Robo-Advisors for Beginners: Let AI Grow Your Wealth While You Sleep (2026 Guide)

Three years ago I asked a friend who works in finance where I should put my savings. He spent 20 minutes explaining things I didn't understand, mentioned a guy named Vanguard like he was a person, and suggested I open a brokerage account and "just pick some ETFs."

I did not open a brokerage account. I did not pick some ETFs. I put the money in a savings account paying 0.4% and tried not to think about it.

This, I would later learn, is what most people do. And it costs us a lot.

The whole point of a robo advisors for beginners — and I mean this sincerely — is that you don't need to know what an ETF is. You don't need a friend in finance. You answer like eight questions, connect your bank, and then something genuinely smart happens to your money while you're at work or asleep or watching TV.

Let me explain what that actually looks like.

The Stuff the Software Actually Does (And Why It Matters)

When you sign up for one of these platforms, you go through a short questionnaire. How old are you. When do you want this money. What happens inside you when markets drop — do you stay calm or do you start sweating. Based on your answers, the platform builds a portfolio out of low-cost index funds (those are the ETFs) spread across stocks, bonds, international markets.

Then it manages that portfolio. Forever. Without you.

Automatic portfolio rebalancing is the unglamorous thing that makes this work. Say your target is 70% stocks, 30% bonds. Stocks have a good year, now you're at 80/20. Without rebalancing you'd slowly drift into a riskier position than you chose — which feels fine in a bull market until it isn't. The software fixes this automatically, usually daily or when you drift past a threshold. No action required from you.

Tax-loss harvesting is the feature that sounds boring and then surprises you. When a position you hold goes down, the platform sells it, claims the loss against your gains for tax purposes, then immediately buys something similar enough that you're still invested the same way. Done consistently, this can be worth 0.77% a year or more in after-tax returns. That's not huge in a single year. Compounded over decades it absolutely is.

Here's the thing nobody warns you about though: none of that matters if you panic and sell when things drop.

The behavioral piece is underrated. Automated investing is partly about optimization and partly about removing decisions from moments when you're emotionally compromised. The platform doesn't freak out in a crash. It just rebalances. Whether you also freak out is up to you, but the structure helps.

Which Platform Should You Actually Use

I want to be honest with you: this section is where most articles start lying, either because they get paid for referrals or because they're trying to seem comprehensive. I'm going to tell you what I actually think.

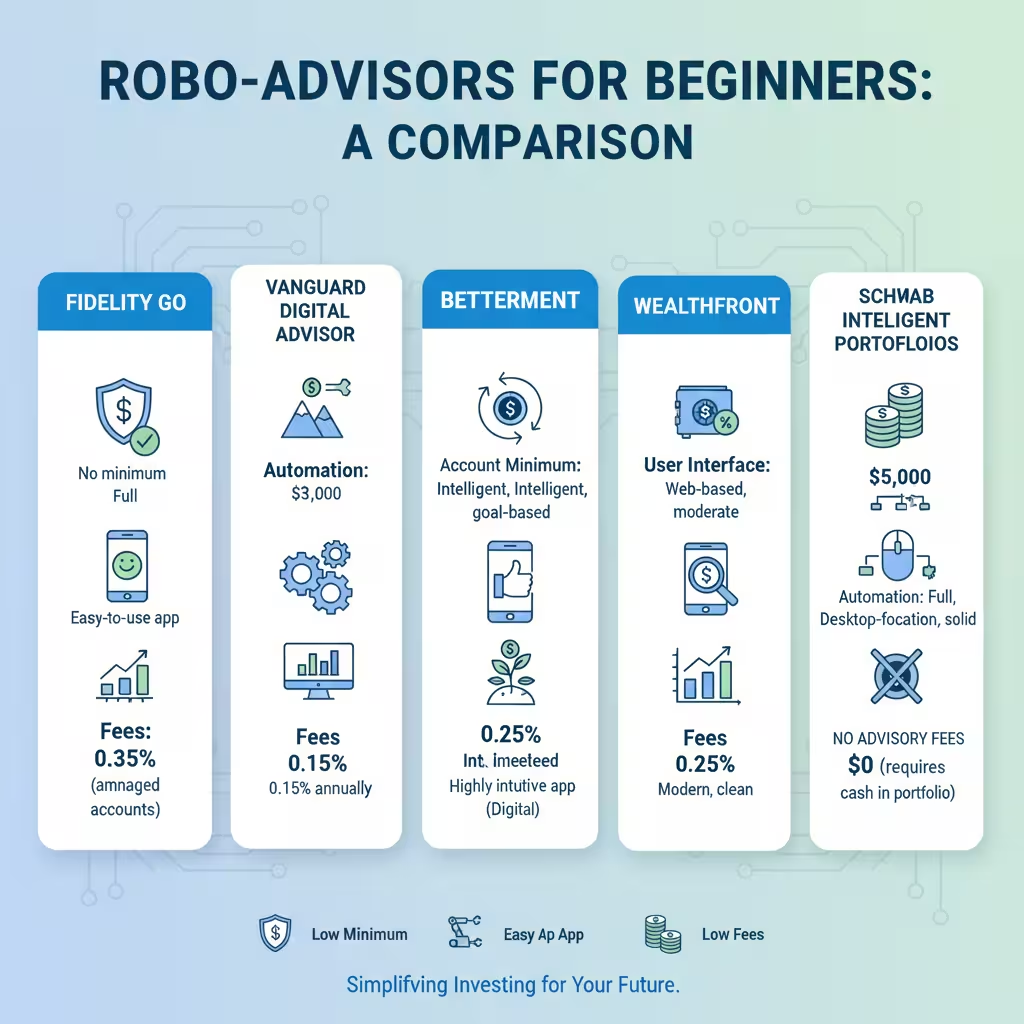

Start with Fidelity Go if you have no idea what you're doing and don't want to pay anything.

Zero minimum. Zero advisory fee for balances under $25,000. And — this is the part that actually matters — zero expense ratios on the funds inside the account, because Fidelity uses its own internal Flex funds. Most platforms charge a small management fee AND the funds inside the account have their own tiny fees on top. Fidelity just doesn't. If you have under $25K, your all-in cost is genuinely nothing.

Real humans at Strategic Advisers LLC review all the trades, which is a small thing but sort of reassuring when you're new. And once you've built up to $25,000, you get coaching calls with actual advisors. Unlimited. Thirty minutes each. That's not bad for a free account.

I'd push back on one thing though. The 0.35% fee that kicks in above $25K — that's fine, but at that point you should probably compare it to Vanguard, which typically runs around 0.15%–0.16% net. Depends on your situation.

Vanguardis the one you graduate into, not the one you start with.

Their digital advisor is excellent for long-term, disciplined, boring investing. And boring is good. The glide path feature adjusts your ETF allocation over time as you age and your circumstances change — they've built over 300 different paths based on age, risk tolerance, marital status, goal timeline. That level of personalization is real, not marketing.

The $100 minimum is low enough that it's technically a beginner platform. I just think most real beginners find Fidelity's zero-fee zero-minimum a cleaner entry point, and Vanguard is where you migrate when you're more established and care about squeezing every basis point.

Bettermentis the one for people who think in goals rather than one big pot.

The idea is you create separate investment buckets — retirement, emergency fund, house down payment, vacation, whatever. Each bucket gets its own risk level and timeline. It sounds like a gimmick until you actually use it and realize it completely changes how you think about money.

The fee is 0.25% annually. There's a trap though. If your balance is under $24,000 and you don't have a $250+ monthly recurring deposit set up, you pay $5 flat per month instead. On a $500 account that's a 12% annual fee. On $2,000 that's still 3%. Set up the automatic deposit or you're getting eaten alive by that flat fee.

I'd also mention: Betterment is genuinely the best option for people who worry about downside. Their minimax approach is built to reduce worst-case losses across your specific time horizon, not just chase the highest average return. If market drops make you anxious, that matters.

Wealthfront is for later, not now — unless you're already earning well and investing in a taxable account.

The platform is technically impressive. The direct indexing feature available at $100,000+ — where they buy the actual individual stocks inside an index instead of an ETF wrapper — is legitimately sophisticated. It massively increases tax-loss harvesting opportunities. The FDIC insurance they offer through partner banks goes up to $8 million. The 0.25% fee is the same as Betterment but you get more tax sophistication.

For someone just starting out with $500? It's fine, but the features that make it worth it don't really kick in until you've built up significantly. Keep it in mind for later.

Schwab is genuinely free and genuinely has a catch.

No advisory fee. Real. But every portfolio holds 7–15% in cash, earning 3.31% APY as of early 2026. Schwab earns money on the spread between what they make on that cash and what they pay you. In a good year for stocks, that cash underperforms what it would've done invested. In a bad year, it's a cushion.

Whether this is a good deal is math-dependent. Run your specific numbers. The $5,000 minimum also means it's not really a beginner-first option — it's for people who already have something saved.

The Part About Human Advisors (Brief, Because It Doesn't Have to Be Complicated)

Traditional financial advisors charge around 1% of assets annually. On $50,000 that's $500. On $300,000 that's $3,000. Every year. The math erodes your returns meaningfully over time.

The question of robo advisor vs financial advisor which is better is less interesting than people make it. For building wealth in your 20s and 30s, automated investing wins on cost almost every time. Where a human advisor genuinely earns their fee is complex situations — estate planning, business sales, divorce, kids with special needs, multi-generational wealth. None of those apply to most people starting out.

And plenty of robo platforms now give you access to real people anyway. Fidelity Go at $25K. Betterment Premium at $100K with certified financial planners. So it's not a permanent either/or choice.

Start automated. Add human expertise when your situation actually warrants it.

The Quick Numbers

| Platform | Minimum | Fee | What makes it worth considering |

| Fidelity Go | $10 | $0 under $25K, then 0.35% | Zero all-in cost while building |

| Vanguard Digital | $100 | ~0.15% net | Lowest long-term cost, great glide paths |

| Betterment | $10 | 0.25% or $5/mo | Goal buckets, downside protection |

| Wealthfront | $500 | 0.25% | Best tax tools, especially at $100K+ |

| Schwab | $5,000 | $0 | Free advisory fee, cash tradeoff |

Three Questions Worth Answering Before You Pick

What are you actually starting with? If it's under $500, Fidelity Go or Betterment. If it's $5,000+, Schwab enters the picture but calculate the cash drag first. If you're somewhere in the middle, Vanguard or Wealthfront are both reasonable.

How do you actually handle market drops? Not how you think you handle them — how you actually respond when your account is down 25% and everyone's panicking. If the honest answer is "badly," lean toward Betterment's downside approach and build toward Fidelity's coaching threshold.

Is this a taxable account or a retirement account? In a 401(k) or IRA, tax-loss harvesting is irrelevant — the account is already sheltered. In a taxable brokerage account, especially at higher income levels, the tax tools at Wealthfront can justify the choice purely on after-tax math.

Frequently Asked Questions (FAQs)

I've heard robo advisors aren't "real" investing. Is that true?

No. Passive investing through diversified, low-cost index funds is what the majority of financial research suggests beats active stock-picking for most retail investors over long time horizons. The "real investing" critique usually comes from people who enjoy picking stocks. That's fine — but it's not more legitimate.

What's the best robo advisors for first-time investors with low fees?

Fidelity Go. Zero minimum, zero fee under $25K, zero expense ratios on underlying funds. Until your balance outgrows it, nothing cheaper exists.

What happens if the company goes out of business?

Your assets are held separately from the company's own funds and are covered by SIPC insurance up to $500,000. The company going under doesn't mean your investments disappear — they'd be transferred or you'd receive them directly.

What does portfolio rebalancing actually do for me?

It keeps you at your chosen risk level. Without it, a good stock year could quietly push you from a moderate portfolio into an aggressive one — which you'd notice painfully when things eventually correct. Rebalancing is the thing that keeps your risk tolerance settings meaningful over time.

Is there any reason NOT to use robo advisors?

If you genuinely enjoy researching individual stocks and you have time to manage your own portfolio, maybe. If you're already working with a fee-only financial advisor who charges flat rates, check whether their fee beats 0.25%. Otherwise, for most people without a specific reason to go another route, automated investing through a low cost robo advisors just works.

Okay, Just Start

I've said everything useful I have to say. The rest is you making a decision.

Fidelity Go for most people, because zero fees while you're building. Betterment if the goal-based structure fits your brain. Vanguard when you've got $100+ and care about the long game. Wealthfront when you're earning well and taxable accounts matter. Schwab if you want zero advisory fees and you've already got $5K sitting around.

Pick one. Open the account. Set up an automatic monthly deposit, whatever you can manage — even $50 makes a difference over time because of how compounding works. Then genuinely don't look at it for a few months.

That's the whole thing. Robo advisors for beginners exists specifically so the "I'll figure it out someday" excuse stops working. The figuring out is already done for you.

Go open the account.

Financial Disclaimer

The information published on Tech Capital Hub is intended for educational and informational purposes only. Nothing on this website — including articles, guides, analysis, or commentary on AI, fintech, blockchain, cryptocurrency, or stocks — should be interpreted as financial advice, investment advice, trading recommendations, or any other form of professional financial guidance.

All investments carry risk, including the potential loss of principal. Past performance of any financial instrument, strategy, or technology is not a reliable indicator of future results. Cryptocurrency and blockchain-based assets are particularly volatile and speculative in nature, and their value can fluctuate significantly in short periods of time.

Tech Capital Hub, Marcus Delray, and any associated contributors do not hold responsibility for any financial decisions you make based on content published on this site. Before making any investment or financial decision, we strongly encourage you to conduct your own independent research and consult with a licensed financial advisor, accountant, or legal professional who understands your personal financial situation.

Any links to third-party websites, tools, or platforms are provided for convenience and informational purposes only. Tech Capital Hub does not endorse or take responsibility for the content, accuracy, or practices of any third-party sites.