Crush Your Debt Smarter: How AI Debt Payoff Tools Create a Plan Banks Charge $300/hr

I used to have a spreadsheet called "DEBT_FINAL_v3_ACTUAL_FINAL.xlsx."

You already know what that means. It means I had four other versions before it, none of them worked, and I gave up on this one too after about six weeks. The tab with my credit card APRs still had placeholder text in it from a YouTube tutorial I was following.

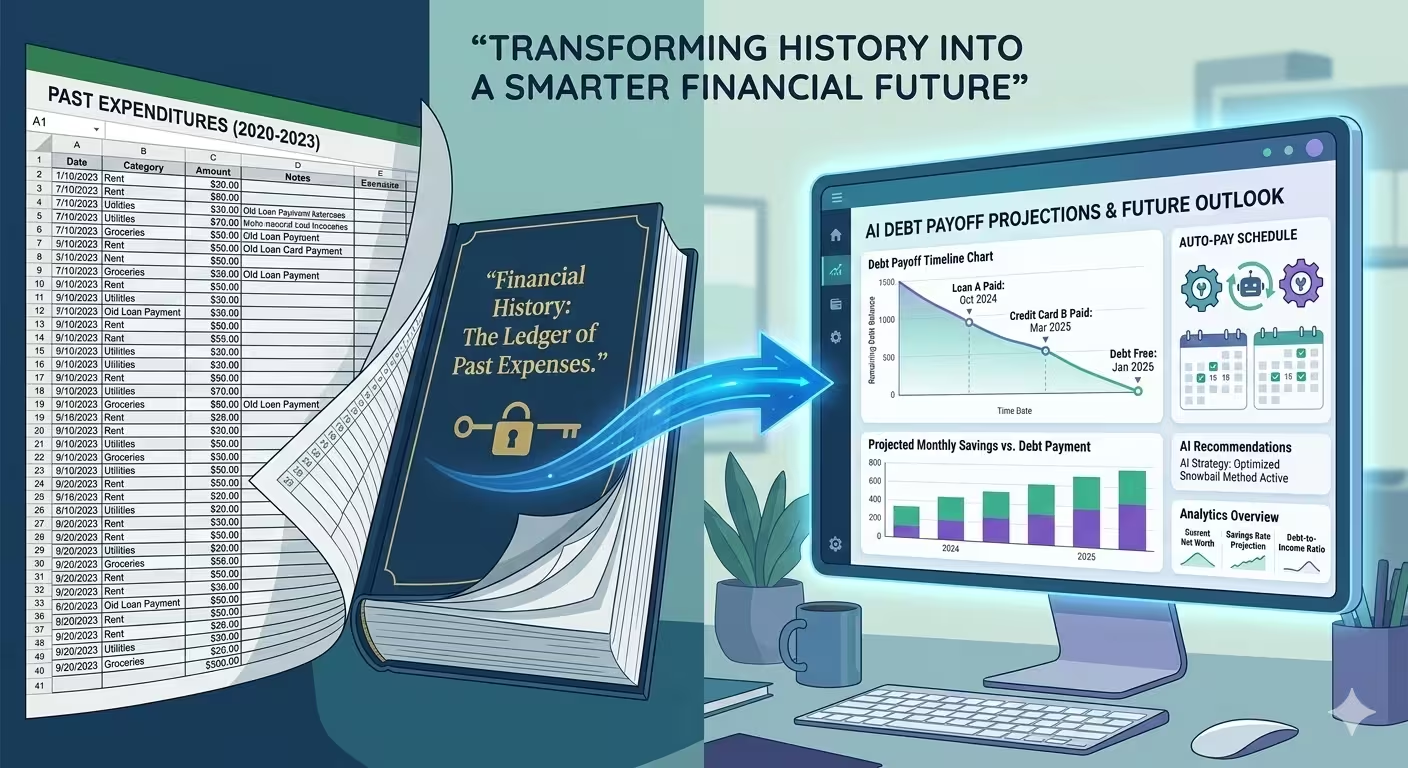

That spreadsheet didn't help me. What eventually helped me was realizing that the problem wasn't motivation or discipline — it was that I was using a tool designed to record history to try to plan a future. Spreadsheets don't update themselves. They don't know when your paycheck lands or when you accidentally renewed that $14.99 subscription you meant to cancel. They just sit there.

An AI debt payoff planner sits there too, technically. But it's connected to your actual accounts, watching in real time, and doing the math every single day without you having to open anything. That's a different thing entirely.

Your Spreadsheet Is a

History Book, Not a Plan

Spreadsheets record what happened. They don't tell you what to do next. And sure, you can set up formulas — but be honest, are you really going back in there every month to update your balances, adjust for that car repair you didn't budget for, and recalculate your payoff date from scratch?

Probably not. That's not a character flaw. That's just how humans work. We're not wired to enjoy financial maintenance tasks on a Thursday evening when Netflix exists.

What makes modern AI tools different is something called a deterministic mathematical engine. Instead of you doing the math, the app does it — automatically, constantly, and with cent-level precision. When your paycheck hits, when you miss a payment, when a subscription renews — the plan updates itself.

Let Me Explain Why

"Just Use the Avalanche Method" Is Bad Advice

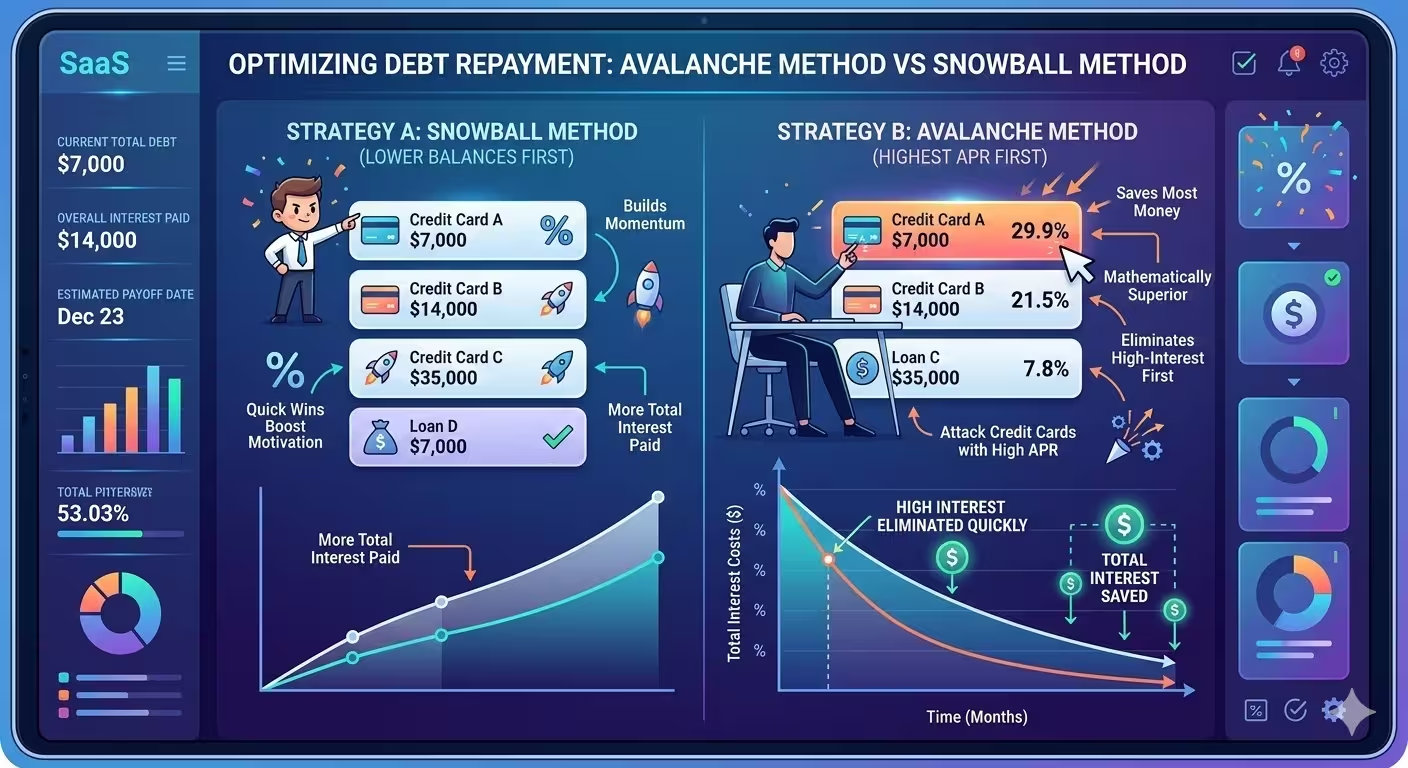

Every personal finance article on the internet says the same thing. Use the debt avalanche method. Target your highest interest rate first. It's mathematically optimal. Done.

And look — they're not wrong that the avalanche is more efficient. If you've got a credit card sitting at 24.99% APR, that thing is bleeding you. Every month you don't attack it, you're paying for the privilege of owing money.

But here's what those articles skip over. Most people who start on the avalanche method quit before they see results. Not because they're weak. Because the highest-interest debt is often also the largest balance, and grinding through a $9,000 balance for eight months without a single payoff feels like running on a treadmill that's also on fire.

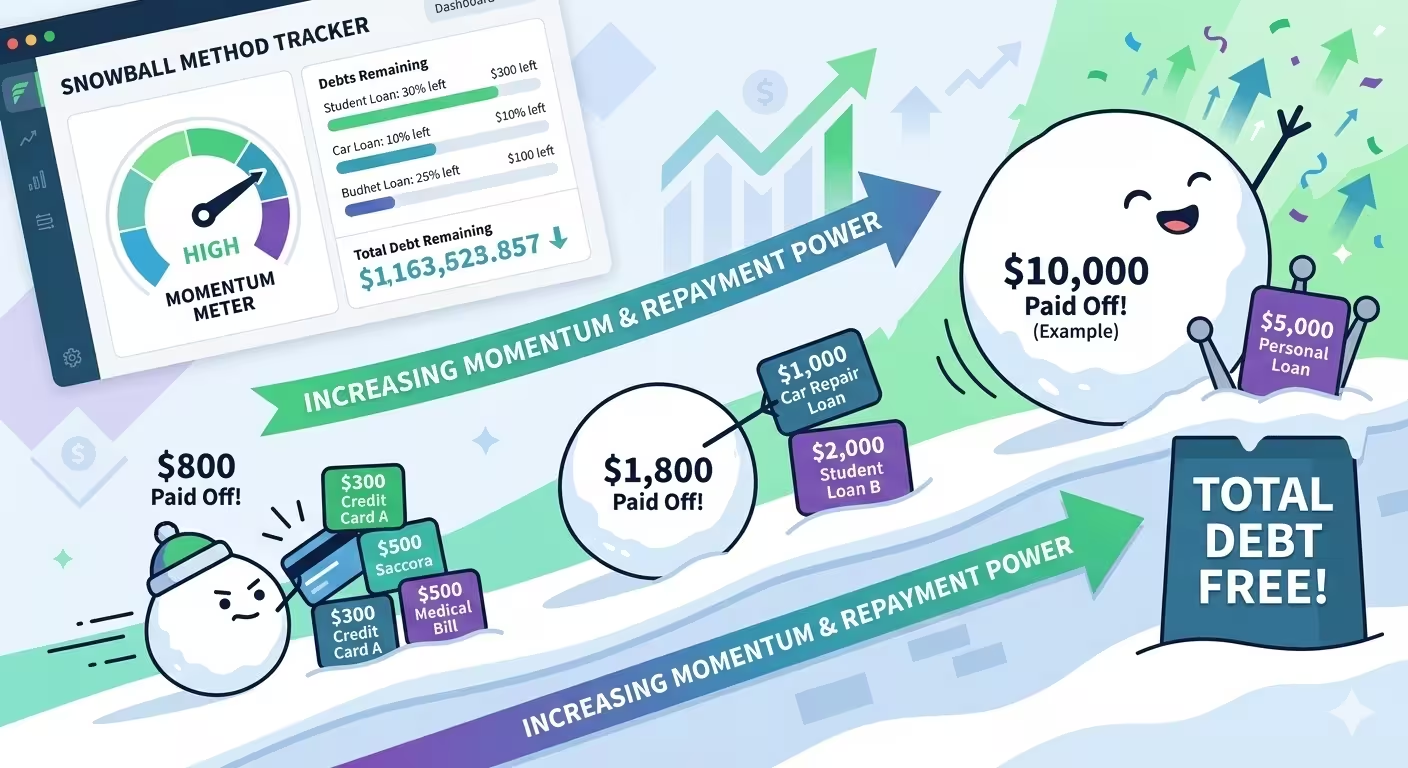

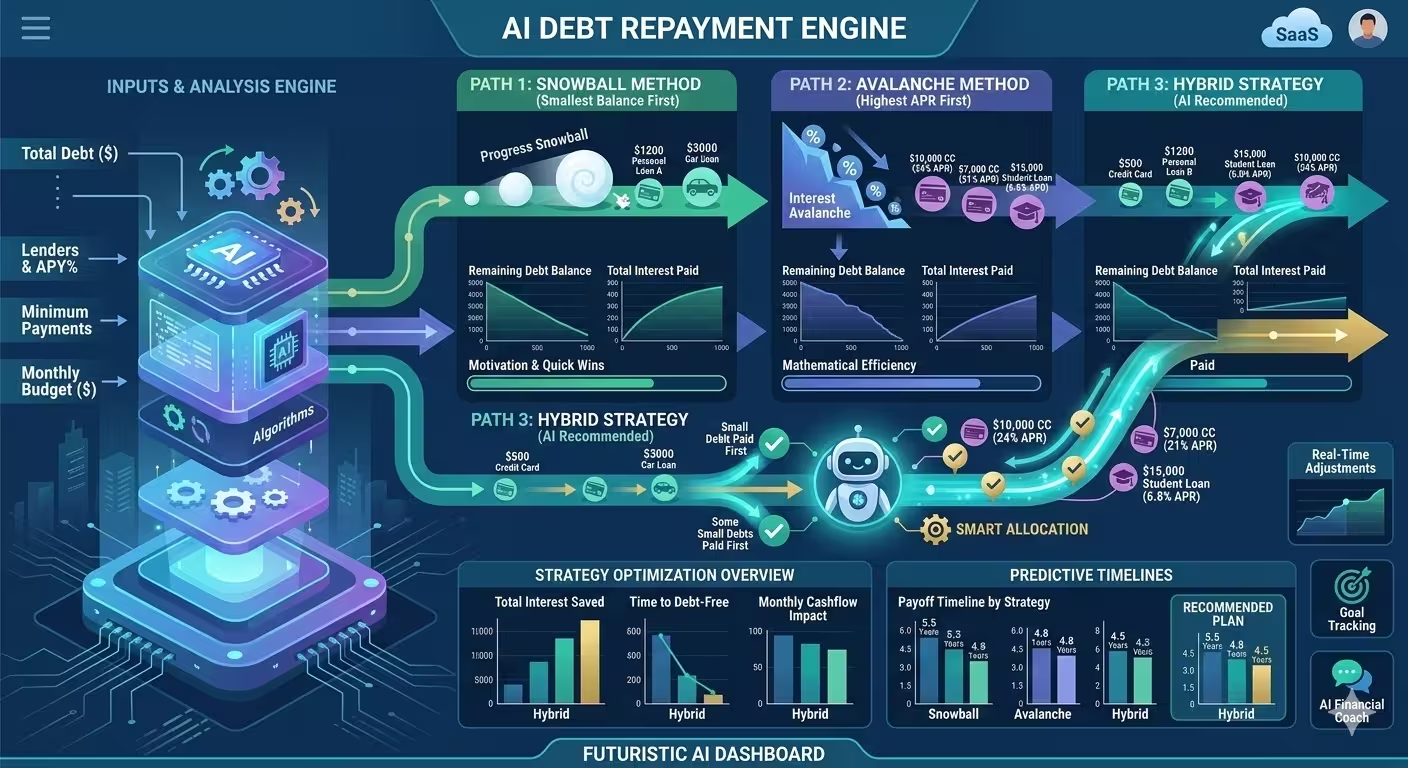

The Debt Snowball Method

You ignore interest rates entirely. You list your debts smallest to largest by balance, and you attack the smallest one first — throwing every extra dollar at it while paying minimums on everything else. When it's gone, you roll that freed-up payment onto the next smallest debt. Each payoff feels like a win. That feeling keeps you going.

Dave Ramsey made this method popular. And it works — especially when you feel buried. Studies consistently show that people who use the snowball method stick with their plans longer. The quick wins are real motivation. If you've ever had a gym membership you used twice, you already know that the optimal plan you don't follow beats literally nothing.

The Debt Avalanche Method

Here you rank debts by interest rate and hit the highest APR first. Mathematically, this is the winning move. You'll pay less total interest and get out of debt faster on paper. The problem? If your biggest, nastiest credit card is also your largest balance, you could be grinding away at it for a year before it's gone. No wins. No momentum. Just quiet desperation.

The Hybrid Method — Where AI Earns Its Keep

So here's what the best AI loan calculator platforms do that no spreadsheet can touch. They combine both methods based on your actual behavior.

The AI starts you on the snowball path. You knock out a couple of small balances. You build the habit. You prove to yourself this is working. Then — once the system has tracked enough of your payment history to see that you're consistent — it shifts your remaining debts to the avalanche strategy. You've already got the habit. Now you're optimizing.

It's a remarkably human insight wrapped in a very non-human level of consistency. No financial advisor is monitoring your spending every day and nudging your strategy in real time. An AI app genuinely is.

AI Tools to Create a

Personalized Debt Payoff Plan

Let me cut to the chase because there are a lot of mediocre apps in this space.

Origin — Best for the Full Picture

Origin gives you a complete view of your finances. Multiple accounts, investments, student loans, maybe a side income — Origin connects all of it and uses a multi-agent AI system where different specialized agents handle different parts of your financial life. In benchmark testing on CFP-style exams, Origin's AI scored 98.3% accuracy. The average human CFP scored around 79.5%. That gap matters when you're making real decisions.

Cost: $12–$20/month

Bright Money — Best for Credit Card Debt

If credit card debt is your main problem, Bright Money zeroes in on your APRs and automatically moves funds toward the most cost-effective balance. Less setup. Less fuss. Point it at the problem and let it run.

Cost: $8.99–$14.99/month

Undebt.it — Best for Flexibility

You can model eight different payoff methods side by side and see exactly how much each one saves you. Free version is genuinely solid. Premium is $12 a year — not a month, a year. Hard to beat.

Cost: Free / $12 per year (Premium)

ZilchWorks — Best for Privacy

Runs completely offline on your desktop. No bank connection. No subscription. No cloud. You enter your numbers manually and it builds the plan. If connecting your accounts to any app makes you uncomfortable, this is the answer.

Cost: $46.94 one-time

Debt Payoff Planner— Best Free Starting Point

Simple, clean, free. Good for beginners who just want to see their balances laid out clearly and try the snowball or avalanche method without paying anything.

Cost: Free

Best AI Debt Calculator for

Student Loans: The 2026 Changes

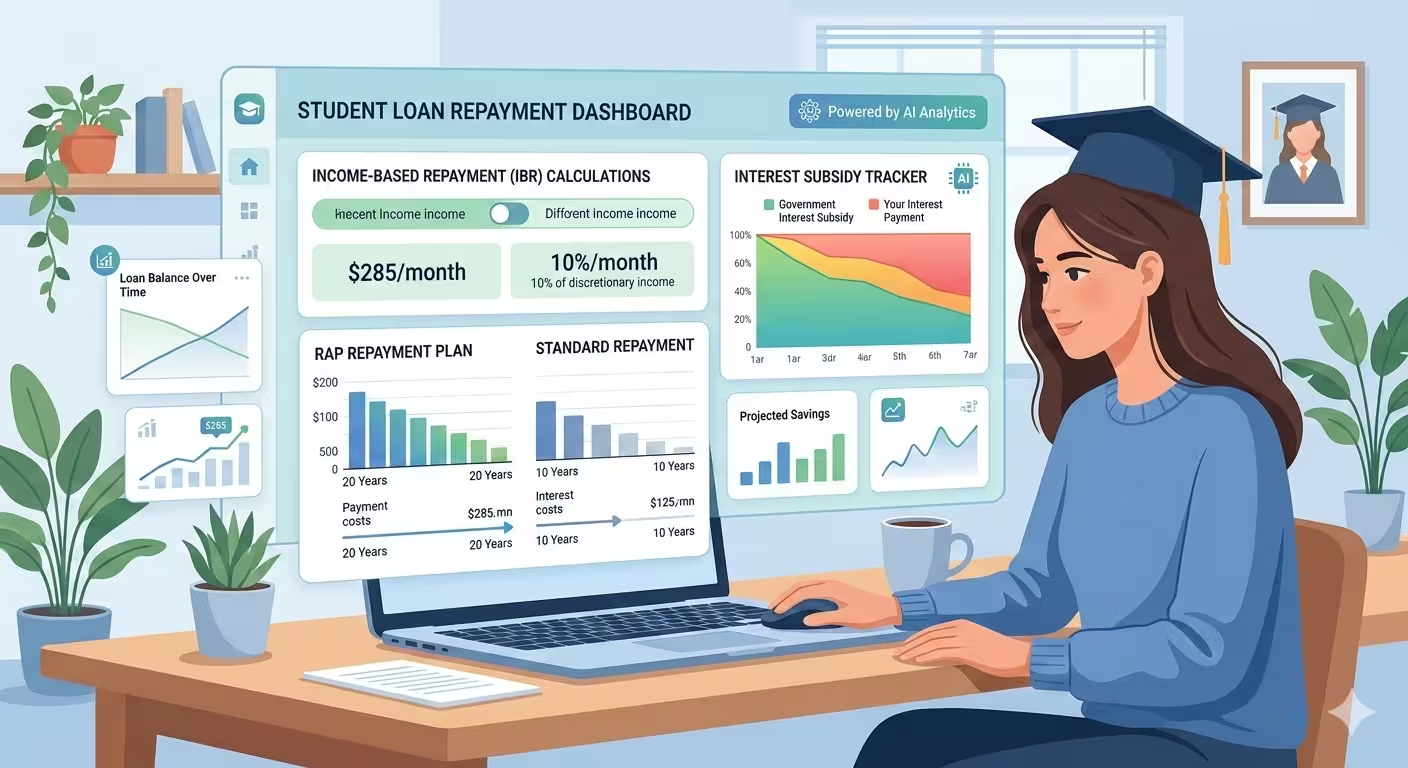

The federal student loan system changed a lot in 2026. If you're not up to speed, you could land in the wrong plan and pay significantly more than necessary.

The Repayment Assistance Plan (RAP)is now the main income-based option for federal loans. It calculates your payment using 1–10% of your Adjusted Gross Income (AGI) — not "discretionary income" like the old formulas.

RAP also includes a 100% interest subsidy. If your required monthly payment doesn't cover the interest that month, the government covers the gap. Your balance won't grow. This prevents negative amortization — that painful situation where you made payments faithfully but somehow ended up owing more than when you started.

Critical Deadlines:

• If your loans are from before July 1, 2026, you still have access to PAYE and ICR until they sunset on July 1, 2028. Model your transition now — not two weeks before the deadline.

• Parent PLUS borrowersare not eligible for RAP. To keep income-sensitive repayment options, they needed to consolidate into a Direct Consolidation Loan before July 1, 2026. After that deadline, the only remaining option is the New Standard Plan — no income adjustment.

An AI debt app that handles student loan modeling will surface these things automatically. A basic spreadsheet template from 2023 definitely won't.

Your Lender Is Using AI Too

— Here's What That Means

While you use AI to manage debt, your lender is running its own AI system — pointed at you — to figure out how to collect. Worth knowing.

Modern collection systems calculate a propensity-to-pay score. They analyze your payment history, your communication patterns, and your spending behavior. If the system flags you as a genuine hardship case, the response may be a proactive offer for restructuring rather than a collections call.

Many lenders now have self-cure portals — 24/7 online platforms where you can negotiate payment plans or explore settlement options without ever talking to a collections agent. If you've missed payments and you're dreading the phone call, check your lender's website for a self-service portal first. You might be surprised at what's on offer.

Smart Debt Management Starts

With Trusting Your Tool

Before connecting any app to your bank accounts, verify these things:

• Read-only bank connection:via Plaid or tokenized access — your login credentials should never be stored by the app

• AES-256 encryption:for data stored and in transit

• Multi-factor authentication (MFA):required at login, not optional

• FDCPA and GDPR compliance:especially important if you're dealing with anything collections-related

• Explainable recommendations:the app should tell you why it's making a suggestion, not just what to do

Frequently Asked Questions - FAQs

What does an AI debt payoff planner do that a spreadsheet can't?

It connects to your live account data, updates your plan automatically when your finances change, and applies behavioral logic to determine which debt strategy will work best for your situation. A spreadsheet waits for you to update it. An AI app runs in the background.

Is the avalanche method really better than the snowball?

Mathematically yes — the avalanche minimizes total interest paid. But 'better' depends on whether you'll stick with it. Research shows that quick wins from the snowball method keep people motivated. The best AI apps combine both through the Hybrid Method.

What's the best AI debt calculator for student loans in 2026?

Origin handles the most complexity, including RAP modeling and federal plan transitions. For a free option, the official loan simulator at studentaid.gov is worth using alongside any app you choose.

Can AI tools help with debt consolidation decisions?

Yes. Most advisor-grade platforms model debt consolidation scenarios and show exact interest savings and timeline changes. The app shows you the math; you make the call.

Is it safe to connect my bank account to a debt payoff app?

Yes, provided the connection is read-only and tokenized through a service like Plaid. The app sees your transactions but cannot initiate transfers. That's the standard for legitimate platforms.

The Short Version

The financial

planning industry spent decades making debt management feel like something only

wealthy, organized, spreadsheet-comfortable people could do well. That's not

really true anymore.

A solid AI

debt payoff planner doesn't need you to be perfect. It needs you to connect

your accounts, choose an approach, and not cancel the subscription before the

math has time to work. The tools have gotten genuinely good.

If you're

overwhelmed, Undebt.it is free and will show you your options without asking

for your credit card. That's a reasonable first step.

This article is for information only. It's not financial advice. Check current pricing with vendors before buying.

Financial Disclaimer

The information published on Tech Capital Hub is intended for educational and informational purposes only. Nothing on this website — including articles, guides, analysis, or commentary on AI, fintech, blockchain, cryptocurrency, or stocks — should be interpreted as financial advice, investment advice, trading recommendations, or any other form of professional financial guidance.

All investments carry risk, including the potential loss of principal. Past performance of any financial instrument, strategy, or technology is not a reliable indicator of future results. Cryptocurrency and blockchain-based assets are particularly volatile and speculative in nature, and their value can fluctuate significantly in short periods of time.

Tech Capital Hub, Marcus Delray, and any associated contributors do not hold responsibility for any financial decisions you make based on content published on this site. Before making any investment or financial decision, we strongly encourage you to conduct your own independent research and consult with a licensed financial advisor, accountant, or legal professional who understands your personal financial situation.

Any links to third-party websites, tools, or platforms are provided for convenience and informational purposes only. Tech Capital Hub does not endorse or take responsibility for the content, accuracy, or practices of any third-party sites.