AI Credit Scoring: How Lenders Decide who gets Approved!

Marcus had been freelancing for six years in Atlanta. He paid rent on

time every month. His utility bills? Never late. His phone bill? Auto-pay,

never missed.

He applied for a car loan at a regional bank. They denied him. The

reason: no credit history.

He'd never carried a credit card. To the old system, he didn't exist.

Three weeks later, Marcus applied through a different lender. This one

used an AI credit score model. Same guy. Same income. Same payment habits. This

time, he got approved.

That's not a fluke. That's how AI determines credit score decisions now — and it's changing who gets approved, and how fast.

Why Your FICO Score Doesn't Tell the Whole Story

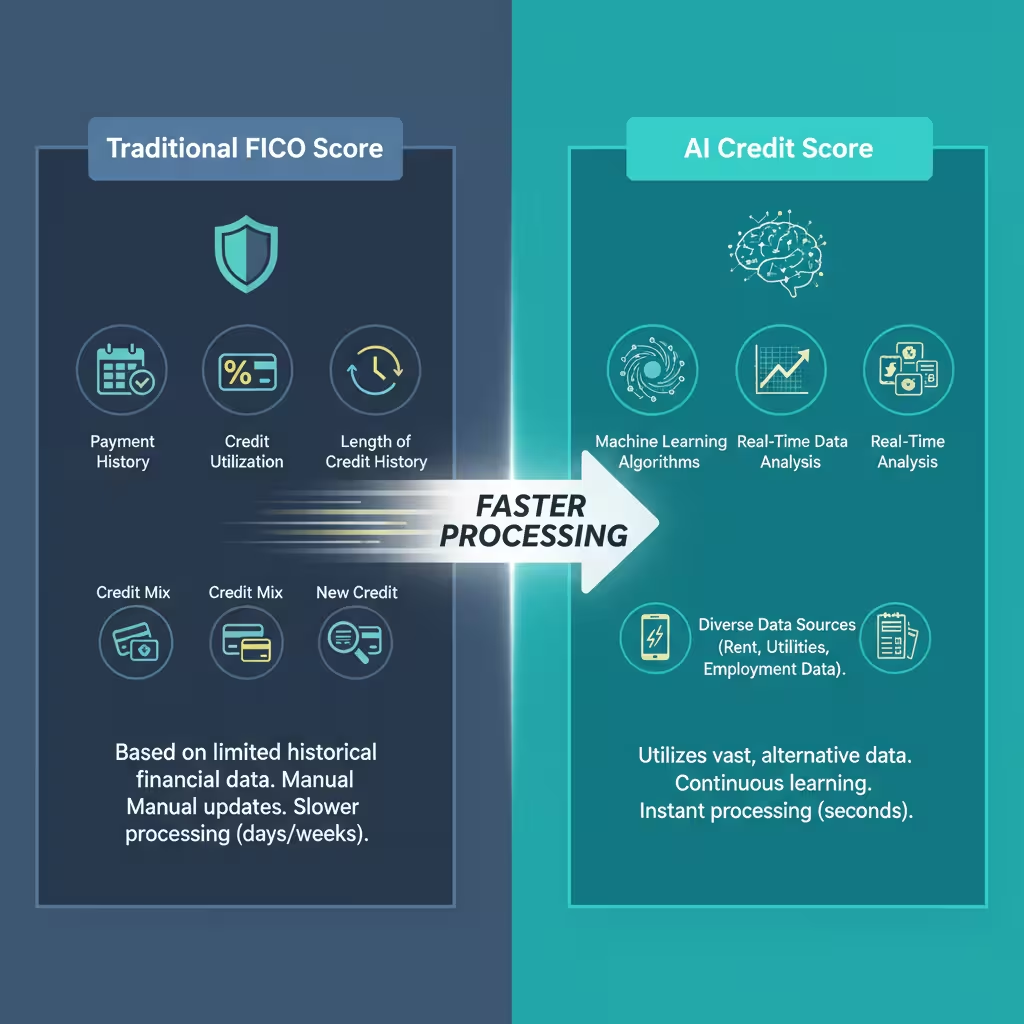

Traditional credit scoring has been the standard for decades. FICO pulls

from five buckets: payment history, amounts owed, credit history length, new

credit, and credit mix.

Simple enough. But it only works if you've used credit products before.

Never had a credit card, car loan, or student loan? You're what lenders

call a "thin-file" borrower. The bureau has almost nothing on you. So

FICO defaults to no.

Around 1.4 billion adults worldwide are unbanked or credit-invisible. In

the US, tens of millions fall into this group. Recent immigrants. Young adults.

Cash users. Gig workers like Marcus.

Traditional models treat all of them the same way. As unknowns.

That's the exact problem AI-based lending platforms were built to fix

What Is an AI Credit Score, Exactly?

An AI credit score comes from a machine learning model — not a

rules-based FICO formula. The gap isn't speed. It's the range of data the model

can read.

FICO looks at 20 to 50 data points from bureau records. A machine

learning credit risk model can scan thousands of signals at once. It pulls from

sources that traditional scoring ignores.

Here's what alternative credit scoring AI looks at:

- Utility payments — Did you pay your electric and

gas bills on time?

- Rent history — Landlord-verified payments are

a strong signal.

- Telecom patterns — Your phone bill cadence

matters.

- Digital wallet activity — Transaction regularity and

payment timing.

- E-commerce history — Purchasing patterns over time.

- Bank account cash flow — Income stability, overdraft

frequency, balance trends.

None of this shows up in your FICO file. All of it tells the AI something

real about your financial habits.

Companies like Zest AI, Pagaya, and Tala have spent years building these models. They're not guessing. Their systems find patterns in millions of past loan outcomes. Then they apply those patterns to new applicants at scale.

How the AI Loan Approval Process Actually Works

The AI loan approval process is fast. Here's the sequence most modern

lenders follow:

Step 1 — Data pull. You submit your application. The system pulls bureau data, bank

statements, and any alternative data the lender has access to. Some platforms

read your pay stubs and tax returns automatically using document processing

tools.

Step 2 — Signal extraction. The model scans hundreds of signals from your data. Not just "did

you pay late" — but how late, how often, and whether the pattern improved

over time. This is where machine learning credit risk modeling earns its name.

Step 3 — Risk scoring. The creditworthiness algorithm runs your signals through a trained

model. It produces a score. That score reflects the probability you'll default

on a loan of a set size over a set term.

Step 4 — Decision. The system approves, declines, or flags your file for human review.

Borderline cases go to a real person. Ethical AI lending standards require it.

Step 5 — Explanation. If you're declined, lenders must tell you why. Explainable AI lending

tools put the model's output into plain language. Example: "Primary

decline factor: Debt-to-income ratio (42%). Secondary factor: Recent credit

inquiries (28%)." A real answer — not a black box rejection.

Start to finish, the process can take minutes.

FICO Score vs. AI Score: What's the Real Difference?

A lot of people think an AI credit score is FICO with better software.

It's not.

For borrowers with strong bureau records, the results can look similar.

The difference shows up fast for thin-file applicants, gig workers, and recent

immigrants.

|

Feature |

Traditional FICO |

AI Credit Score |

|

Data Points |

20–50 bureau variables |

Hundreds to thousands |

|

Thin-file Performance |

Poor — defaults to no |

Strong — reads alternative signals |

|

Speed |

Hours to days |

Seconds to minutes |

|

Explainability |

Basic |

Factor-level breakdowns |

|

Bias Risk |

Moderate |

High if unchecked |

That last row matters. AI can outperform FICO on inclusion. But it can also replicate old discrimination patterns if built carelessly.

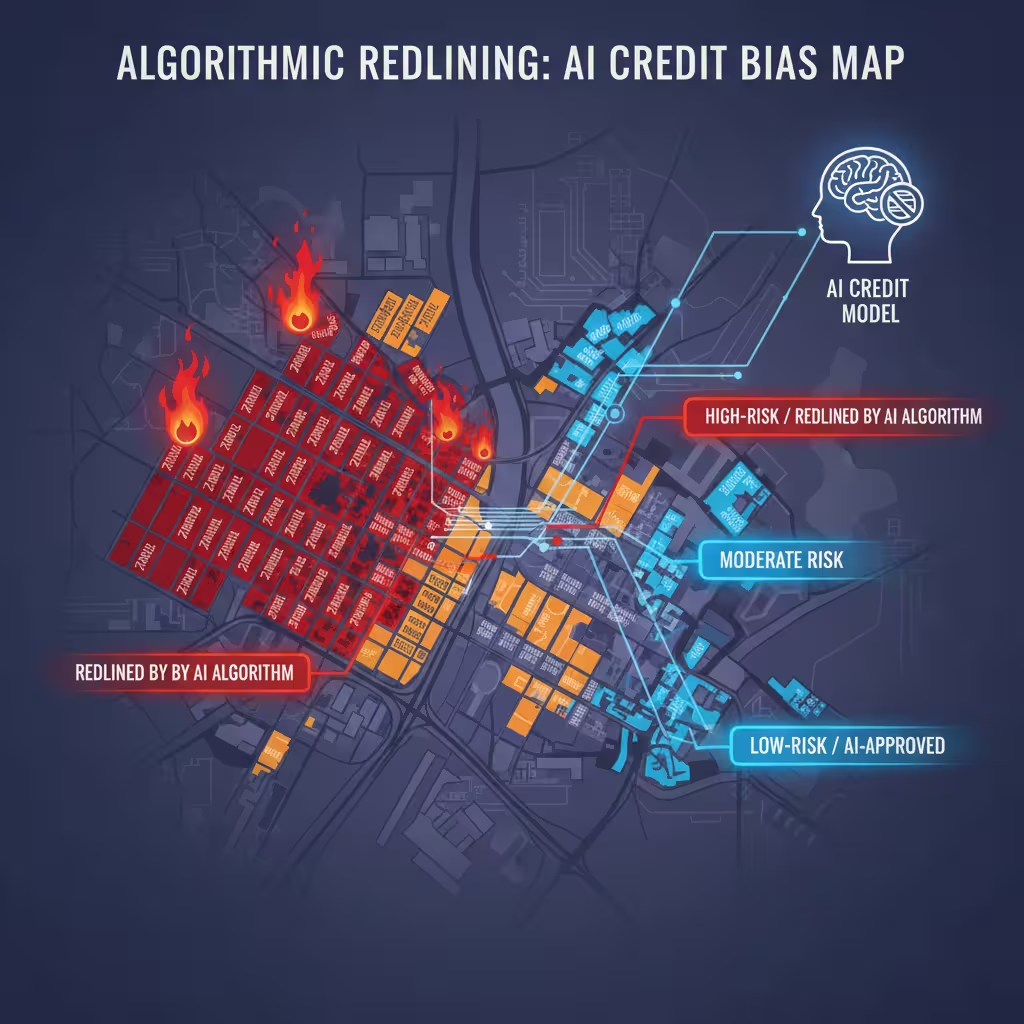

The Bias Problem Nobody Talks About Enough

Here's the uncomfortable truth. AI credit models can discriminate without

ever looking at your race.

It's called algorithmic redlining. It happens when a neutral data point

acts as a stand-in for a protected trait.

ZIP codes are the clearest example. A model trained on old lending data

will "learn" that certain ZIP codes are high risk. Not because those

borrowers are bad payers. But because decades of bad lending policy starved

those areas of capital. The AI doesn't know that history. It sees the pattern

and runs with it.

Surnames, shopping habits, and phone type can do the same thing. They

carry bias into a model that claims to be colorblind.

The legal system is catching up.

OceanFirst Bank paid $15.1 million in 2024 to settle redlining claims.

SafeRent Solutions paid $2.2 million. Their screening tool penalized Black and

Hispanic applicants who held housing vouchers. It ignored those vouchers. It

flagged the applicants as high risk based on old credit data — not current

behavior.

These aren't edge cases anymore.

The EU AI Act — fully enforced for high-risk systems as of August 2026 —

classifies credit scoring AI as high-risk. Lenders must run bias audits,

document their models, and let borrowers request an explanation for any denial.

In the US, Colorado's AI Act took effect in early 2026. It requires

annual audits and disparate impact testing. State attorneys general are the

main enforcers now.

Fair lending compliance isn't optional. It's the cost of playing in this space.

Can AI Actually Improve Your Chances of Getting Approved?

Short answer: yes — if traditional scoring misses you.

Gig workers. Recent grads. First-generation Americans. People who manage

money well but have never had a credit card. For these borrowers, an AI-based

lending platform gives the model a chance to see what FICO can't.

Alternative data shows what matters: steady payments, reliable habits,

stable cash flow. A person who has paid $1,200 rent on the first of every month

for three years is showing something real. The old credit decision engine

didn't care. The new one does.

AI isn't magic, though. Real debt problems and recent defaults show up too. But the model looks at more. So you get a fuller read — not a narrow slice of old history.

What Data Does AI Use to Score You — And What You Can Do About It

Knowing how the credit decision engine works helps you feed it better

signals. Here's what moves the needle:

Bank account behavior. Steady deposits and a stable balance signal health. Connect your bank

account when a lender offers that option. It works in your favor if your cash

flow is solid.

Rent and utility payments. Services like Experian Boost let you add rental and utility history to

your credit file. Use them. This is the fastest way to become visible to an AI

model from zero.

Telecom history. Some AI models check whether your phone bill is paid on time. Set it to

auto-pay.

Keep hard inquiries low. Applying for several credit products in a short window leaves marks. The

AI picks up the pattern.

FICO Score 11, launched in early 2026, now includes cash-flow and rental

data. Some alternative signals are moving into mainstream scoring for the first

time.

The credit system is opening up. Feed it the right signals.

FAQ: AI Credit Score Questions Answered

How does AI decide if you get a loan? The model analyzes hundreds of signals — payment

history, cash flow, account behavior — and calculates the odds you'll repay.

Higher odds mean better approval chances.

Is an AI credit score vs traditional FICO score really that different? For borrowers with strong bureau

history, the results can look similar. For thin-file borrowers, the difference

can mean approval vs. rejection.

Can AI improve your chances of loan approval? Yes — if you have steady habits that

FICO doesn't capture. Rent and utility payment history can make a real

difference with AI-based models.

What data does AI use to determine credit? Bank account activity, rent history,

utility payments, telecom patterns, e-commerce records, digital wallet

behavior, and standard bureau data — all reviewed together.

Are AI lending decisions biased? They can be. Models trained on biased data carry that bias forward.

Regulators now require fairness testing and bias audits. Ask any lender what

their adverse action process looks like.

What are AI-based lending platforms for bad credit? Platforms powered by Zest AI, Pagaya, and Tala build models designed to score thin-file and non-traditional borrowers. Research them if traditional lenders have turned you down.

The Bottom Line

Marcus got that car loan.

The second lender's AI model saw what the FICO pull missed. Four years of

on-time rent. Steady utility payments. A cash-flow pattern that showed someone

who handled money well. Same person. Completely different outcome.

That's what the AI credit score shift means for regular people. Not

fintech buzzwords. Real access for borrowers who manage money carefully but

don't fit the old mold.

The system isn't perfect. Bias risks are real. Regulatory pressure is

building for good reason. But the direction is right. A credit decision engine

that reads more of who you are — not just which cards you've carried — is

better than the one it replaced.

Know what signals you're sending. Feed the model the right data. Know

your rights when it comes to explanation and appeal.

The box isn't as black as it used to be.

Disclaimer: This article is for informational purposes only and does not

constitute financial or legal advice. Lending decisions vary by lender, state,

and individual circumstances. Always consult a financial professional before

making borrowing decisions.