Set It and Forget It: The Secret to Using Predictive AI for Hands-Off Saving

Written May 2026

Priya had been “about to start saving” for two years.

Not because she was bad with money. $52,000 a year. Low debt. She actually knew she should have an emergency fund — she’d read enough financial content to know the three-to-six-month rule cold. The knowing was never the problem.

The problem was the moment.

Every time she planned to transfer money to savings, something else came first. A bill. A birthday dinner. A car repair. Or nothing — just the end of the month arriving with less money than she expected and no transfer made.

She tried budgeting apps twice. Both times she set them up, felt briefly organized, and stopped checking them after two weeks.

Then a friend told her about Tilt. She set it up in 20 minutes on a Sunday afternoon. Connected her checking account. Set a savings goal. Didn’t touch it again.

Four months later she had $1,100 in her emergency fund. She hadn’t manually transferred a single dollar.

That’s the actual story of predictive AI for savings in 2026. Not a motivational system that helps you want to save more. A system that saves for you when you’re not thinking about it, using data you’d never process yourself.

Nothing here is financial advice. These are tools, data, and observations. Talk to a licensed professional before making major financial decisions.

Why Willpower-Based Saving Doesn’t Work

Most financial advice is built around the idea that if you understand why saving matters, you’ll do it. More discipline. Better habits. Track your spending. Build awareness.

The research doesn’t really support this.

The reason most people don’t save consistently isn’t ignorance. It’s timing. The decision to save keeps landing at the wrong moment. Money already spent. Balance already lower than expected. Something else already took priority. By the time the saving decision arrives, it’s already lost.

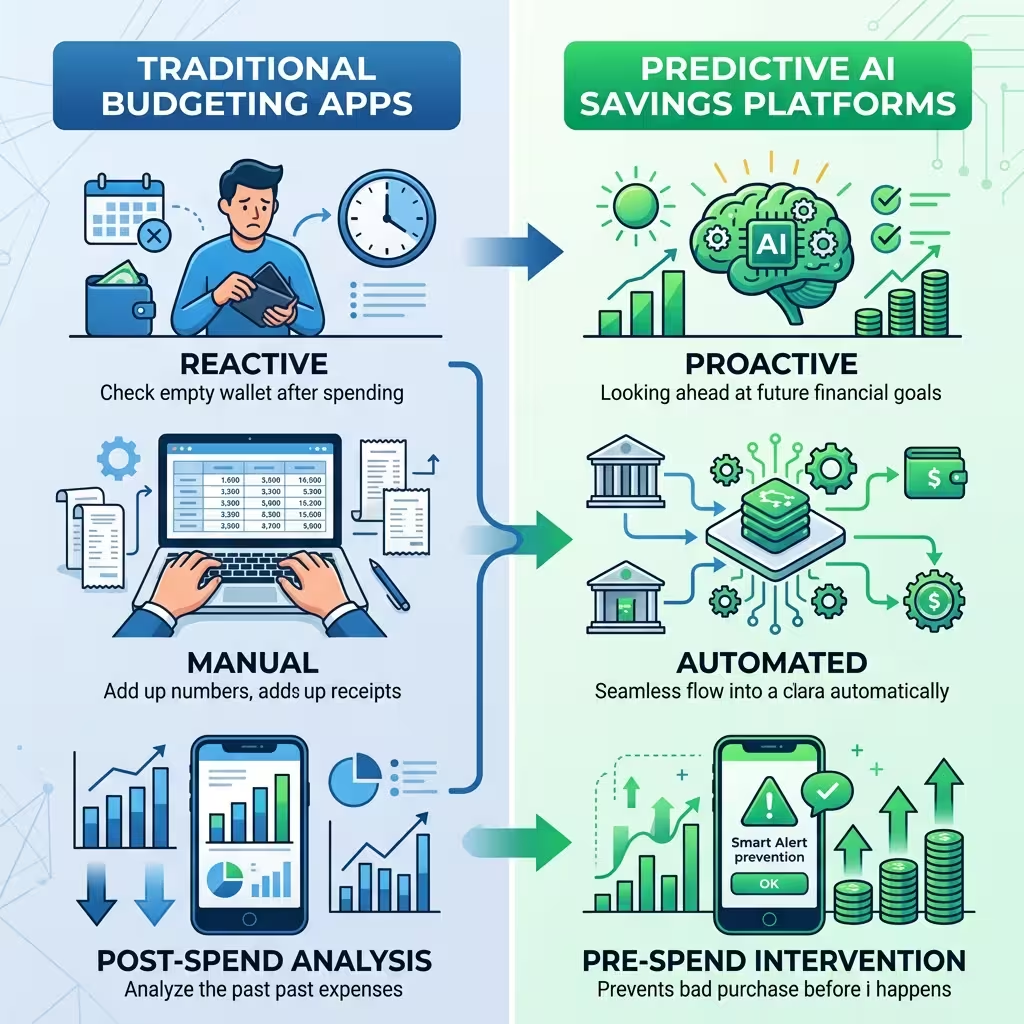

Traditional budgeting apps made the problem worse in one specific way. They told you what happened after it happened. You overspent on food in March. You see the chart in April. The information is accurate and completely useless. The money is already gone.

Behavioral finance AI works differently. It doesn’t show you what happened. It intervenes before the spending occurs.

Platforms using behavioral financial planning AI — Tilt and Oportun are the two built for this specifically — watch what comes in and what goes out. Salary deposits. Subscription renewals. The electric bill that hits the same week every month. All of it. Over time, the model learns your rhythm. Then it finds the gaps — the days when your balance has room — and moves money to savings in those gaps, automatically.

The psychology here matters. When saving happens before the money is available to spend, you don’t feel the loss. A $40 transfer to savings on a Wednesday afternoon, when your account has space, costs you nothing emotionally. A $40 transfer you decide to make at the end of the month, when your account is running low, feels like a sacrifice.

Same amount. Different timing. Completely different behavior.

How Cash Flow Forecasting Makes This Work

Predictive AI for savings doesn’t just look at today’s balance. It builds a forward model.

Cash flow forecasting means the AI scans your incoming and outgoing money — salary deposits, recurring subscriptions, typical bill cycles, seasonal spending patterns — and builds a rolling picture of what your finances will look like over the next 30 to 60 days.

From that model, the platform finds the safe windows. The moments when moving $20 or $40 to savings won’t cause an overdraft or leave you short before a bill lands. The transfers happen then — quietly, without notification, in amounts that don’t hurt.

This is completely different from a scheduled transfer. If you set up a $200 transfer for the 15th of every month, it doesn’t know your car insurance just renewed on the 12th. Cash flow forecasting knows. It’s been watching long enough to build the pattern.

The result is emergency fund automation that adjusts to your actual financial reality rather than an ideal version of it.

Priya had tight months. Tilt barely moved anything in those months — maybe $15. Then she had a good paycheck and lower spending one week, and it moved $80. She never decided either number. The system read the balance and acted accordingly. Eight months in, the average worked out to about $275 a month without her ever sitting down and choosing to save $275.

Round-Up Savings — The Slowest Way That Actually Works

Not everyone starts with a platform like Tilt. Some people start with the smallest possible entry point.

Round-up savings is the version of automated micro-investing most people already understand. Every debit card purchase gets rounded up to the nearest dollar. The change goes into savings or an investment account.

Buy coffee for $4.60. The app rounds to $5.00. The $0.40 goes to savings without you doing anything. Every purchase, same process, running in the background.

Those individual amounts feel meaningless. You’re right — they are individually meaningless. But the behavioral effect is not. Round-up savings removes the decision entirely. You spend money the way you normally do. The accumulation happens as a side effect.

Acorns pioneered this model and still does it well. Chime and Dave both have versions. For someone who has never maintained a savings habit before, this is the lowest-friction starting point. The gap between having $0 in savings and having $300 in savings is often just a matter of which system gets started first.

One year of consistent round-ups — across a normal spending pattern — typically generates $300 to $600. Not enough to retire on. Enough to start the psychological shift from “I don’t save” to “I save automatically.”

Psychological Triggers — What Makes People Spend Before They Think

Here’s the part behavioral finance AI is specifically designed to address.

Impulse spending is not irrational. It’s a predictable response to how you’re feeling at a specific moment. Bored at 10pm. Stressed after a bad meeting. Feeling good after a Friday paycheck. These states lower the threshold for an unplanned purchase. They move faster than any financial reasoning.

Traditional financial tools do nothing with this. They see the transaction after it clears and put it in a category. Behavioral financial planning AI tries to intervene before the transaction completes.

Platforms like Whistl use what they call a “pre-spend save” mechanism. When the AI sees a user about to make a discretionary purchase, it prompts a savings micro-transfer first. Not a block. A pause. A split second where the person makes a tiny financial choice before the spending goes through. That pause is the whole product.

The NLP-driven conversational interfaces in these apps are part of the same design logic. Instead of a dashboard, you get a coaching dialogue. Instead of a chart, you get a question: “You’re about to spend $45 at Target. Want to save $5 first?” That phrasing — a choice, not a restriction — changes the psychology.

Smart saving algorithms are built around this. Systems that restrict produce anxiety. People avoid the app, override the limits, and eventually delete it. Systems that offer choices produce follow-through. The best platforms in 2026 understand that the emotional path to saving has nothing to do with guilt or willpower. It just has to feel like your decision rather than someone else’s rule.

How to Build an Emergency Fund Using Predictive AI — Step by Step

This is the specific question most people come to these tools with. Here’s how to actually do it.

Step 1: Choose the right platform for where you are now.

If you’ve never saved consistently: start with Acorns or Chime. Connect your debit card, turn on round-ups, and let it run. Don’t touch the account for 90 days.

If you have inconsistent income or variable expenses: use Tilt or Oportun. These platforms are built specifically for variable cash flows. They won’t try to move $200 on a week you can’t afford it.

If you want the full behavioral coaching layer: look at Cleo or PocketGuard. These add conversational prompts and real-time spending limits on top of the savings automation.

Step 2: Set a specific goal, not a general intention.

“Build an emergency fund” is a category. “Save $1,000 by September 15” is a target the AI can work with. Most platforms let you set a named goal with a target amount and a date. The algorithm builds the transfer schedule backward from that target.

Step 3: Connect only accounts the AI needs.

For cash flow forecasting to work, the platform needs read-only access to your main checking account — the one where income arrives and bills leave. It does not need access to credit cards, investment accounts, or savings accounts you don’t want it to touch. Most platforms use APIs like Plaid that provide read-only access only. They cannot move money out of accounts that aren’t explicitly connected.

Step 4: Leave it alone for 60 days.

This is the step most people skip. They set up the automation and then start manually adjusting it. That defeats the purpose. The forecasting model needs time to learn your actual spending patterns. The first month is calibration. The second month is when the transfers start to feel right.

Step 5: Review once a quarter.

Not every week. Not every day. Once a quarter, look at the total saved, check that the transfers aren’t conflicting with any bills, and adjust the target if your income or expenses changed significantly. That’s it.

Automated saving strategies for low income specifically depend on steps 1 and 4. Platforms like Oportun are built to work with lower and more variable incomes. They use smaller, more frequent transfers instead of larger monthly ones. $8 one week, $12 the next, $5 the week after. The cumulative total is the same. The individual transfers don’t create financial stress.

The Broader AI Picture — What’s Happening at the Platform Level

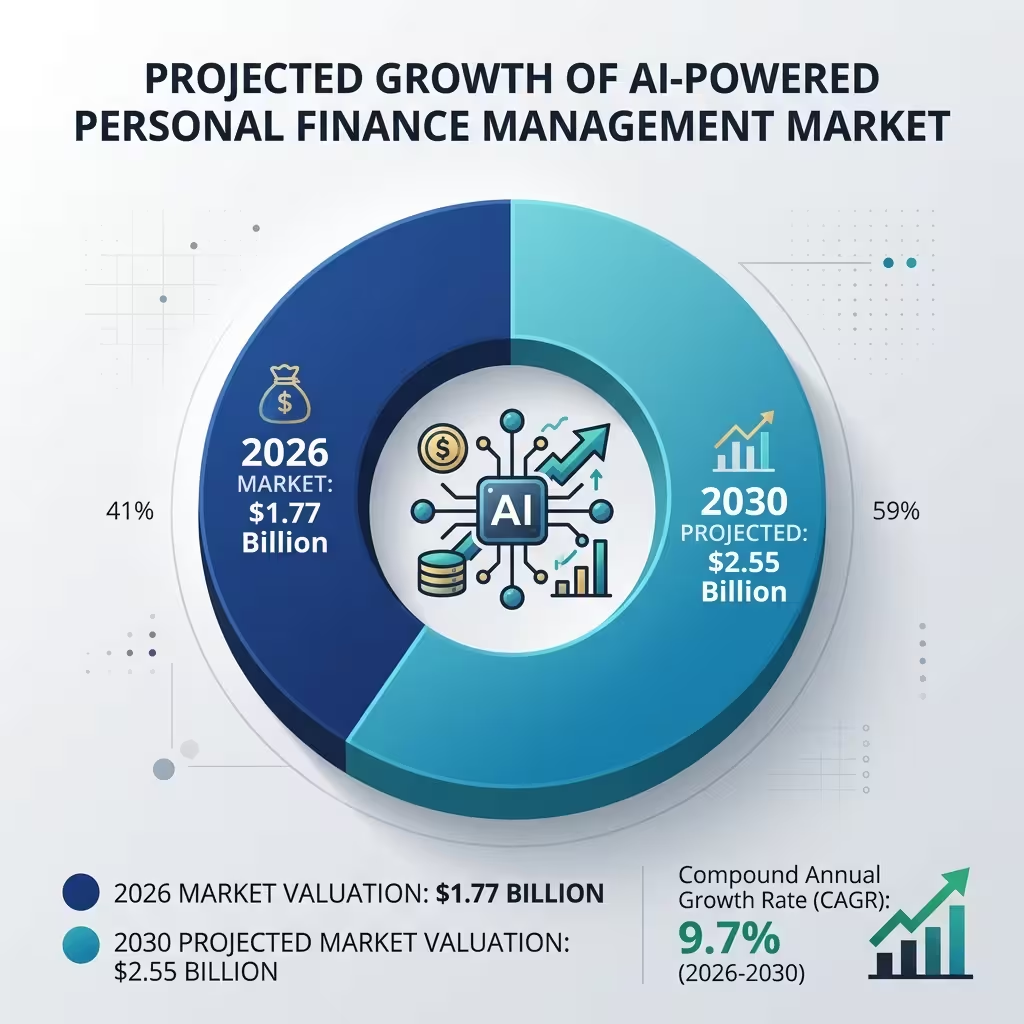

The AI-powered personal finance management market was valued at $1.77 billion in 2026. It’s projected to reach $2.55 billion by 2030. The growth rate is 9.7% annually.

Three technologies are driving this market. Machine learning lets platforms study your patterns and get smarter about your specific financial behavior over time. Predictive analytics is the forecasting engine — the model that builds a 30 to 60-day picture of your cash flow. NLP is what makes these tools feel like a conversation instead of a spreadsheet.

The shift from reactive to proactive is the defining trend here. Reactive told you what already happened. Proactive changes what’s about to happen. That’s what makes 2026’s tools genuinely different from the apps people tried in 2021 and deleted after two weeks.

The financial sector has a 30% AI adoption rate — second only to professional services at 33%. That number is growing. The platforms becoming standard in personal finance are the ones that automate the behavior, not just the reporting.

People Also Ask – PAA’s

How do I use predictive AI to build an emergency fund?

Pick a platform that does cash flow forecasting — Tilt and Oportun are the two built specifically for this. Connect your main checking account, set a named goal with a dollar amount and a date, and leave it alone for 60 days. The AI identifies the safe transfer windows in your cash flow and moves money when your account can absorb it. You don’t decide when or how much. The system does.

What are the best automated saving strategies for people with low income?

Oportun is specifically designed for lower and variable incomes. It uses small, frequent transfers instead of large monthly ones. Acorns’ round-up model also works well — it never takes a fixed amount, only the spare change on purchases you make anyway. Both approaches avoid the overdraft risk that makes automated saving fail for people with tight cash flows.

Is behavioral finance AI actually safe?

The safety question comes down to two things: data access and platform security. Reputable platforms connect through read-only APIs. They can see your transactions but cannot initiate withdrawals from unconnected accounts. Look for SOC 2 Type II certification. Avoid platforms that ask for your login credentials directly rather than using a secure API connection like Plaid or Finicity.

What’s the difference between round-up savings and smart saving algorithms?

Round-up savings is simple — every purchase gets rounded up and the spare change goes to savings. Smart saving algorithms are more complex. They model your entire cash flow, identify optimal transfer windows, adjust for upcoming bills, and vary the transfer amount based on what your account can handle. Round-ups are the starting point. Smart algorithms are the upgrade once you have a stable enough income to make the larger transfers worth modeling.

Do I still need a budget if I use predictive AI for savings?

Not necessarily. These platforms work by automating the behavior that budgeting asks you to do manually. If your main goal is building savings, a predictive AI platform does more to produce that outcome than a manual budget does. If you want full visibility into every spending category, you might want a budgeting app alongside it. But for pure savings accumulation, the automation alone handles the task.

What Happened With Priya

Four months in, she had $1,100. Eight months in, she hit her first goal: $2,000. The target she’d never reached in two years of planning to save.

She didn’t become a more disciplined person. She didn’t change her spending habits. She didn’t start reading financial newsletters or tracking every purchase.

She just set up a system that moved money when she wasn’t thinking about it, in amounts her account could handle, automatically, until the goal was done.

That’s the whole product promise of predictive AI for savings. Not that you’ll want to save more. That you won’t have to want to — because the system will do it for you.

The secret to hands-off saving is actually removing your hands from the process entirely.

About the Author Marcus Delray covers AI in personal finance, behavioral finance technology, and smart saving tools. He has written about fintech platforms and consumer financial tools for nine years.

Disclaimer: General information only. Not financial advice. App features, performance, and availability may change. Verify current details directly with the app provider before connecting financial accounts. The author and publisher accept no liability for outcomes based on this content.