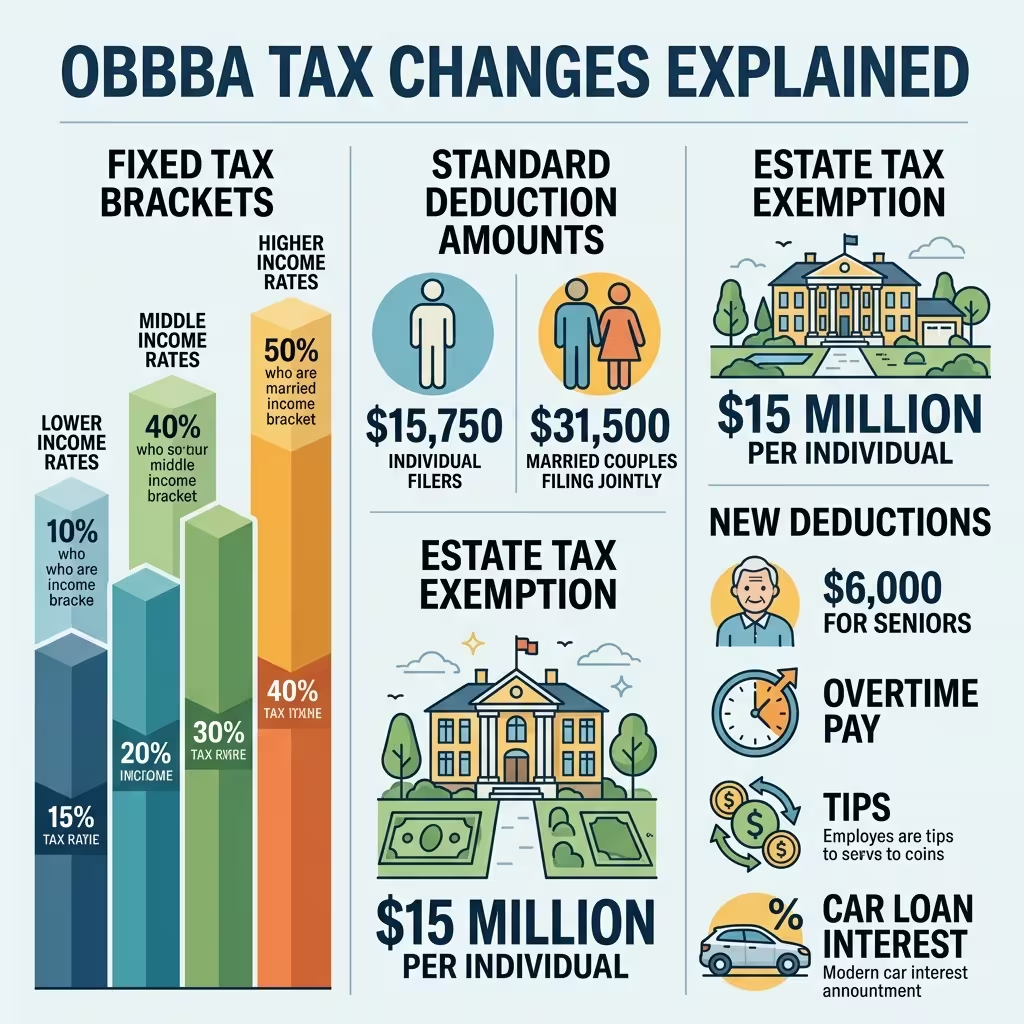

The One Big Beautiful Bill Act was signed on July 4, 2025. It made the 2017 Tax Cuts and Jobs Act permanent. Seven income tax brackets. Now fixed. The standard deduction landed at $15,750 for single filers and $31,500 for married couples filing jointly. Estate tax exemption went to $15 million per individual.

Here is why that matters for smart financial planning. AI tools work better when tax rules don’t change. Every time brackets shift, optimization models have to recalibrate. With the OBBBA, that problem went away. Stable rules mean better long-term automated strategies. The planning window that opened in mid-2025 is still wide open.

New deductions are also running that most people don’t know about. If you’re 65 or older, you get an extra $6,000 deduction off your taxable income through 2029. Income phase-out applies — MAGI under $75,000 single or $150,000 joint. Overtime pay has a deduction capped at $12,500 for single filers. Tips are exempt up to $25,000 per year. Car loan interest on US-assembled vehicles is deductible up to $10,000.

None of this is complicated. But most people miss all of it. A good AI financial tool catches every deduction automatically without you hunting through the tax code.

The Tools That Work — And What Each One Actually Does

I want to be direct here because most reviews lump everything together as if all fintech apps are the same. They are not.

Origin is the all-in-one option. It connects spending, investing, and tax planning in one dashboard. It uses what it calls multi-agent reasoning. That means multiple AI processes run at the same time across your accounts. You type something like “optimize my portfolio for this year’s tax brackets” and the system rebalances while modeling the tax hit at the same time. That is what agentic AI means. Not one automated task. Several things handled together at once.

Wealthfront is the best for automated tax optimization. Its direct indexing feature holds individual stocks instead of ETFs. That gives the AI far more chances for tax-loss harvesting. It reportedly captures two to four times more losses than ETF-based systems. On a $500,000 portfolio, that works out to 1.5% to 2.5% in annual tax alpha. Real money. Just from smarter tax moves.

Betterment is the cleanest option for W-2 workers who want goal-based investing with no complexity. Set a goal, set a timeline, the platform handles it. Not the most powerful tool on this list. But the easiest to start with.

For specific problems there are others. Cleo is best for conversational budgeting. You chat with it about spending and it gives habit-based feedback. Rocket Money finds and cuts recurring subscriptions you forgot about. Monarch does household cash flow forecasting with predictive analytics. Undebt.it uses machine learning in finance to model debt payoff and compare Snowball versus Avalanche with real numbers. PocketGuard gives you a live “Safe to Spend” number to stop lifestyle creep before it happens.

Each one solves a specific problem well. The mistake most people make is downloading five at once. They end up with the same fragmentation they started with.

How to Build Your Setup Based on Portfolio Size

Here is a plain framework. Portfolio size drives the right approach.

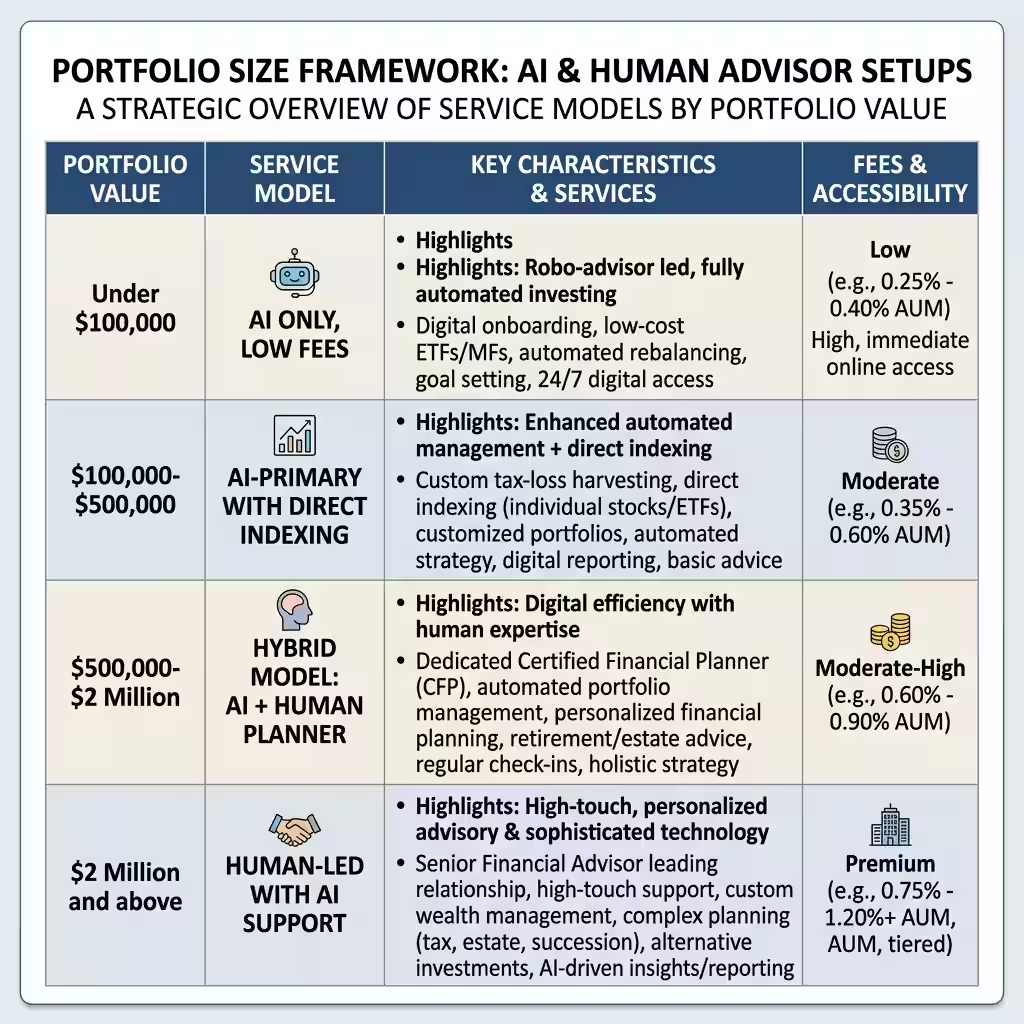

Under $100,000: Use AI only. Low fees matter most at this stage. Fidelity Go or Betterment charge near zero. Start with one platform. The point right now is building the habit and keeping costs down.

$100,000 to $500,000: Go AI-primary with direct indexing. This is where Wealthfront earns its fee. Tax optimization at this level starts producing real returns. You want a platform with solid data encryption and security. Not just a free budget app.

$500,000 to $2 million: Hybrid model. AI handles daily management and tax moves. One flat-fee human planner does an annual review. The planner catches what the AI misses — RSU vesting, business income, estate questions. AI runs everything in between.

$2 million and above: Human-led with AI support. Multi-generational estate planning with trusts and family dynamics needs a human advisor. AI helps but does not lead.

Agentic AI — What Changed and Why It Matters

People using fintech apps in 2023 were using automation. A recurring transfer. A scheduled rebalance. Set it, forget it.

That is not what 2026 looks like.

Agentic AI handles multi-step tasks across different platforms without being told each step. You say “optimize for tax efficiency” and the system checks your portfolio, finds losing positions, runs the harvesting, models your bracket impact, and updates your projection. No menu clicking. You just said what you wanted.

The Federal Reserve tracks AI adoption by sector. Finance and professional services lead all others. What the data shows is that AI use is concentrated in cognitive, high-value work right now. Simple data entry got automated years ago. What’s happening now is that systems are starting to reason across financial contexts — across accounts, platforms, and tax rules — rather than just executing one task at a time.

The gap between people using these tools and those who aren’t is compounding. Someone with direct indexing and automated tax-loss harvesting is getting 1.5% to 2.5% more per year than someone with the same portfolio in a standard ETF. Over 20 years, that is a lot of money. Not from picking better stocks. From smarter tax management running in the background.

The Risks That Don’t Get Enough Attention

The upside gets all the coverage. The risk side usually gets one paragraph that says “be careful.” That’s not enough.

Vishing is the fraud I’m most worried about in 2026. AI-powered voice synthesis can clone a person’s voice from a short audio clip. Scammers call pretending to be a family member or company executive. They create urgency. They get people to authorize wire transfers. These attacks run at scale now — not as rare, individual scams but as industrialized operations. The cloned voice sounds exactly like someone you know. You cannot tell the difference.

The “All Green” problem makes this worse. Normal fraud detection flags unusual behavior. But if a real customer is tricked into making a transfer that looks legitimate, the system sees a clean, authenticated transaction. No alert. The money is gone before anyone checks.

Shadow AI adds another layer. 59% of organizations have employees using unapproved AI tools. Those tools often touch financial data. Without proper data encryption and oversight, sensitive information flows through systems with no adequate security controls.

Practically: stick to platforms with recognized security standards. NIST AI RMF compliance is one marker worth checking. Ask your financial tool provider how the AI makes its decisions. If they can’t explain it clearly, that is a problem.

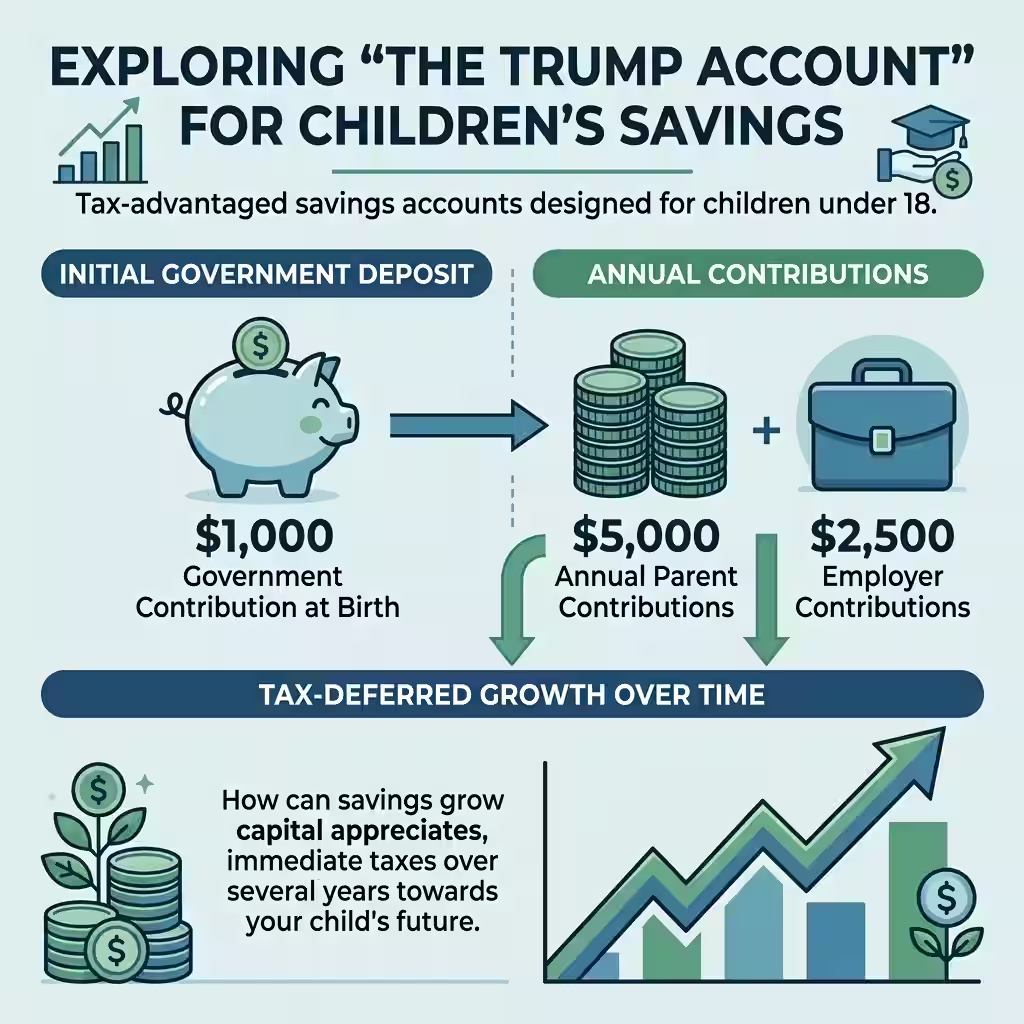

The Trump Account — Most People Don’t Know This Exists

One item from the OBBBA that hasn’t gotten enough attention.

Trump Accounts are tax-advantaged savings accounts for US citizen children under 18. For kids born between 2025 and 2028, the federal government deposits $1,000 to open the account. Parents can add up to $5,000 per year after that. Employers can contribute up to $2,500. The money grows tax-deferred. At 18, distributions are taxed at ordinary income rates.

The math is simple. $1,000 from the government, invested at 7% annual return from birth, reaches about $3,400 by age 18. Add parent contributions on top of that and it becomes a real starting point for a young adult.

The estate tax change is worth noting too. Exemption is now $15 million per person, $30 million for couples. A “no clawback” provision means gifts made under those limits are permanently protected. If you’re anywhere near that threshold, the window to restructure is open and the rules are stable right now.

People Also Ask – PPA’s

How do I use AI for personal wealth management in 2026?

Pick one platform. Not five. Connect your accounts to Origin or Wealthfront. Let the AI run its first analysis on your portfolio, tax exposure, and spending. Then work through the top two or three recommendations. Most people see a real improvement just from connecting accounts and letting the AI find what they were missing.

What are the best AI tools for financial freedom?

For overall management: Origin. For tax optimization: Wealthfront. For goal-based investing: Betterment. For debt payoff modeling: Undebt.it. For daily budget limits: PocketGuard or Cleo. For killing forgotten subscriptions: Rocket Money. Pick based on your biggest problem, not the best-looking interface.

Is AI financial advice more accurate than a human CFP?

On technical questions, yes. Origin AI Advisor hits 98.3% on CFP benchmarks. Human CFPs average 79.5%. But AI does not handle big life transitions well. Divorce. Inheritance. Business sales. Family estate complications. A hybrid model — AI for day-to-day, human for major events — is what makes sense above $500,000.

How safe is my financial data with these tools?

It varies. Check for NIST AI RMF compliance, clear data encryption practices, and explainability — can the platform tell you why it made a decision? If the answer is no, look elsewhere. Shadow AI is a real exposure. Don’t use tools that haven’t been vetted by your employer or financial institution.

What is the OBBBA and how does it affect my taxes?

Signed July 4, 2025. Made the 2017 Tax Cuts and Jobs Act permanent. Your brackets are now fixed. New deductions include $6,000 for seniors 65 and older, overtime and tips exemptions, and car loan interest. AI tax tools updated their models for these changes immediately. If you’re using an older platform, check that it reflects current law.

What Nadia Did

She picked Origin.

Connected the three bank accounts, the 401k, and the two investment apps she’d ignored for months.

The AI found three things in the first two days. A subscription she’d forgotten about — $240 a year. A tax-loss harvesting move in her brokerage. A deduction she had missed.

She did not become a finance expert. She did not start reading investment newsletters. She spent 90 minutes on setup. Then the automated budgeting ran on its own.

Six months later, her net worth was up, her taxes were lower, and she had stopped feeling that low-grade financial dread every time she checked her phone.

That is the real story of AI personal finance in 2026. Not a revolution. Not overnight money. Just the slow, quiet removal of friction that had been costing her money every single month.

The tools are there. The question is whether you set them up.

Disclaimer: General information only. Not financial, legal, tax, or investment advice. All figures and projections are based on available public data and are not guarantees. Consult a licensed financial professional before any investment or tax decision. The author and publisher accept no liability for outcomes based on this content.