The Death of the Wealth Manager? How Generative AI is Leveling the Playing Field

May 2026

Sofia had been paying the same financial advisor $2,800 a year since 2021.

She’s a marketing director in Chicago. Mid-30s. Good income. Some investments she didn’t fully understand. The advisor called twice a year. Sent quarterly reports. Made her feel like things were under control.

Then her company rolled out an AI financial tool for employees. She tried it one Thursday evening. Not for any urgent reason — mostly curiosity.

The AI found a $3,600 tax-loss opportunity her advisor had never flagged. It identified a concentration risk she’d been carrying without knowing. It built a financial model specific to her: her actual cash flows, her liabilities, her tax position. Not a general template. Her numbers.

She sat with that for three days. Then she called her advisor.

He told her the portfolio was doing fine.

That gap right there — between what she got from the AI in 18 minutes and what she got from her advisor in five — that’s what generative AI wealth management means in practice. The technology didn’t replace her advisor. It just made clear what the advisor was and wasn’t delivering.

Quick note: nothing here is financial advice. These are observations and market data. Talk to a licensed professional before making big financial decisions.

What “Leveling the Playing Field” Really Means

The wealth management AI market hit $243 billion in 2025. That number matters less than what it unlocked.

Services that used to require a $2 million account minimum at a private bank are now available to anyone with the right app. Multi-state tax modeling. Estate document analysis. Personalized asset allocation. Continuous portfolio optimization. None of these are behind a paywall anymore. The cost of delivering them dropped to near zero.

Research from NeurIPS 2026 showed something concrete. Large language models that processed public financial media — earnings transcripts, analyst calls, Bloomberg commentary — helped retail investors build portfolios that beat the S&P 500 in backtests. The institutional advantage was never intelligence. It was access to data, analysts, and time. AI closes that gap.

Economists have a term for the problem AI solves here: bounded rationality. The idea that people make worse decisions when they’re short on time, information, and mental bandwidth. An AI tool removes those limits. That’s what personalized financial advice for regular people actually looks like now.

Generative AI vs. Agentic AI — What Changed in 2026

Most people still picture AI financial tools as chatbots. Ask it a question, it answers. That’s generative AI. That’s the 2024 version.

What’s running on leading platforms now is different.

Agentic AI doesn’t wait for a question. It acts. These systems reason across multiple platforms at the same time. They plan and execute multi-step tasks without a human telling them each step. One instruction — “prepare my client review” — and the system pulls the data, updates the CRM, flags compliance issues, drafts the agenda, and sends the summary. The advisor reads the output instead of building it.

For advisors, this compresses what they call “invisible labor.” Meeting prep. File review. Data extraction. Report writing. The things that eat hours without clients ever seeing the work. Industry figures put the productivity gain from this compression at 25% to 40%. That’s the cognitive dividend — time given back for the work only humans can do.

For clients, the change is a financial digital twin. A live model of their specific financial situation that updates continuously. Not a static plan reviewed once a year. A model that runs in real time and adjusts when things change.

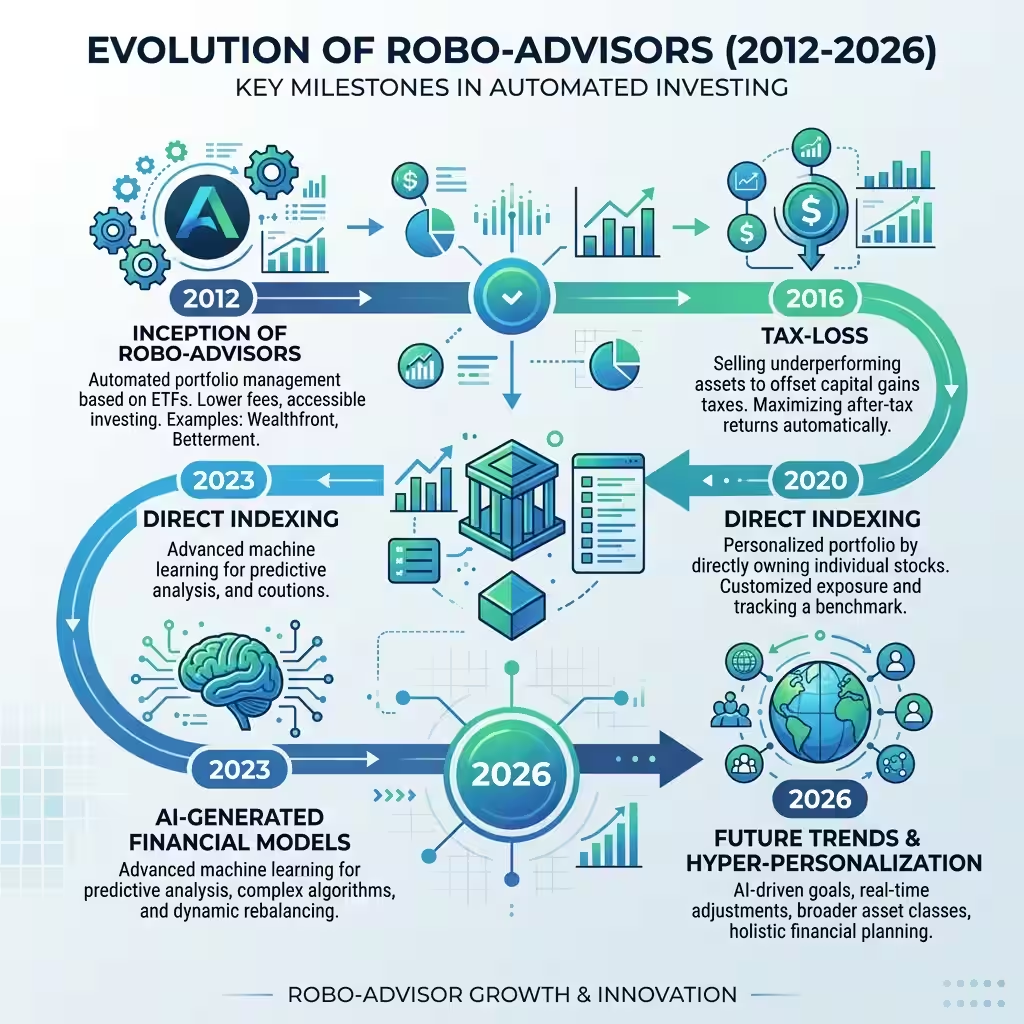

Robo-Advisor 2.0 — Not the Same Product

The original robo-advisor was simple. Answer eight questions, get put in index funds, rebalance once a quarter. Betterment and early Wealthfront. Useful in 2012. Limited everywhere that mattered.

What’s called a robo-advisor today is a completely different category.

Automated portfolio management now includes direct indexing. Instead of buying an ETF, the system holds the individual stocks inside the index. That gives it far more shots at tax-loss harvesting. Platforms running this approach capture two to four times more tax losses than ETF-based systems. On a $500,000 portfolio, that’s 1.5% to 2.5% per year staying in your account instead of going to the IRS.

That’s just the tax piece. Tax filing, estate planning analysis, multi-goal modeling, values-aligned investing — these are now standard features on platforms that cost a fraction of a traditional advisor fee.

GPT for finance isn’t a concept anymore. It’s a product category with benchmarks.

Charles Schwab launched Portfolio Insights in 2026. Retail clients get plain-language explanations of why their portfolio moved, with news and research baked in. Vanguard’s Expert Insights gives advisors AI-generated stress tests against extreme market conditions. Betterment’s AI Account Recommender explains every suggested account adjustment in plain language.

None of this is what a robo-advisor was. The name stuck but the product changed.

The Human Advisor Isn’t Gone — The Business Model Is Under Pressure

I want to be direct here because most coverage gets this wrong in one direction or the other.

AI is better than human advisors at technical financial work. That’s documented. Advisor-grade AI systems score 98.3% on CFP-style professional benchmarks. Human CFPs average 79.5%. On calculation, optimization, and pattern recognition, the machine wins.

The practical result is what industry analysts are calling the “SaaSpocalypse” — the collapse of fees for services that AI can now deliver for near-zero cost. Basic tax projections. Routine rebalancing. Generic asset allocation. These are being commoditized. The fee justification for that work is weakening fast.

What AI doesn’t do: manage the emotional side of big money decisions.

When a client’s retirement account drops 22% in a market shock, they don’t primarily need updated projections. They need someone who knows them. Someone who can hold the situation steady while they process it. Someone who stops them from making a panic move they’d regret for 20 years. That’s behavioral coaching. No algorithm replaces it.

70% of young investors expect at least monthly contact with their advisor. 92% say personal values matter in their investment choices. 43% want impact investments factored in. These things don’t get handled by a dashboard. They need real, ongoing human contact.

The industry consensus right now is not “AI replaces advisors.” It’s “advisors who use AI will replace advisors who don’t.” There are 40% of current advisors retiring in the next decade. The projected growth in relationships that need coverage is 28% to 34%. The numbers only work if AI handles the technical volume.

The Regulatory Picture — Shorter Than You Think

The SEC made AI a top examination focus in 2026. They look at three things: how firms evaluate AI before using it, how they monitor what it produces, and whether their security policies cover AI-specific risks.

AI washing got expensive. The SEC collected $400,000 in combined civil penalties from firms like Delphia and Global Predictions for overstating their AI capabilities. The Nate, Inc. case went further — $42 million in alleged fraud after the CEO claimed the app used neural networks when real people were doing the work offshore.

Recordkeeping changed. Under SEC Rule 204-2, if an AI prompt leads to an investment recommendation, both the input and the output get archived. The AI’s reasoning is now auditable. That’s a meaningful shift for any firm using AI to generate client advice.

Smaller RIAs managing under $1.5 billion had a Regulation S-P compliance deadline of June 3, 2026. They have to verify that their AI vendors don’t use client data to train public models. Using free tools like ChatGPT with client information is a confidentiality failure under this standard.

For individual investors: hallucination rates in AI financial tools run 3% to 27% depending on the question type. A confident-sounding wrong answer and a correct answer look identical. For high-stakes decisions, use purpose-built financial AI with deterministic engines, not a general chatbot.

People Also Ask – PPA’s

Will generative AI replace financial advisors?

Partially, yes — for the technical work. Portfolio construction, tax optimization, and routine rebalancing are being commoditized. Human advisors who focus on behavioral coaching, major life transitions, and complex family governance still provide something AI can’t. The hybrid model — AI for the technical layer, human for the judgment layer — is the working answer in 2026.

How do I use ChatGPT for custom investment advice?

Carefully. General LLMs are useful for explaining concepts and testing your own thinking. They are not designed for mathematical precision in financial models. Hallucination rates of 3% to 27% in financial contexts mean wrong answers look convincing. For real investment decisions, use a purpose-built financial AI platform with verified data sources — not a general chatbot.

What is robo-advisor 2.0 and what makes it different?

The original robo-advisors put you in index funds and rebalanced quarterly. Today’s platforms add direct indexing, continuous tax-loss harvesting, AI-generated financial models, multi-goal planning, estate planning analysis, and values-based investing. Schwab, Vanguard, and Betterment all launched new AI-integrated features in 2026. The name is the same. The product is not.

Is it safe to use AI for financial planning?

For personal use, the risk is accuracy rather than regulation. Hallucination rates are real and not always obvious. For regulated firms, using public AI tools with client data creates compliance exposure. Purpose-built platforms with tenant isolation and SOC 2 Type II certification handle data correctly. Free general tools often don’t.

Where Sofia Is Now

She didn’t cancel her advisor right away. She waited another quarter.

On the next call, she asked pointed questions. About the tax opportunity. About the concentration risk. He had good answers. He knew things about her family situation and her specific goals that the AI model didn’t carry.

She renegotiated the fee. Kept him for one deep session per year — the big decisions, the life events, the moments that need a person. The AI handles the rest.

She pays less now. Gets more coverage. Stopped dreading the twice-a-year calls where someone tells her things are fine.

The wealth manager isn’t dead. The version that charges high fees for work a machine now does faster and better — that version has a problem.

About the Author James Whitfield covers AI in wealth management, automated portfolio management, and fintech. He has written about investment platforms and regulatory trends for nine years.

Disclaimer: General information only. Not financial, investment, or legal advice. All benchmarks and projections are based on public data and are not guarantees. Consult a licensed professional before any investment or planning decision. The author and publisher accept no liability for outcomes based on this content.