How AI Can Boost Your Credit Score Faster Than Any Bank Will Tell You

Nobody at the bank is sitting you down for this conversation.

And honestly? That's kind of the point.

The scoring system running your financial life just got the biggest

overhaul in 30 years. Not a tweak. Not a pilot program somewhere. A full

structural shift — one where the tools that used to belong only to lenders and

hedge funds are now sitting in your app store, mostly free or close to it.

AI credit score tools are what changed the math here. Platforms like

Arro, BON Credit, and Experian Boost read your financial behavior in real time,

spot what's dragging your score down, and tell you what to actually do about it

— before your next statement closes, not after.

Your bank isn't going to hand you that playbook. This guide will.

Heads up: Some links here are affiliate links. If you sign up through

them, we may earn a small commission at no extra cost to you. Doesn't change

what we recommend.

What Just Changed — And Why It Actually Matters for You

Let's start with the uncomfortable part.

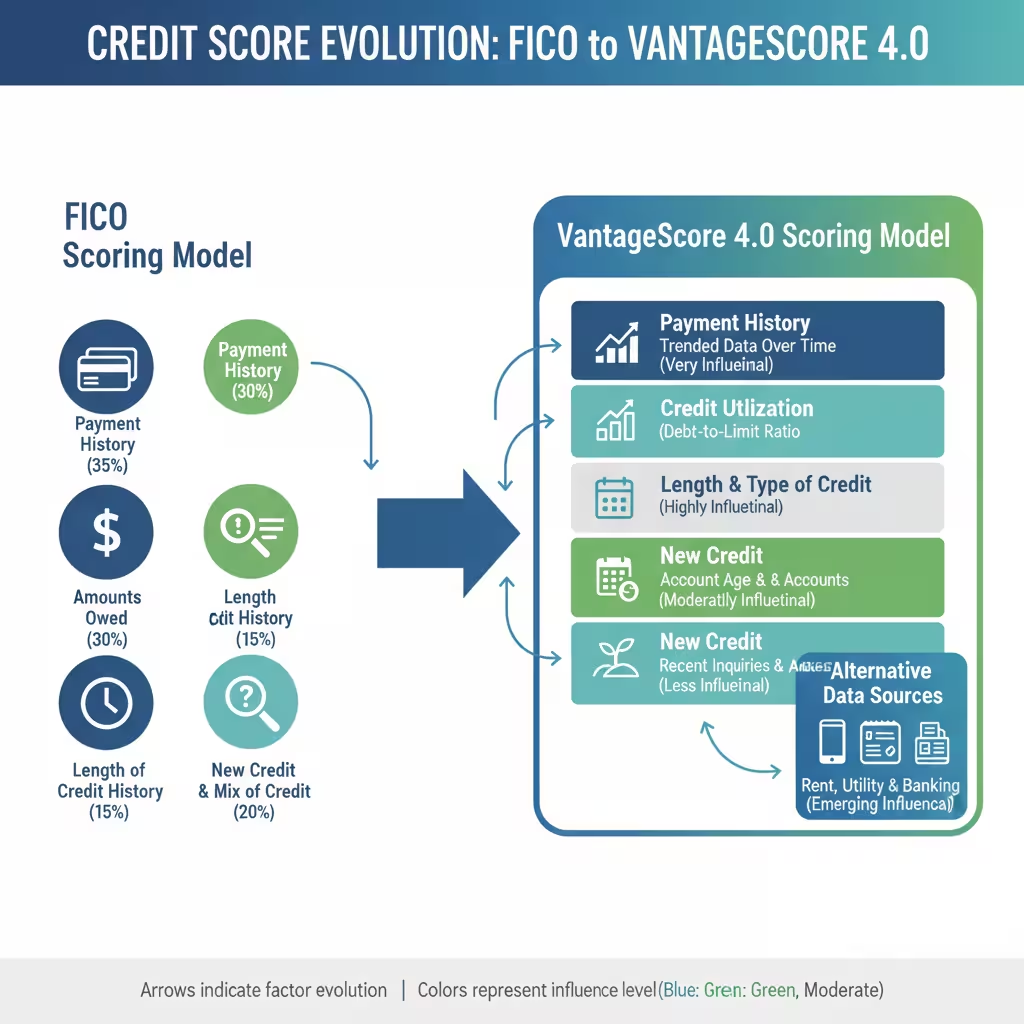

Between 2021 and 2026, FICO raised its per-pull mortgage score price from

$0.60 to $10.00. That's not a typo. A 16x increase in five years. Lenders were

bleeding money on every single application, and they had no real alternative —

until they did.

The Federal Housing Finance Agency stepped in. Starting in 2025,

VantageScore 4.0 became the required model for all mortgages sold to Fannie Mae

and Freddie Mac. FICO's grip on the mortgage market cracked open for the first

time in decades.

Here's why that matters to you personally.

VantageScore 4.0 doesn't just look at your debt. It tracks patterns — how

your balance moves month to month, whether your payments are trending up or

down, what your cash flow actually looks like. It also scores the 33 million

Americans who were completely invisible to the old system. Renters.

Freelancers. Gig workers. Students who never touched a credit card.

If you've been paying bills on time for years but couldn't get a decent

score because you weren't carrying the "right" kind of debt — that

era is over.

You need tools built for the new model, though. Because the old playbook doesn't apply anymore.

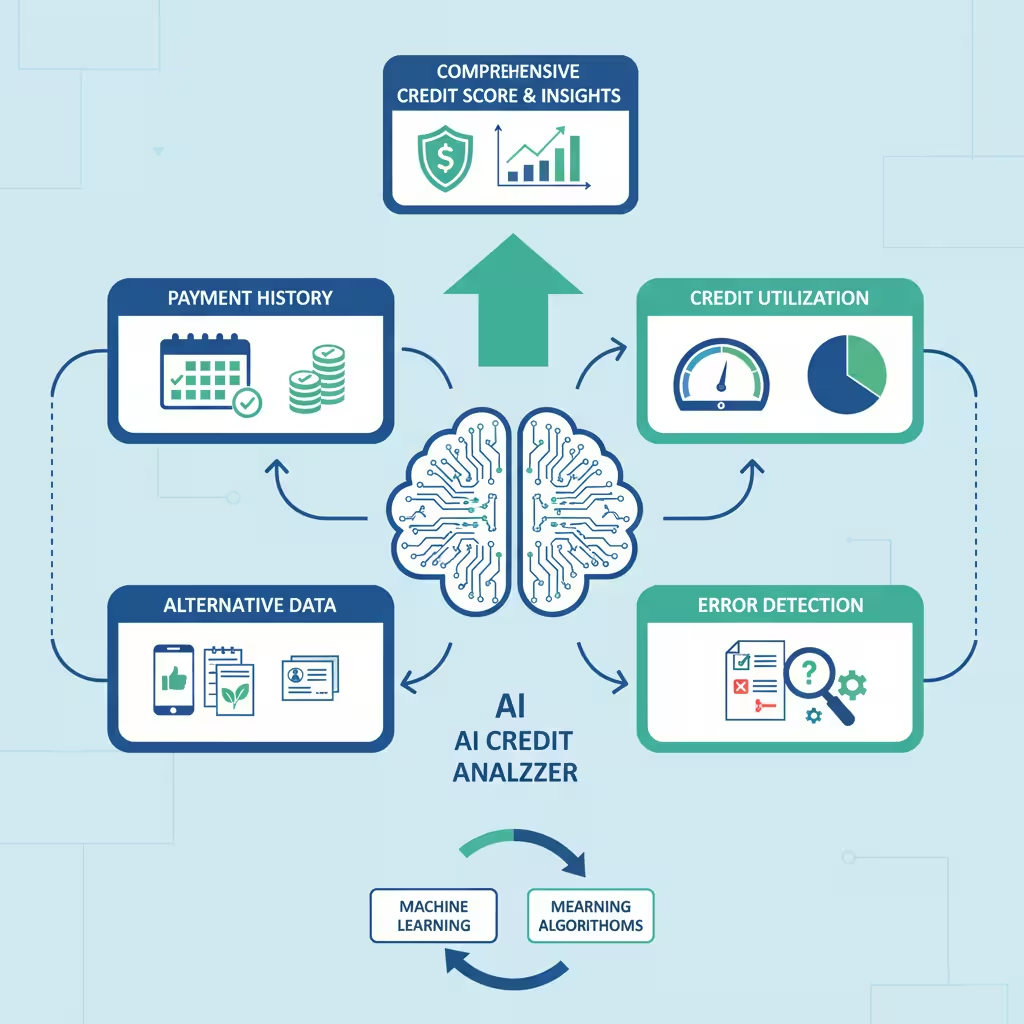

What AI Credit Score Tools Are Actually Doing in the Background

Most people think credit monitoring means checking your number once a

month. That's not this.

Real AI credit monitoring runs continuously. It's watching your payment

behavior across every linked account, flagging timing problems before they hit

your report, and scanning your existing bills for credit-building opportunities

you're probably missing entirely.

Here's what's actually running when you use something like Arro or BON

Credit:

Payment history analysis. The AI looks at trajectory, not just your record. One rough month from

three years ago doesn't define you — 14 straight months of on-time payments

does. Under VantageScore 4.0's trended data model, that direction is weighted

heavily. The system is asking: is this person getting more reliable over time,

or less?

Credit utilization tracking. The old rule is keep it under 30%. Top AI tools push for under 10% — and

here's the part most people never figure out on their own: utilization is

calculated when your statement closes, not when you pay. So if you're carrying

$2,200 on a $5,000 card and your statement closes Thursday, you've already

reported 44% utilization to the bureaus. Even if you pay it off on Friday. The

AI flags this before Thursday, not after.

Alternative data identification. This is honestly where the biggest gains are hiding. AI tools scan your

connected accounts and identify which bills — rent, phone, electricity,

streaming — can be reported to Experian, Equifax, or TransUnion through

services like Experian Boost. Payments you're already making every month. Not

getting any credit for. That ends the day you connect them.

Error detection. One in five credit reports contains a material mistake. Dovly runs automated scans across all three bureaus and flags anything worth disputing. No spreadsheets, no certified mail — just a flag and a next step.

Two AI Platforms Worth Your Money Right Now

(Pricing confirmed as of February 2026 — verify before you sign up,

things change fast in this space)

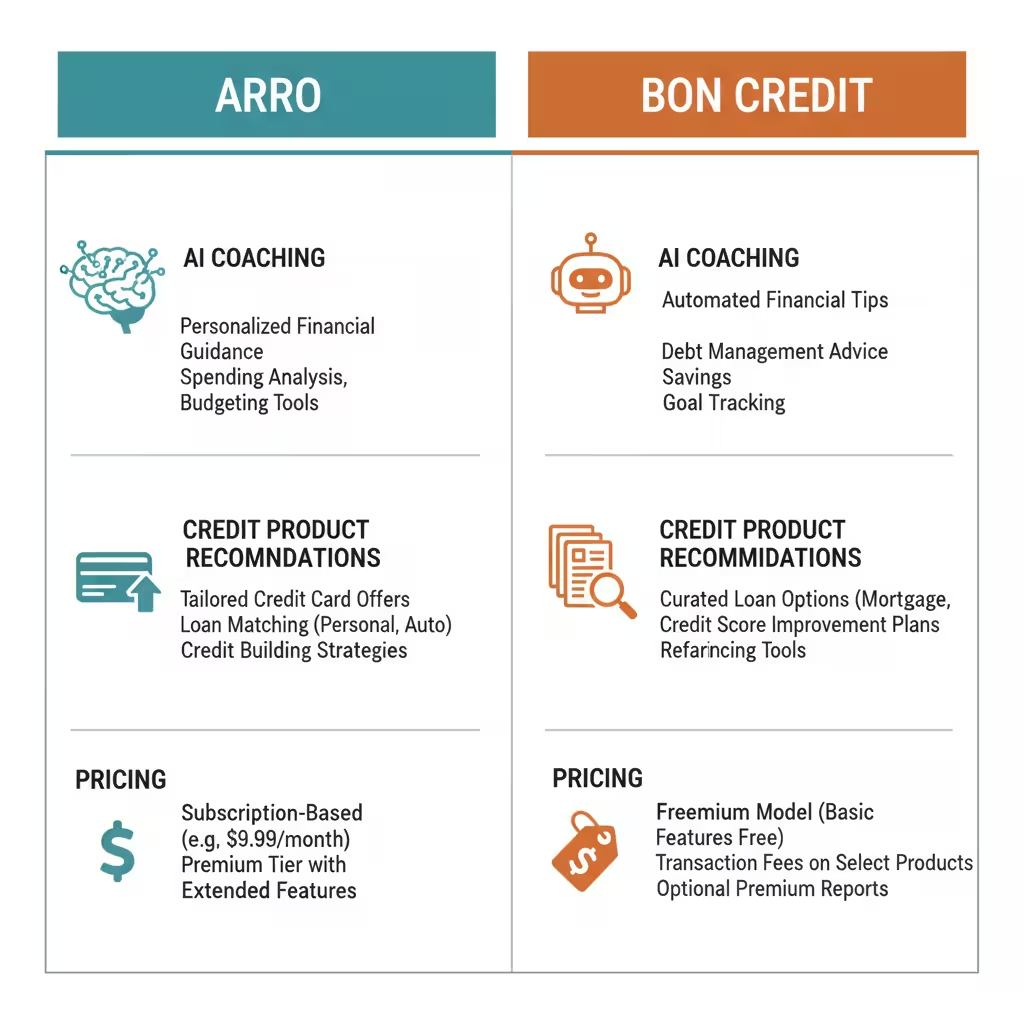

Arro — $12/month

Arro is built around one specific destination: a real revolving credit

card. Not a tradeline. Not a credit-builder loan. An actual card with a limit

that reports to lenders as open-ended revolving credit.

The AI coach is called Artie. It's available around the clock — you can

ask it why your score moved, what to pay and when, whether you're on track.

What makes it different from other coaching tools is that Artie shows you the

behavioral reason behind each recommendation. Not "reduce your

utilization." More like: "Your Chase card reports on the 17th and

your current balance would report at 38% — pay $420 before then to drop it

under 10%."

That specificity is worth the $12, honestly.

Arro reports to Experian and Equifax. The path to the Arro Card takes a

few months of consistent behavior, but that's the point — it's building a

verified track record, not just adding a line to your file.

BON Credit — Free (basic version)

BON Credit's AI is called CredGPT, and it works differently. Instead of

coaching you on what to do with what you have, it scans over 14,000 credit

products to find what you should get next — based on your actual profile, not a

FICO bucket.

It connects through Plaid, so it's reading your real bank data. When you

don't know whether to apply for a secured card or a store card or a

credit-builder loan — CredGPT tells you which one you'll actually get approved

for and which one helps your profile most. That "which product first"

question trips up a lot of people. Hard inquiries from declined applications

hurt your score, so the matchmaking matters.

Premium features are coming later in 2026. For now, the free version is

genuinely useful.

One thing to note about revolving credit, since it comes up a lot: a tradeline (like from Kikoff) proves you have an account. A revolving card proves you can manage an open credit line responsibly over time. Future lenders — especially mortgage lenders — read those two things very differently. Kikoff at $5/month is fine as a starting tradeline. It's not a replacement for working toward a real card.

The 15/3 Method — This Is the One Most People Find Out About Too Late

No elaborate setup required for this one. Just a timing change.

Your utilization ratio is based on the balance your card reports when

your statement closes. Not when you pay. Not your average balance. The snapshot

on the day the statement generates.

So if your statement closes on the 20th and you're carrying $1,800 on a

$4,000 card, you're reporting 45% utilization to the bureaus — even if you pay

the whole thing on the 21st and your account hits zero. Lenders already got

that 45% number. It's on your file.

The 15/3 method is a payment timing fix:

- 15 days before your statement

closes: Pay down roughly half of whatever you're carrying.

- 3 days before it closes: Pay the rest down to near zero.

- What the bureau sees: Consistently low utilization

month after month.

VantageScore 4.0 specifically rewards that pattern. Not a one-time payoff

before a loan application — a pattern. Two or three months of this and the

trended data starts working in your favor in a way it doesn't with the old FICO

snapshot model.

Arro's Artie tracks your close dates and sends reminders. You don't have

to remember any of this yourself.

Most people who find out about the 15/3 method are annoyed they didn't know sooner. Now you do.

Improving Credit With AI Using Bills You Already Pay Every Month

Here's something that surprises people: if you're paying rent, utilities,

and a phone bill consistently — you're already demonstrating creditworthiness.

The problem is that none of it is showing up in your file.

Rent. This is the biggest one. If you pay through a property management

portal, that payment can now be reported to Experian through Experian Boost.

Cash and Venmo don't count — it needs to be a bank-linked transaction. But for

renters with no credit history? On-time rent is the strongest signal in your

file. Lenders read it the same way they'd read a mortgage payment: you show up

every month for a large, non-optional bill.

Utilities. Electricity, gas, water — all of it now counts. Consistent payments on

these flag you as someone who handles essential obligations before

discretionary ones. That's low-risk borrower behavior, and lenders know it.

Your phone and streaming. Under Experian Boost, your cell bill and home internet count as

tradelines. Netflix and Disney+ build your Experian file too, as long as the

payment pulls from a connected bank account rather than a manually entered

card.

The setup: go to Experian Boost, connect your checking account, let it pull 24 months of qualifying payments. A lot of users see a score jump within 24 hours. It takes about 10 minutes and costs nothing.

A Real Timeline: What Happens Over 90 Days With AI Credit Monitoring

If you're building from scratch — or rebuilding — here's what honest

progress actually looks like, not the optimistic version.

Days 1 to 30. Pull your free reports at AnnualCreditReport.com. Don't just glance at

the number — read the actual entries. Look for duplicate accounts, addresses

that aren't yours, any account you don't recognize. Use Dovly to flag and

dispute anything suspicious. Activate Experian Boost and connect your bank

account so your bills start building history. Check that your Equifax file

shows your employment through The Work Number Report Indicator — it signals

income stability to lenders automatically, without you having to upload

documents.

Days 30 to 60. Start the 15/3 timing habit on every card you carry a balance on. Enroll

in Arro or BON Credit for guidance specific to your file. If you have zero

credit history at all, add Kikoff at $5/month — it's an easy tradeline on all

three bureaus while you work toward something more substantial.

Days 60 to 90. This is when trended data actually kicks in. VantageScore 4.0 rewards

patterns, and 60 to 90 days of clean behavior is when meaningful score movement

tends to show up. If Artie flags a plateau, it'll suggest a credit mix

adjustment — sometimes a credit-builder loan, sometimes a second card.

Sixty days isn't a guarantee. What it is: a real window if you're consistent.

One Specific Warning — Don't Skip This Part

Not every credit platform is worth your business. Most are fine. One

isn't.

TomoCredit. Avoid it. The Better Business Bureau gives it an "F" rating.

There are documented legal challenges, reported unauthorized withdrawals, and a

long trail of complaints about subscriptions that are nearly impossible to

cancel. A credit platform that's hard to cancel is a problem you don't need to

add to your financial life right now.

Dovly ($0 to $39.99/month depending on the plan) is fine for dispute-focused

monitoring. The free version covers basic TransUnion monitoring. The $39.99

plan adds a $2,000 tradeline. Worth it if dispute resolution is your main need.

Kikoff at $5/month is legitimate and reports to all three bureaus. Go in knowing the cancellation process is slow and customer service is inconsistent. Use it as a tradeline starter. Don't expect more than that.

Frequently Asked Questions

How fast can AI improve my credit score? Thirty to sixty days is realistic for

measurable movement, if you're applying the 15/3 habit and Experian Boost at

the same time. Enough movement to change your loan tier — what lenders call a

tier upgrade, which can mean a meaningfully lower interest rate — usually takes

60 to 90 days of consistent behavior. AI doesn't manufacture results. It

removes the guesswork so your consistent behavior actually compounds.

What's the best AI app to monitor and improve my credit score? Depends what you're optimizing for.

If you want a clear path to a revolving credit card, Arro is the right call. If

you're starting with no cards and need to figure out which product to apply for

first, BON Credit's CredGPT is where to start. Both are worth having if your

budget allows — they serve different functions and don't overlap much.

Can AI help if I'm credit invisible? Yes — and this is the part of the 2026 shift that

doesn't get enough attention. VantageScore 4.0 was built specifically to score

the 33 million Americans who had zero FICO score. AI tools that connect your

rent, utility bills, and cash flow to your credit file can make you visible to

mortgage lenders, car lenders, and card issuers — without any traditional debt

on your record at all.

Does credit utilization matter more than payment history? Payment history is the most important

factor, full stop. One missed payment can stay on your report for seven years.

But utilization is the fastest factor you can actually move right now. Good AI

credit monitoring tools handle both at the same time — they alert you before

you miss a payment and flag rising utilization before your statement closes.

How is AI credit monitoring different from a standard credit alert? A credit alert tells you after

something already happened. AI credit monitoring tools like Arro and BON Credit

tell you what to do before the score changes. That's the whole difference.

Reactive vs. proactive.

Will using multiple AI tools hurt my score? No. Signing up for monitoring platforms doesn't trigger hard inquiries. Only applying for new credit — a card, a loan — creates a hard pull. You can run Arro, BON Credit, Experian Boost, and Dovly simultaneously with zero score impact from the tools themselves.

The Bank Isn't Going to Hand You This

There's a reason none of this is in the brochure at the teller window.

An informed borrower negotiates harder. Shops around. Costs more to

retain. That's not a criticism of banks specifically — it's just how the

incentive structure works. Institutions don't build tools designed to give

customers the upper hand.

But the credit system changed. VantageScore 4.0 is now the mortgage

standard. Your rent and your Netflix and your electric bill count now. And AI

tools that track all of it in real time are available, they're affordable, and

they genuinely work.

Start with Experian Boost. Ten minutes, costs nothing, you may see a

score bump by tomorrow. Then pick one AI platform — Arro if you want a

revolving card on the horizon, BON Credit if you need help figuring out which

product to go after first. Apply the 15/3 timing to every card you carry. Run

it for 60 days.

The system finally works for people who understand it.

You do now.

This article is for informational purposes only. It's not financial or legal advice. Credit outcomes vary by individual. Pricing and features for third-party platforms change — confirm directly with each provider before enrolling.

Financial Disclaimer

The information published on Tech Capital Hub is intended for educational and informational purposes only. Nothing on this website — including articles, guides, analysis, or commentary on AI, fintech, blockchain, cryptocurrency, or stocks — should be interpreted as financial advice, investment advice, trading recommendations, or any other form of professional financial guidance.

All investments carry risk, including the potential loss of principal. Past performance of any financial instrument, strategy, or technology is not a reliable indicator of future results. Cryptocurrency and blockchain-based assets are particularly volatile and speculative in nature, and their value can fluctuate significantly in short periods of time.

Tech Capital Hub, Marcus Delray, and any associated contributors do not hold responsibility for any financial decisions you make based on content published on this site. Before making any investment or financial decision, we strongly encourage you to conduct your own independent research and consult with a licensed financial advisor, accountant, or legal professional who understands your personal financial situation.

Any links to third-party websites, tools, or platforms are provided for convenience and informational purposes only. Tech Capital Hub does not endorse or take responsibility for the content, accuracy, or practices of any third-party sites.