YNAB vs Copilot Money vs Monarch: Which AI Budgeting App Actually Stops You Overspending?

Last Updated: April 2026

Marcus pulled in $94,000 last year. Not bad for 31. No debt spiral, no

gambling habit, nothing dramatic.

But here's what happened every single month. Around the 18th, he'd open

his bank app, see a number, and start doing math in his head. Dinner last

Friday. The gym membership. That Amazon order he forgot about. He'd think he

was fine. He'd hope he was fine.

Most months he wasn't.

What Marcus was dealing with isn't a income problem. It's a clarity

problem. The 2026 Money Mood Report found that 85% of Americans are

stressed about money — same number as people stressed about their health. And

76% are doing exactly what Marcus does: running the math in their heads instead

of opening a budget.

That's the gap AI budgeting apps are supposed to close. But they don't

all close it the same way.

Some apps want you to show up and do the work. Others want to do it for

you. And one of them — depending on who you are — will change how money feels

in your life. The others will sit unused after three weeks.

This breakdown covers YNAB, Copilot Money, and Monarch Money. Not which

one has the longest feature list. Which one will stop you from overspending.

Disclosure: This post contains referral-style links. If you sign up

through one, we may earn a small commission. Costs you nothing. All opinions

are independent.

Why Most AI Budgeting Apps Don't Actually Work

Let's get this out of the way. The problem with most budgeting apps isn't

the app. It's what the app does after you spend money.

Most of them report. They don't prevent.

You buy something stupid. It syncs. The app puts it in a category. You

look at the pie chart and feel bad. That's it. That's the whole experience. You

didn't make a better decision — you got a slightly colorful receipt.

That's not budgeting. That's an autopsy.

What changes the behavior is knowing before. A live number. The amount

you have left in a category before the card hits the terminal. That's the shift

— from tracking to deciding. And the best AI budgeting software in 2026 is

built around that exact moment.

The question is which one fits the way your brain works.

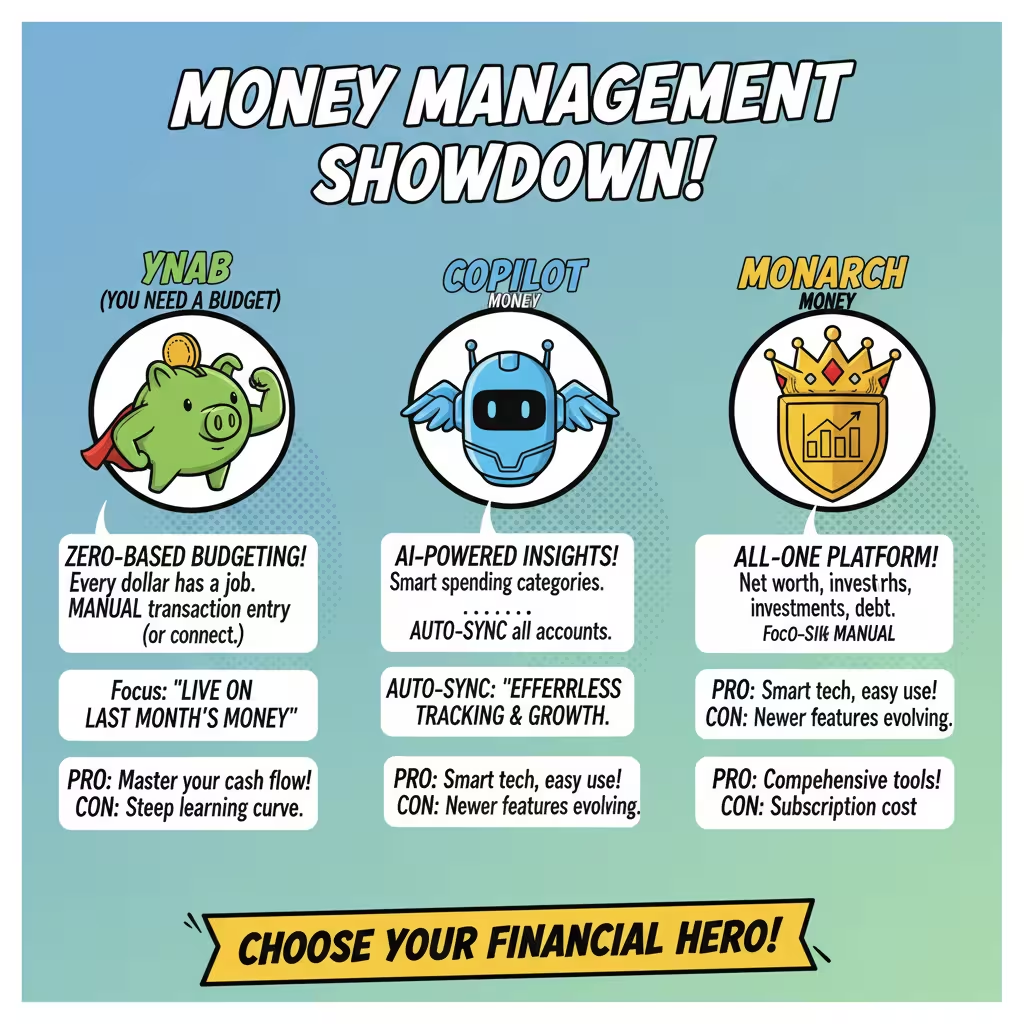

Quick Comparison: YNAB vs Copilot Money vs Monarch Money

|

Feature |

YNAB |

Copilot Money |

Monarch Money |

|

Budgeting Method |

Zero-based |

AI-automated |

Holistic cash flow |

|

AI Expense Categorization |

Yes |

Yes — learns over time |

Yes + receipt scanning |

|

Net Worth Tracking |

Basic |

Yes (crypto + real estate) |

Full equity tracking |

|

Couples / Shared Budgets |

YNAB Together plan |

No |

Unlimited collaborators |

|

Bill Reminders |

Yes |

Yes |

Yes |

|

Platform |

iOS, Android, Web |

iOS only |

iOS, Android, Web |

|

Price (2026) |

~$109/year |

~$107/year |

~$99/year |

|

Free Trial |

34 days |

30 days |

7 days |

YNAB: Built for People Who Keep Falling Off Track

Here's who YNAB is for. You earn decent money. You're not reckless. But

at the end of the month, you genuinely don't know where it went.

Sound familiar?

YNAB runs on zero-based budgeting. The idea is blunt: every dollar you

earn gets a job before you spend it. Rent gets a job. Groceries get a job. That

vague "fun stuff" feeling you've been spending on? That gets a job

too. Once the job is assigned, the guesswork stops.

It sounds like a lot of work. It's actually less work than what you're

doing now — running numbers in your head at the register and hoping for the

best.

The 2026 version added a feature called "Current Goal" — a

single mission pinned to your home screen every time you open the app. One

number. One target. Nothing buried in a menu. It's a small thing that turns

discipline into habit because you can't avoid seeing it.

YNAB Together, the shared plan, now shows "Recent Moves" — who

moved money between categories, complete with their avatar. Useful when you and

your partner both manage the budget and someone shifted the grocery money into

"dining out" again. No blame, no mystery. The app just shows you.

92% of users report less financial stress within a month of using YNAB.

That's a number they publish from their own research, and I believe it — not

because the app is magic but because the method forces you to make decisions

before spending, not after.

The weak spots. Getting started takes effort. If you miss a week and come back to a

backlog of uncategorized transactions, catching up is a slog. A lot of people

quit before the method clicks. Also, YNAB's investment tracking is thin. If you

have RSUs or a complex portfolio, you'll need something else for that piece.

Best for: Anyone stuck in the paycheck-to-paycheck loop even on a decent income. People who want to build a real habit, not just watch a dashboard.

Copilot Money: The Hands-Off AI That Learns Fast

Copilot asks very little of you. That's the whole pitch.

You connect your accounts. It watches. After a few weeks, it starts to

know you. The charge showing up as "SQ*HARBOR COFFEE" gets filed

under coffee without you touching it. The $52 Trader Joe's run lands in

groceries, not household supplies. You stop fixing its mistakes. Eventually you

stop thinking about it.

That's the goal. An AI app that tracks all your spending automatically —

and does it quietly, without asking you to rate every purchase or assign every

dollar a category name.

The investment side is where Copilot pulls ahead of the other two for

solo users. It links to crypto wallets, pulls Zillow estimates for real estate,

and puts your full net worth in one view. All of that for $107 a year is

genuinely good value.

One feature that gets overlooked: Rollovers. Say you budget $200 for

entertainment and only spend $130 this month. The leftover $70 automatically

carries into next month. No decision required. That one thing alone removes a

weird amount of friction.

The weak spots. Copilot is iOS only. Full stop — if you're on Android, close this tab.

It also has no couples mode. You can technically share login credentials,

but there's no collaborative layer, no ownership icons, nothing built for two

people managing money together.

And it's passive. Copilot is excellent at showing you what happened. It's

not going to tell you what to do next. If you need that kind of direction — if

you want the app to hold you accountable — Copilot will feel like it's not

paying attention.

Best for: iPhone users who want automated budget tracking without the manual work. Solo earners who want spending clarity without a system to maintain

Monarch Money: The One Built for Couples and Complex Households

Monarch Money is the hardest one to summarize because it does the most.

That's its strength and, honestly, its one real weakness.

Start with the AI assistant. Monarch didn't build a chatbot that

regurgitates generic tips. They trained it with input from Certified Financial

Planners and PhDs. You can ask it something like "why did my net worth

drop this month?" and get an actual, specific answer — not a redirect to a

help article.

The Receipt Scanning feature fixes something that drives me crazy about

other apps. When you spend $190 at Costco, most apps throw the whole thing into

"Shopping." Done. Monarch splits that same charge into groceries,

household, electronics — automatically. If you're tracking spending categories

automation across a real budget, that difference matters every single month.

For couples, the Ownership Icons are the feature that changes everything.

Every transaction shows who made it. No more "did you buy this?"

conversations. The Sankey diagram — a visual flow chart of where income goes —

gives both partners the same picture at the same time. I've seen this feature

specifically credited with reducing money arguments in households because it

removes the information gap that causes most of them.

Equity compensation tracking is in a class by itself here. If you receive

RSUs, ISOs, or NSOs as part of your comp package, Monarch tracks vesting

schedules alongside your cash flow. Most people handling that kind of

compensation are either using a separate spreadsheet or ignoring it entirely.

Monarch brings it into the same view as your monthly budget.

The weak spots. Sync reliability is a recurring complaint. Fidelity and PayPal

connections drop more than they should. When a linked bank account goes dark

for two days, the whole "effortless" experience breaks down fast.

The free trial is only 7 days. Not enough time to feel the value.

Best for: Couples. High-income households with investments and equity comp. Anyone who wants a Monarch Money review from someone who's actually dug into the equity features — they're real and they're useful.

The One Feature All Three Get Right: Sinking Funds

This deserves its own section because most people skip it — and it's the

habit that removes more financial stress than anything else on this list.

Sinking funds work like this. Your car will need repairs at some point.

You don't know exactly when. So you put $50 a month into a "Car

Repairs" category and leave it there.

Then the $800 bill shows up. And it's not a crisis. It's an

inconvenience.

A real YNAB user in 2026 described it exactly that way. Car needed major

work — thousands of dollars. Wasn't an emergency. The money was already there,

already assigned. That's the line between white-knuckling your budget and

actually being worry-proof.

All three apps support sinking funds in some form. Copilot's rollovers do this passively. YNAB and Monarch let you build dedicated categories with monthly targets. Either way, the concept turns financial surprises into planned expenses — and that one shift makes the $100 monthly fee for any of these apps worth it.

Which Budgeting App Should You Actually Use?

No single winner.

If your core problem is overspending because you never know what's left —

use YNAB. The zero-based method forces you to decide before you spend. The

34-day trial is long enough to feel the difference.

If you're on iPhone and want automation that stays out of your way — use

Copilot. Set it up once, let it learn, check in weekly. No maintenance

required.

If you share finances with a partner, or you have investments and equity

comp alongside your regular budget — use Monarch. The collaboration layer and

the AI assistant built on actual financial expertise put it in a different

category for complex households.

Marcus, the guy we opened with, tried all three. He's on Monarch now. Not

because of the feature count. Because his partner uses it too — and the

ownership icons killed three arguments in the first month. He mentioned the

Sankey diagram to me specifically. Said it was the first time money ever made

visual sense to him.

That's what a good AI budgeting app does. It doesn't bury you in data. It closes the gap between knowing and doing. That gap is where overspending lives

Frequently Asked Questions - FAQ's

What is the best AI budgeting app for couples in 2026? Monarch Money. It supports unlimited

collaborators, displays who made each transaction, and includes an AI assistant

trained by financial professionals. The shared cash flow visibility alone makes

financial conversations easier for most households.

YNAB vs Monarch Money — which is actually better? Depends on your situation. YNAB wins

for building discipline and breaking the paycheck-to-paycheck cycle through

zero-based budgeting. Monarch wins for couples, complex households, and anyone

tracking investments or equity compensation. Both are strong. The difference is

method, not quality.

Is Copilot Money worth it for budgeting? Yes, if you're on iOS and want

spending categories automation without constant manual input. The AI

categorization gets accurate fast, the investment tracking is solid, and the

hands-off design is genuinely rare. If you're on Android, it's not an option.

What is zero-based budgeting and does it actually work? Zero-based budgeting means giving

every dollar of income a specific job before you spend it. Nothing sits in a

vague "whatever" pile. YNAB built its entire product around this

method, and 92% of users report measurably less financial stress after one

month. It works — but it requires you to show up.

Are AI budgeting apps safe with linked bank accounts? Reputable apps connect through

read-only services like Plaid, Finicity, or MX. These can see your transactions

but have zero ability to move or transfer funds. Monarch Money also holds SOC 2

certification, which is a verified third-party security audit. Enable

multifactor authentication on every financial app. Non-negotiable.

Which app is best for subscription tracking? All three handle subscriptions. If

subscription cancellation and bill negotiation are your main goals, Rocket

Money is the more focused option — they negotiate bills directly with providers

and only charge a fee if they succeed.

About the Author

Marcus Delray is a financial operations consultant based in Austin, TX.

He works with independent professionals on personal finance systems, cash flow

strategy, and digital budgeting tools. He has spent the last three years

helping individuals build automated money systems that reduce anxiety without

requiring constant maintenance.

Disclaimer: This post is for informational purposes only and does not constitute financial advice. App pricing and features are subject to change. Verify current terms directly with each provider before subscribing.