AI in Personal Finance: How Artificial Intelligence Is Quietly Managing Your Money in 2026

Last October, I got a text from my bank at 7:14 in the morning. A $312 charge had been flagged — a furniture store in Phoenix. I've never been to Phoenix.

By the time I opened the app, the card was already frozen. Nobody called me. Nobody filed a report. The AI caught it, acted on it, and sent me the text all before I'd even poured my coffee.

That's the version of AI personal finance tools that actually exists right now. Not the glossy demo videos. Not the "coming soon" features in press releases. The version that's already sitting inside your bank account, working quietly while you sleep.

Most people I talk to have this vague sense that AI is changing money stuff — but they picture it as something happening at hedge funds or inside Goldman Sachs trading algorithms. Not something that touches their checking account or their grocery budget.

But that's changed pretty dramatically. And 2026 is the year a lot of it clicked into place.

The financial apps that most Americans use every day — budgeting tools, banking apps, investment platforms — have spent the last two or three years layering actual intelligence into what used to be pretty passive software. A 2025 Citizens Bank report found that midsize financial institutions are seeing average ROI of around 35% on AI investments. The reason it's showing up in consumer tools now is simple: the underlying technology got good enough, and cheap enough, to push down to everyday products.

The Budgeting Problem AI Actually Solved

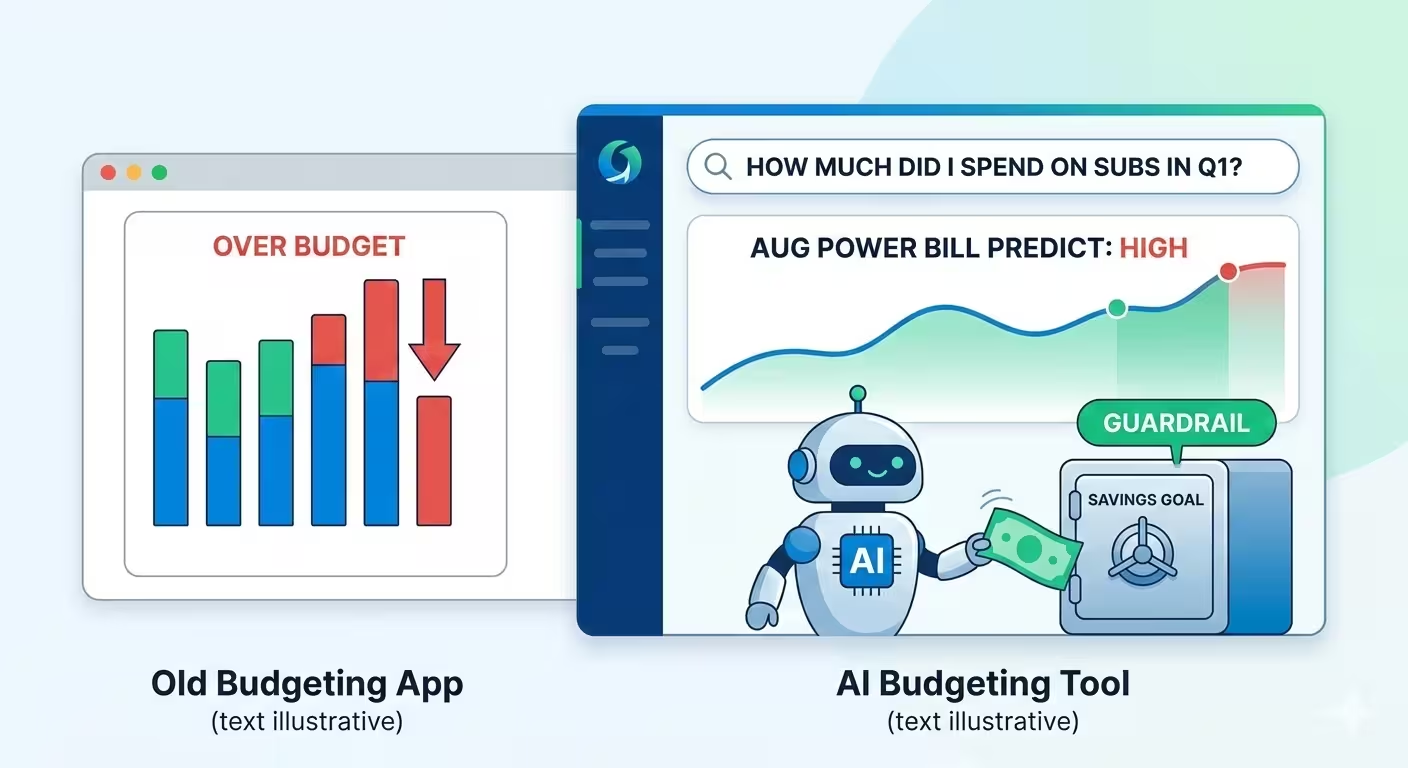

I used Mint for years. If you're not familiar, it was one of the original personal finance apps — connected to your accounts, tracked your spending, told you when you went over budget.

Here's the thing, though. It told you after. You'd blow your dining budget by $80, and Mint would dutifully log it. Cool. Already spent.

Artificial intelligence budgeting tools work differently because they're not just logging — they're modeling. Your app builds a picture of your financial behavior over time and uses that to look forward, not just backward. If your electricity bill always spikes in August, the AI has already factored that in. If you've got a pattern of impulse spending the Thursday after payday — and a lot of us do — a decent AI budgeting app will catch that pattern and flag it before Thursday rolls around.

Apps like Copilot Money and Monarch Money have built this kind of predictive layer into their core features. What genuinely surprised me when I started using one of these more seriously was the natural language search. You can type something like "how much did I spend on subscriptions in Q1?" and get an answer in two seconds. No spreadsheet. No hunting through statements.

The automated savings features have also gotten a lot smarter. Not just the round-up stuff — though that still works fine. I'm talking about apps that look at your account balance, check what bills are coming up in the next ten days, and then move an amount into savings that the AI calculates you can actually spare. The timing matters. Moving $50 into savings the day before a $400 insurance payment is a bad idea. A good AI money management app knows that.

Robo-Advisors: AI Finance Apps That Stopped Being a Niche Thing

Five years ago, robo-advisors felt like something for people who were already financially savvy but didn't want to pay advisor fees. A bit niche.

That's shifted. A lot.

Platforms like Betterment, Wealthfront, and SoFi Invest now handle the full cycle — building a diversified portfolio based on your goals and risk tolerance, rebalancing when markets move, adjusting allocation as you get closer to whatever target you've set. The fees are usually around 0.25% annually. On a $15,000 account, that's about $37.50 a year.

A traditional financial advisor managing that same account would typically charge ten to twenty times that. Which — fine, sometimes the human expertise is worth it. Estate planning, a complicated business situation, a major inheritance. Those aren't robo-advisor territory. But steady long-term investing toward retirement or a down payment? The AI does it better than most of us would on our own, and it never panics when the market drops 8% in a week.

That last part isn't a small thing, by the way. Behavioral finance research has shown for decades that the biggest enemy of investment returns isn't market volatility — it's investors making emotional decisions during volatile periods. The AI doesn't have emotions. It just rebalances.

There's a piece of this that doesn't get talked about much, and it's probably the most consequential: Fraud Detection

The system protecting your money right now is monitoring a lot more than just whether a charge looks weird. It's tracking your typical purchase locations, the merchants you use regularly, what time of day you tend to spend, how large your transactions usually are. Dozens of signals, running constantly.

When something breaks from your pattern — even slightly — it flags it. Sometimes it freezes the card. Sometimes it just texts you. Either way, it's doing this in seconds, not hours.

Michael Cummins of Citizens Bank described AI as "rewriting both sides of the fraud playbook" in 2025. That framing captures something real: the same technology protecting consumers is also making phishing attacks more convincing and deepfake scams harder to spot. It's genuinely an arms race. But from where I sit as someone who had that Phoenix furniture charge caught before I noticed it? The defensive side is working.

Some platforms are now running identity verification across 400+ digital signals before approving a transaction. The kind of cross-referencing that would've taken a human fraud analyst days to do — the AI completes before a page loads.

What to Actually Look for in AI Personal Finance Tools

Not everything marketed as "AI-powered" is worth your time. Here's what I'd actually look at:

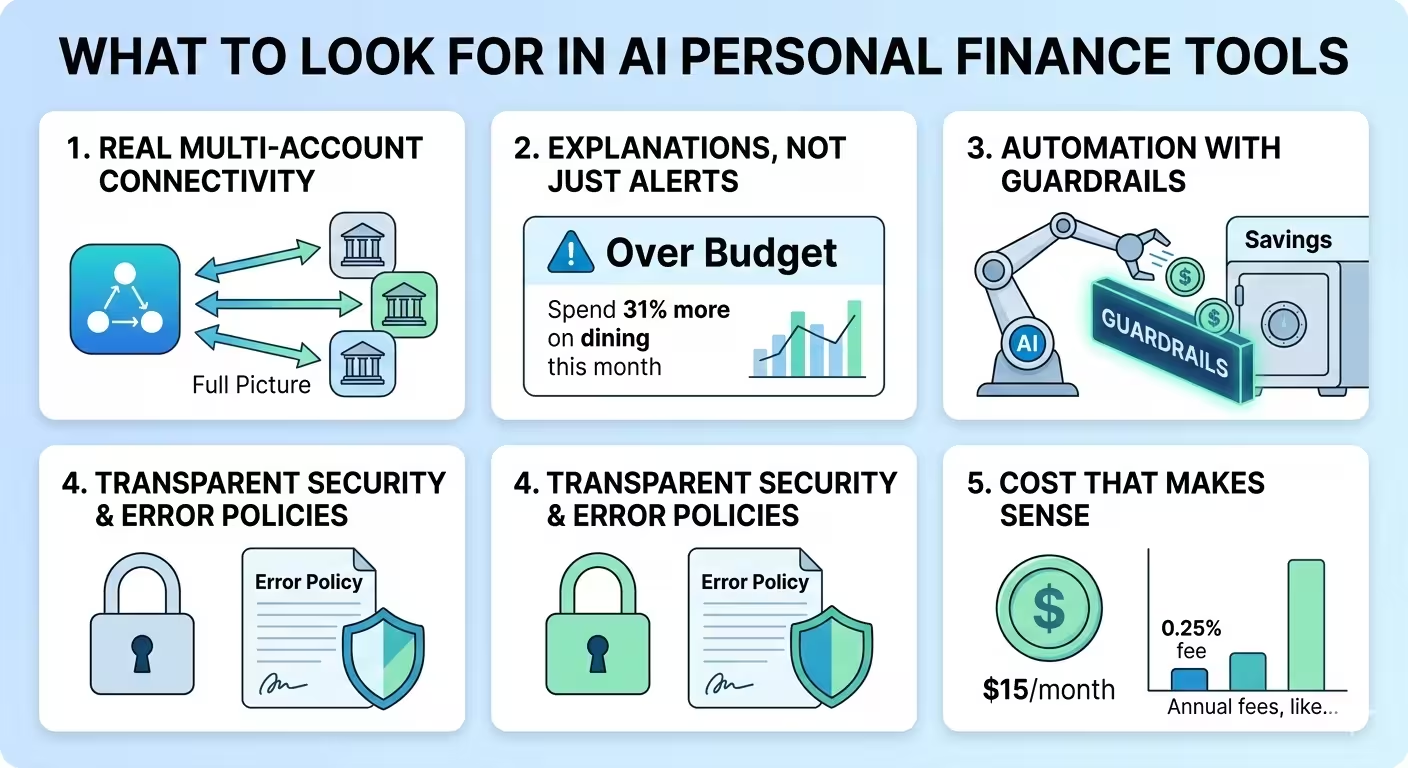

• Real multi-account connectivity. The best AI personal finance tools pull from all your accounts — not just one bank. If it only sees part of your financial picture, the insights are going to be partial too.

• Explanations, not just alerts. An alert that says "you're over budget" is almost useless without context. Good AI finance apps tell you why — "you spent 31% more on dining this month" — so you can actually act on it.

• Automation with guardrails. Automated savings features are great. But you want to control what the AI can do on its own versus what requires your sign-off. The best apps are clear about this.

• Transparent security and error policies. With agentic AI becoming more common in finance, there's a real question forming around liability. Reputable platforms are clear about what happens when something goes wrong. If a company can't explain that, that's a red flag.

• Cost that makes sense. A lot of solid expense tracking AI tools are free or under $15/month. Premium robo-advisors typically charge 0.25–0.50% of your invested assets annually — so $50–$100 per year on a $20,000 portfolio. Be skeptical of anything significantly higher without a clear reason why.

A Note on Staying in Control

All of this technology is genuinely good. I mean that.

But here's something worth sitting with: AI works best when you actually stay engaged with it. The people who get the most out of smart budgeting and financial wellness apps aren't the ones who set it up and disappear. They're the ones who check in, adjust goals when life changes, and treat the AI's output as a starting point for thinking rather than a final answer.

The technology is advancing fast. Your job is to stay at least loosely aware of what it's doing with your money — and to know you always have the right to ask questions.

California's new Automated Decision-Making Technology rules — taking effect January 1, 2027 — will require companies using AI for significant financial decisions to give consumers the right to opt out and appeal those decisions to a human reviewer. That's a healthy development. It keeps a human layer in the loop where it matters most.

Frequently Asked Questions

How does AI help with personal budgeting?

It analyzes your transaction history automatically, categorizes spending, identifies patterns, and flags potential problems before they happen — not after. Unlike traditional apps that just track past spending, AI budgeting tools predict what's coming and give you time to adjust.

Are AI finance apps safe?

Yes, when you're using established platforms. Look for bank-level encryption, clear data policies, and FDIC insurance on any savings features. Avoid giving full banking credentials to any app that isn't well-reviewed and transparent about security.

What's the difference between a robo-advisor and an AI budgeting app?

A robo-advisor manages your investments — building and rebalancing a portfolio automatically. An AI budgeting app handles day-to-day spending, savings, and financial planning. Many people use both for different parts of their financial life.

Can AI apps that track spending and save money automatically work with any bank?Most major platforms support hundreds of U.S. financial institutions. Coverage for smaller credit unions has improved a lot in the past two years, but it's worth confirming before you commit.

How much do AI personal finance tools cost?

Many core features are free or close to it. Premium AI budgeting plans run about $8–$15/month. Robo-advisor fees are typically 0.25–0.50% of your invested assets annually — so they scale with your account size rather than charging a flat monthly fee.

Where Does This Leave You?

Personal finance used to feel like you were always a step behind your own money. You'd check your account at the end of the month, see where things went sideways, vow to do better. Repeat.

AI personal finance tools have changed that dynamic in a real way. The best ones shift you from reactive to proactive — from discovering problems after the fact to having a system that catches them first. In 2026, those tools are more capable, more accessible, and more woven into everyday financial life than they've ever been.

You don't have to overhaul everything at once. Start with a smart budgeting app. Set up a robo-advisor for money you're not going to touch for a few years. Let your bank's fraud AI do its thing in the background. None of these are big commitments — and the cumulative effect on your financial wellness is worth it.

The main thing is just getting started. The slow, manual way of managing money still works. It's just not your only option anymore.

Financial Disclaimer

The information published on Tech Capital Hub is intended for educational and informational purposes only. Nothing on this website — including articles, guides, analysis, or commentary on AI, fintech, blockchain, cryptocurrency, or stocks — should be interpreted as financial advice, investment advice, trading recommendations, or any other form of professional financial guidance.

All investments carry risk, including the potential loss of principal. Past performance of any financial instrument, strategy, or technology is not a reliable indicator of future results. Cryptocurrency and blockchain-based assets are particularly volatile and speculative in nature, and their value can fluctuate significantly in short periods of time.

Tech Capital Hub, Marcus Delray, and any associated contributors do not hold responsibility for any financial decisions you make based on content published on this site. Before making any investment or financial decision, we strongly encourage you to conduct your own independent research and consult with a licensed financial advisor, accountant, or legal professional who understands your personal financial situation.

Any links to third-party websites, tools, or platforms are provided for convenience and informational purposes only. Tech Capital Hub does not endorse or take responsibility for the content, accuracy, or practices of any third-party sites.