Predicting Late Payments: Using AI Pattern Recognition to Fix Accounts Receivable

Last Updated: April 2025

My friend Carla called me frustrated last fall.

She manages AR for a mid-size manufacturer outside Houston. Been doing it seven years. Smart, detail-oriented, the kind of person who actually reads the aging report before 8 a.m. Her team of four covers about $14 million in monthly receivables across 200-plus active accounts.

Her CFO had just told her — not asked, told — that DSO needed to come down from 47 days to under 35 within two quarters.

She didn’t push back. But after the meeting she called me and said something I keep thinking about: “The worst part is, I don’t even know which customers are going to be late until they already are.”

That sentence is the whole problem with traditional AR. Not laziness. Not bad process. Just a system built entirely around reacting to things that have already gone wrong.

The data to see those problems coming was sitting right there in her payment history. Four years of it. Every customer leaving a trail every single invoice cycle. And none of it was being used to look forward.

That’s what AI for predicting late payments actually fixes. Not the chase. The blind spot.

If you want to understand how this fits into your broader treasury strategy, our ultimate guide to AI cash flow forecasting covers the full picture — from AR prediction all the way through to liquidity positioning.

Here’s something I’ve watched happen at multiple companies. They hire smart AR people. They build a solid collections process. Reminders go out on schedule. Escalations happen when they’re supposed to. The workflow is clean. And DSO still sits at 45 days, quarter after quarter, because the entire process is built to kick in after the problem exists.

Think about what that means operationally.

An invoice goes out. Due date comes. Nobody pays. Three days pass — now a reminder goes out. Customer says they never received it, or there’s a line item dispute, or the PO number doesn’t match. Another three days go by sorting that out. By the time actual payment happens, you’re 20 days past due on what should have been a net-30 account.

And the frustrating part? That exact sequence — the dispute, the PO mismatch, the delayed response — probably happened with that same customer six months ago. And six months before that.

The pattern was there. Nobody read it.

The Pattern Problem in Accounts Receivable

Every customer leaves behavioral fingerprints in your payment data.

Some customers always pay in the last three days of their net-30 window. Some routinely go 10 to 15 days past due but always pay eventually. Some pay fast when invoice amounts are under $5,000 and slow down significantly above that. Some dispute invoices whenever a specific product code appears. Some go quiet during their own fiscal year-end.

None of this is secret. It’s sitting in the transaction history of any company that’s been issuing invoices for more than a year.

Traditional AR software tracks invoice status. It doesn’t analyze payment behavior. That’s the gap. And it’s the exact gap that machine learning fills when you’re using AI for predicting late payments properly.

The models work by training on historical invoice and payment records — timing, amounts, dispute types, customer segments, invoice characteristics, seasonal cycles — and learning which combinations of signals statistically predict a late payment before the due date arrives.

When a new invoice is issued, the model scores it. High-risk invoices get flagged immediately. Not after they’re late. The moment they’re created.

Onguard’s 2025 research found that one in five invoices in the Netherlands contained errors significant enough to delay payment — and incorrect invoices were the fastest-growing cause of late payment that year. The US pattern isn’t dramatically different. Most of those errors were predictable from the data. Wrong PO numbers, missing line items, amount mismatches with existing purchase orders. A trained model catches those patterns before the invoice ever reaches the customer.

What Happens When You Actually Act Early

I want to be specific about this because “proactive collections” sounds like a vague consulting phrase.

Here’s what it looks like in practice.

Your AI platform scores 180 open invoices on Monday morning. Twelve get flagged as high-risk — probability of late payment above 70 percent based on current signals. Your collector looks at the list. Three of those are accounts with a history of PO disputes. Two are customers who always slow down in Q4. One is a new account with no history, flagged because of its industry segment and invoice size.

Before Tuesday, your team has:

Called the three dispute-prone accounts to confirm the invoice was received clean and the PO number matches. Sent a personalized heads-up to the two Q4 slow-payers, offering a small early payment discount. Routed the new account flag to the credit manager for a quick review.

None of those were collections calls. They were service calls. And the difference in how customers respond is significant.

Enterprises using AI to prioritize and act on high-risk accounts early have reported DSO reductions of up to 20 percent, according to published research from the International Journal of Engineering Research & Technology. For a company carrying $14 million in monthly receivables — like Carla’s — cutting DSO from 47 to 38 days frees up close to $1.4 million in working capital. That’s not a small efficiency gain. That’s a strategic lever.

That freed-up working capital shows up directly in your 13-week outlook — which is exactly why automating your 13-week cash flow forecast with AI and tightening AR prediction work best as a pair.

Dynamic Discounting — The Other Side of This

Most AR teams focus entirely on preventing late payment. Fewer think actively about accelerating early payment.

Dynamic discounting changes that.

The setup is simple: vendors offer customers a variable discount — typically between 0.5 and 2 percent — in exchange for paying ahead of the due date. The earlier the payment, the larger the discount. AI-powered platforms identify which customers are good candidates and trigger the offer automatically, without anyone on the AR team having to think about it.

For mid-size companies, the savings add up fast. Automated dynamic discounting platforms can generate between $50,000 and $200,000 in annual savings while simultaneously improving cash conversion cycles. Customers who take the discount pay faster. Customers who don’t still pay on time because the relationship stays positive.

Both outcomes are better than what the reactive model produces.

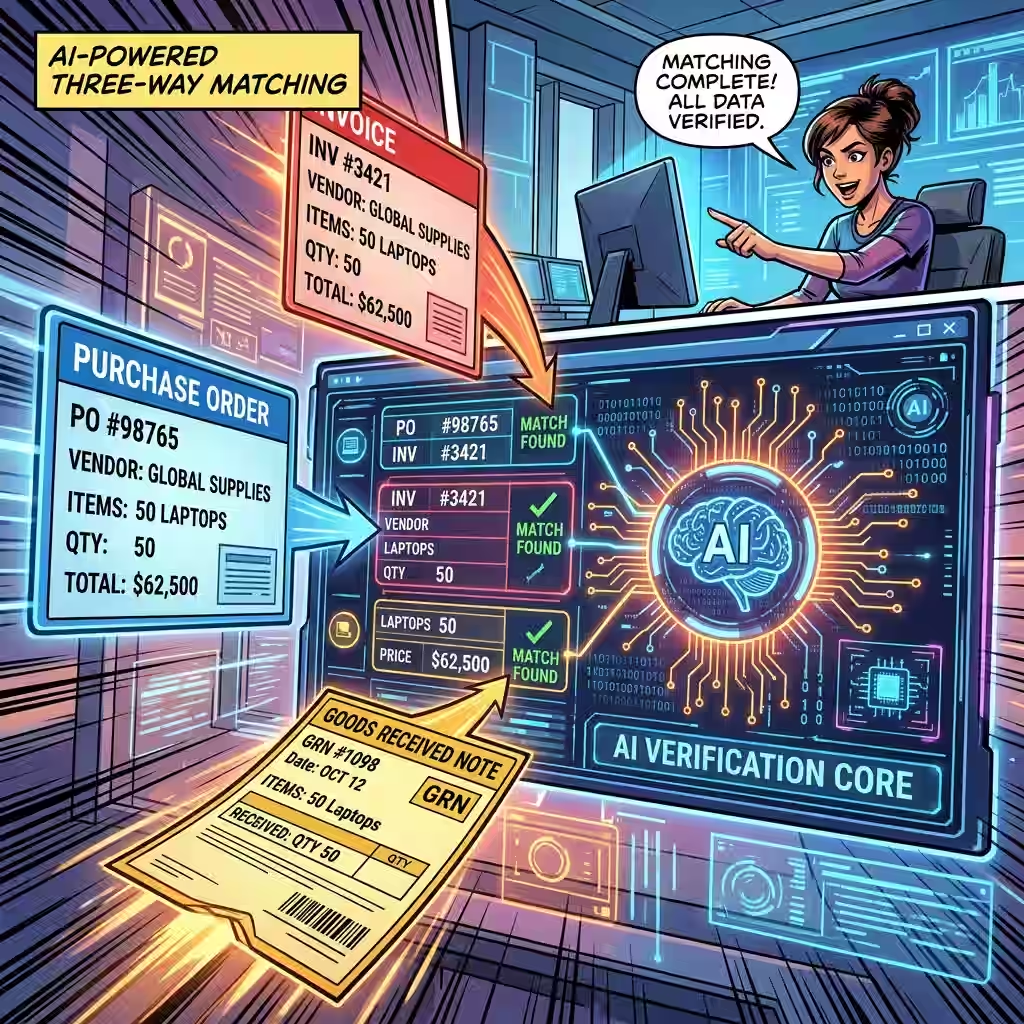

Three-Way Matching — Fixing the Error Problem at the Source

Here’s where I push back a little on the “customer behavior” framing of late payments.

A significant share of late payments aren’t about customer behavior at all. They’re about bad invoices. Invoices that go out with the wrong PO number, mismatched quantities, incorrect pricing — and sit in a dispute queue for two weeks while someone manually sorts out what went wrong.

One in five invoices contains these errors, according to Onguard’s research. That means 20 percent of your invoice volume has a built-in delay risk before a single customer makes a single decision.

AI-powered intelligent data capture addresses this directly.

Modern systems extract data from invoices with 99-plus percent accuracy regardless of format, language, or layout. They then run three-way matching automatically — checking that the invoice lines up with the original purchase order and the goods received note before it enters the payment workflow.

Old way: an AP clerk pulls the PO, pulls the GRN, compares them line by line to the invoice. If anything doesn’t match — and something usually doesn’t — a dispute gets opened. Days pass. Cash doesn’t move.

New way: the AI runs the same check in seconds. Exceptions get flagged. Clean invoices move straight through. Error rates drop by 95 percent. The most common cause of payment delay gets neutralized before the invoice even reaches the customer.

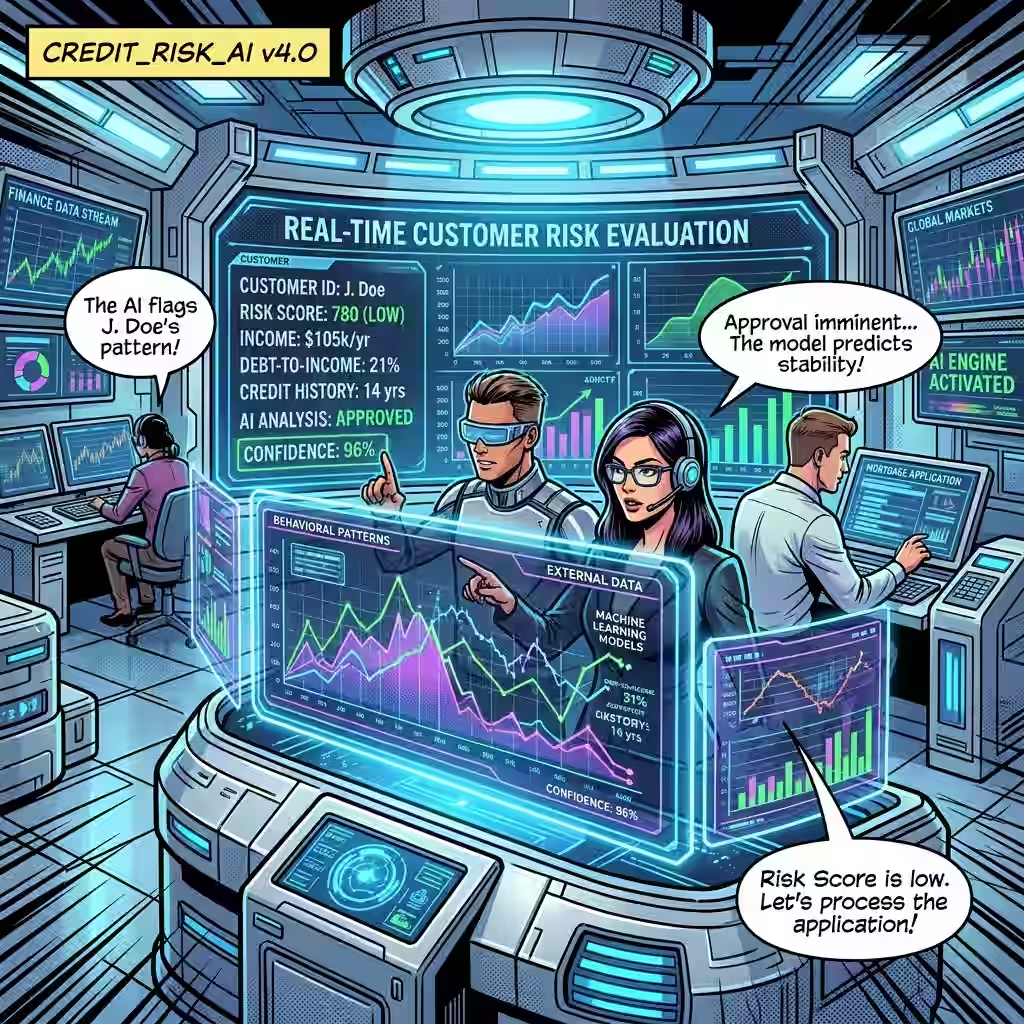

Credit Risk AI — Knowing Who to Watch Before You Extend Terms

Prediction isn’t only useful after terms are extended. It’s useful before.

Traditional credit evaluation was a point-in-time check. Pull a credit report when the customer opens an account. Update it annually if someone remembers. Everything that happens in between goes unmonitored.

AI underwriting changes the timing.

Platforms like Resolve offer credit decisions in 10 to 30 seconds using AI models that evaluate customer risk in real time. Slope, backed by J.P. Morgan, uses AI-driven cash flow underwriting to price net terms dynamically. These aren’t slow enterprise implementations — they’re live decisions made at the moment of sale, updated continuously as payment behavior evolves.

Disclosure: Platforms mentioned are referenced for informational purposes based on published research only. This is not a product recommendation.

The practical AR value: a customer who has paid reliably for 18 months but just missed two invoices in a row will see their risk score shift immediately. The system flags the account before the third invoice goes out — not after the third late payment has already happened.

Non-recourse financing takes the risk question off the table entirely. The financing platform assumes all credit exposure. If the customer defaults, the merchant is fully protected. Companies like Resolve and Now offer same-day payouts to merchants regardless of when the customer pays. For AR teams dealing with enterprise customers on long payment cycles, this changes the cash flow equation dramatically.

The Data Problem Nobody Wants to Talk About

I’ve watched AI AR implementations fail. Not many, but enough to see the pattern.

Almost every time, the problem wasn’t the AI. It was the data underneath it.

In 2025, research found a strange thing: Excel was making a comeback in finance departments. Not because people prefer spreadsheets. Because their CRM, ERP, and accounting tools don’t integrate natively, and someone has to bridge the gap. That bridge is usually an AR analyst with a pivot table and four browser tabs, manually reconciling payment statuses between systems that don’t agree with each other.

This is the exact problem that makes integrating AI forecasting cleanly with your ERP a prerequisite — not an optional step. That fragmentation kills AI prediction. A model trained on incomplete or inconsistent payment history will produce unreliable risk scores. An invoice that shows as open in the ERP, disputed in the CRM, and partially paid in the accounting system simultaneously — the model doesn’t know what to do with that. Nobody does.

Fix the data first. I know that’s not exciting advice. It doesn’t come with a demo or a trial period. But every AR team that’s gotten real results from AI pattern recognition ran a data quality audit before they evaluated a single platform. Clean, connected data is the foundation. Skip it and you’re just scoring chaos faster.

Agentic AI Is Already Changing What’s Next

The leading edge of AR technology isn’t just prediction anymore.

Agentic AI — autonomous systems that execute workflow steps without being triggered — is moving into accounts receivable fast. Not just flagging high-risk invoices. Actually sending the early reminder. Triggering the dynamic discount offer. Routing the disputed invoice to the right person based on account history and issue type.

A global bank deployed agentic AI across its financial operations and saved over 40,000 hours while cutting operational costs by 65 percent. A retail company integrated agentic systems with its inventory and collections workflows and reduced lag by 90 percent — saving $3.8 million per quarter.

Those numbers come from real deployments, not projections.

For AR specifically, what this means is that the team’s job changes. AI handles the routine — the reminders, the matching, the early flags. People handle the judgment — the complex disputes, the strategic accounts, the relationship decisions that can’t be automated without damaging a customer relationship.

That’s not a smaller AR team. It’s an AR team with time to actually do the strategic work they were always supposed to be doing but never had capacity for.

What Happened With Carla

She did the data audit. Hated it. Three weeks of untangling customer records that had been duplicated when the company switched ERPs two years earlier. Payment histories split across two systems, neither of them complete.

Once the data held up, they deployed an AI-based predictive AR platform.

Week three, the system flagged nine accounts before their due dates. Her team reached out early. Six paid on time — four of them had been reliable late-payers for over a year. Two negotiated short extensions with actual commitment dates, which they hit.

End of the first full quarter: DSO dropped from 47 to 41 days. Not 35 yet. But the direction was clear, and more importantly, Carla stopped getting surprised. The CFO noticed. Didn’t say much — just stopped asking weekly questions about the aging report.

She told me the strangest thing wasn’t the DSO number. It was how the job felt different. Less firefighting. More actual management.

That’s the real promise of AI for predicting late payments. Not magic. Not a tool that runs itself. A system that reads the patterns your customers have been leaving in your data for years — and gives your team a chance to act before it costs you anything.

People Also Ask – PAA’s

How does AI predict late payments before they happen?

It trains on historical invoice and payment data — timing patterns, dispute history, invoice characteristics, seasonal behavior — and scores each new invoice at the moment it’s created. High-risk invoices get flagged before the due date so your team can act proactively instead of reactively.

What is DSO and how much can AI actually reduce it?

DSO measures how many days on average it takes to collect payment after a sale. AI reduces it by identifying high-risk accounts early, automating reminders and prioritization, cutting invoice errors through intelligent data capture, and enabling dynamic discounting to accelerate payment from reliable customers. Enterprises using AI for DSO optimization have reported reductions of up to 20 percent.

How does machine learning identify delinquent accounts early?

Models analyze thousands of historical transactions to find which signals — payment timing, dispute frequency, invoice error rates, seasonal dips — most reliably predict a late payment. Scores update as new payment data comes in, so risk reflects current behavior, not just history from years ago.

What is three-way matching and why does it matter for reducing late payments?

Three-way matching checks that an invoice aligns with the original purchase order and the goods received note before it enters the payment queue. AI automates this with 99-plus percent accuracy, catching the invoice errors that cause roughly one in five payments to get delayed before a single customer makes a single decision.

What does non-recourse financing do for AR risk?

In a non-recourse model, the financing platform assumes all credit exposure. If the customer doesn’t pay, the merchant isn’t liable. Companies like Resolve offer same-day payouts regardless of when the customer actually settles. For businesses with large enterprise customers on long payment cycles, it removes the AR cash flow problem almost entirely.

Is data quality really that important before deploying AI for AR?

Yes — more than almost any other factor. An AI model built on fragmented or inconsistent payment data will produce unreliable risk scores. The most common cause of failed AR AI deployments isn’t the algorithm. It’s incomplete data from disconnected CRM, ERP, and accounting systems. Run a data audit before evaluating platforms.

About the Author

This article was researched and written by the finance operations editorial team at [Publication Name]. Source data draws on Onguard’s 2025 Credit Management Report, Ardent Partners AP research, SAP TechEd 2025 RPT-1 briefings, and published research from the International Journal of Engineering Research & Technology.

Disclaimer: This article is for informational purposes only. It is not financial, legal, or investment advice. Companies evaluating AI platforms for AR or credit management should work with qualified advisors before deployment.